Intelligence in Motion,

Value Reimagined:

Automotive Industry Outlook 2026

Intelligence in Motion,

Value Reimagined:

Automotive Industry Outlook 2026

Eight key trends help automakers stay focused on intelligent transformation and capability upgrading amid a rapidly reshaping industry, turning technology investment into scalable value and unlocking new growth in an increasingly competitive market.

Turbulent times, diverging trajectories.

In 2025, amid intensifying macroeconomic uncertainty and the normalization of supply chain disruptions, the global automotive industry maintained overall resilience, yet structural tensions became increasingly pronounced:

Weak demand recovery and subdued consumer confidence in Europe and the United States have made the chain of “slowing growth, excess capacity, and margin pressure” increasingly pronounced. By contrast, China’s economy has remained relatively resilient amid a broader adjustment in its growth model and ongoing structural upgrading. Under the overarching principle of pursuing progress while maintaining stability, China’s economic growth is gradually moving beyond the traditional factor-driven path and entering a new stage centered on innovation-led development and total factor productivity improvement. Meanwhile, China’s automotive market has continued to operate at a high level. Through export-driven growth and product mix upgrading, it has partly offset capacity pressure and become an important anchor for the rebalancing of global automotive supply and demand.

Meanwhile, new energy vehicle (NEV) penetration continued its steady ascent. Hybrid powertrains served as a vital buffer for both volume and profitability under transitional "technology—cost—charging infrastructure" constraints; power batteries and core components drove robust upstream expansion, while the aftermarket—including charging networks and auto finance—accelerated its penetration, collectively propelling the industry from "single-OEM competition" toward a paradigm of "full value chain, multi-profit-pool competition."

On the competitive landscape front, the industry is shifting from "scale-driven competition dominated by legacy OEMs" to "capability-led divergence competition". Legacy automakers still command the global volume and profit base, yet emerging players and leading Chinese OEMs are continuously reshaping cost curves and technology diffusion pathways through electrification platformization, accelerated intelligent iteration, and scaling overseas expansion.

Taking China as an example, BYD, Geely, and Chery have built stronger offensive-defensive capabilities through scale and broadened product portfolios, while Leapmotor, XPeng, and Xiaomi are reinforcing differentiation via intelligent user experiences and customer engagement—driving Chinese automakers’ migration from traditional profit pools toward new revenue streams defined by "software, service ecosystems, data, and experience," and increasingly contesting global standards and mindshare.

Looking ahead to 2026, industry evolution will converge around three principal themes:

First, electrification transitions from "penetration growth" to "structural substitution"—NEV models will continue to serve as the core incremental driver of exports and global expansion, particularly in emerging markets such as Brazil, Southeast Asia, and Africa, where the confluence of demand release and industrial policy will accelerate market opening;

Second, intelligent mobility enters the "capital-intensive + scale monetization" phase—AI investment is concentrating on autonomous driving, intelligent cockpits, and smart manufacturing. The competitive focus is shifting from feature stacking to systemic capabilities in data closed-loops, algorithm iteration efficiency, and hardware-software synergy, with the brand landscape entering an initial phase of consolidation and winner-take-more dynamics;

Third, corporate growth logic extends from "selling vehicles" to "cross-sector positioning"—strategic initiatives in future mobility and next-generation components will become new profit-pool entry points, with automakers accelerating capability spillover and business extension into low-altitude economy, intelligent manufacturing, and advanced materials.

Intelligence leads the leap; value finds its new frontier.

2026 is not merely a continuation of cyclical recovery—it represents a repricing window for the global automotive industry amid growth-model transitions and profit-pool redistribution.

Premier offers a strategic lens on eight key automotive trends shaping 2026, underpinned by critical charts and case analyses, to help automakers assess the landscape, set benchmarks, chart their course, and seize the competitive advantage at this pivotal juncture.

DOWNLOADS

Lite Report (75 pages)

01. GLOBAL PROSPECT

From Vehicle Volume-Chasing To

Downstream Value-Capture:

Re-Plotting Value Chain Amid

Structural Overcapacity

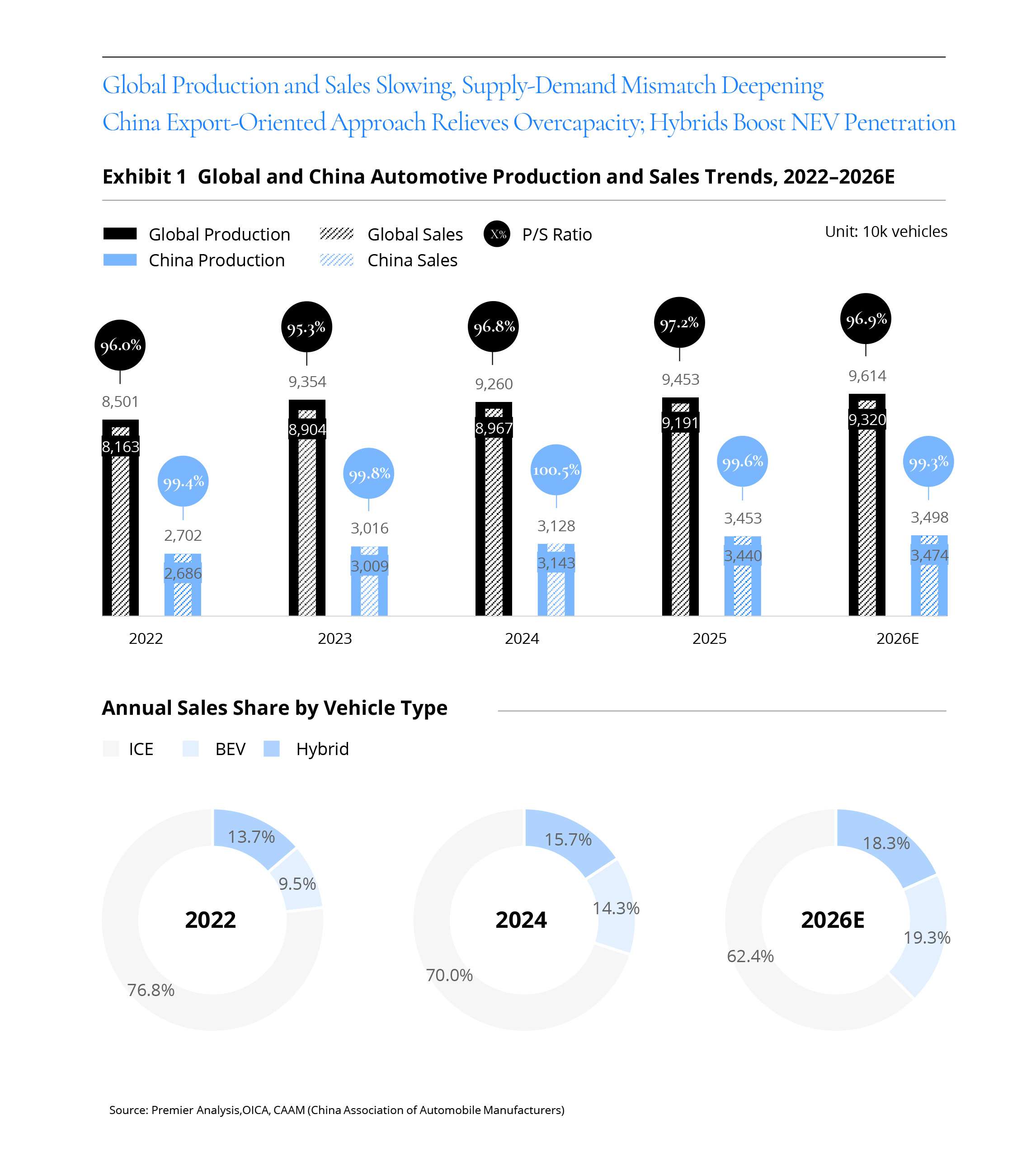

In 2025, propelled by pent-up demand recovery and accelerating electrification penetration, the global automotive industry charted a more resilient rebound trajectory: full-year vehicle production is projected at 94.53 million units, up 2.1% YoY; sales are estimated at 91.91 million units, up 2.5% YoY. NEV production and sales recorded 23.06 million and 20.70 million units respectively, with YoY growth exceeding 20%, making NEVs the critical “incremental engine” driving the industry forward.

Yet recovery does not equate to an unburdened path—the specter of global overcapacity persists, with high utilization rates difficult to sustain effectively, compounded by inventory buildups and rising costs in certain regions. Over the medium to long term, the intense capital demands of industrial transformation versus the practical constraints of capacity utilization create an increasingly acute tension, compelling some legacy OEMs to make difficult trade-offs between “absorbing excess capacity” and “betting on electrification.”

Against this backdrop, China’s automotive industry maintained robust high-level performance in 2025, emerging as one of the most definitive bright spots globally: full-year production reached 34.53 million units, with sales of 34.40 million units, representing YoY growth of 10.4% and 9.4% respectively—surpassing early-year expectations and marking the 17th consecutive year as the world’s largest market. Domestic NEV passenger vehicle penetration approached 60%, with sustained BEV and PHEV sales momentum reflecting consumers’ enduring preference for electrification while further consolidating the supply chain’s scale advantages and iteration speed.

Looking ahead to 2026, the global automotive industry is poised to enter a new range of “normalized low growth”: particularly in mature markets such as Europe and North America, as demand gradually approaches saturation, production and sales growth are expected to remain subdued. Weakening economic momentum and increasingly cautious consumer spending will further compress growth headroom for premium models and conventional ICE vehicles, subjecting them to more direct pressures from price sensitivity and deferred replacement cycles.

Nevertheless, the industry’s central narrative remains far from dim—the electrification transition will continue to accelerate, with NEV penetration expected to rise further. By 2026, global NEV sales are projected to account for approximately 30% of total volume, serving as the pivotal force enabling the industry to navigate through the cycle.

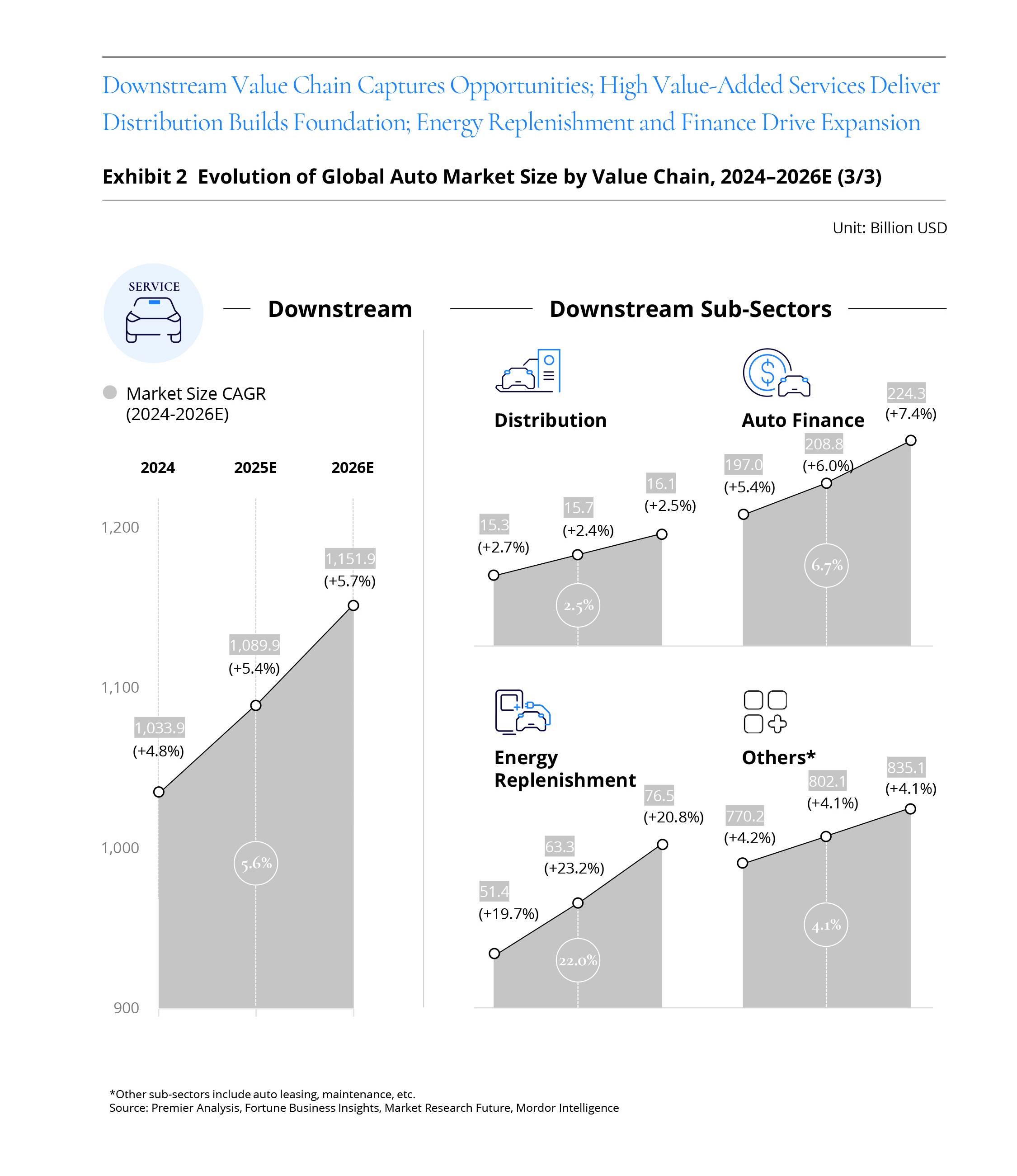

Looking further ahead, the automotive downstream market in 2026 is expected to sustain its expansion trajectory, with the overall market size projected to reach USD 1,151.9 billion, up 5.7% YoY. As the industry transitions from “capacity-driven” to “service-and-experience-driven” growth, downstream segments are emerging as the critical arena for capturing growth and realizing value—absorbing the spillover effects of volume recovery while reflecting the deeper restructuring of distribution channels, energy systems, and financial infrastructure.

Among these, the automotive distribution segment is expected to expand in tandem with the recovery of global vehicle sales, with the global market size approaching USD 16.1 billion by 2026. The penetration of digital channels and improvements in sales efficiency are driving the distribution system from single-point transactions toward an integrated “online-offline convergence” model: online engagement and conversion become more agile, while offline experiences and delivery grow more personalized. By integrating online ordering, content-led merchandising, offline test drives, and immersive showroom experiences, OEMs and dealers are not only shortening the purchase journey but also reshaping consumers’ brand and product perceptions through more refined interactions.

The energy replenishment market is projected to reach USD 76.5 billion in 2026, poised to become one of the most certain growth engines in the coming years. The buildout of charging networks and EV sales are reinforcing each other in a virtuous cycle: more vehicles drive denser charging networks; denser networks boost consumer confidence to purchase EVs. As policy support intensifies and deployment accelerates, charging infrastructure will extend to more cities and intercity corridor scenarios, paving a “visible road” for NEV adoption while unlocking broader incremental growth for the industry.

Meanwhile, automotive finance will maintain steady growth, with the global market size projected at USD 224.3 billion in 2026. In an environment of increasingly rational consumption and fluctuating capital costs, financial solutions are evolving from a “vehicle purchase tool” into a “consumer spending expansion lever”: rising financing demand for both new and used vehicles, expanding leasing and subscription services, and the gradual adoption of alternative financing models are deepening product coverage and broadening touchpoints. Auto finance not only underpins vehicle purchase accessibility but also delivers more resilient transaction and value-realization mechanisms across the industry chain.

02. REGIONAL EVOLUTION

East Asia At The Helm,

Recharting Global Auto Landscape

Emerging Markets Surge,

With EV Momentum Widening

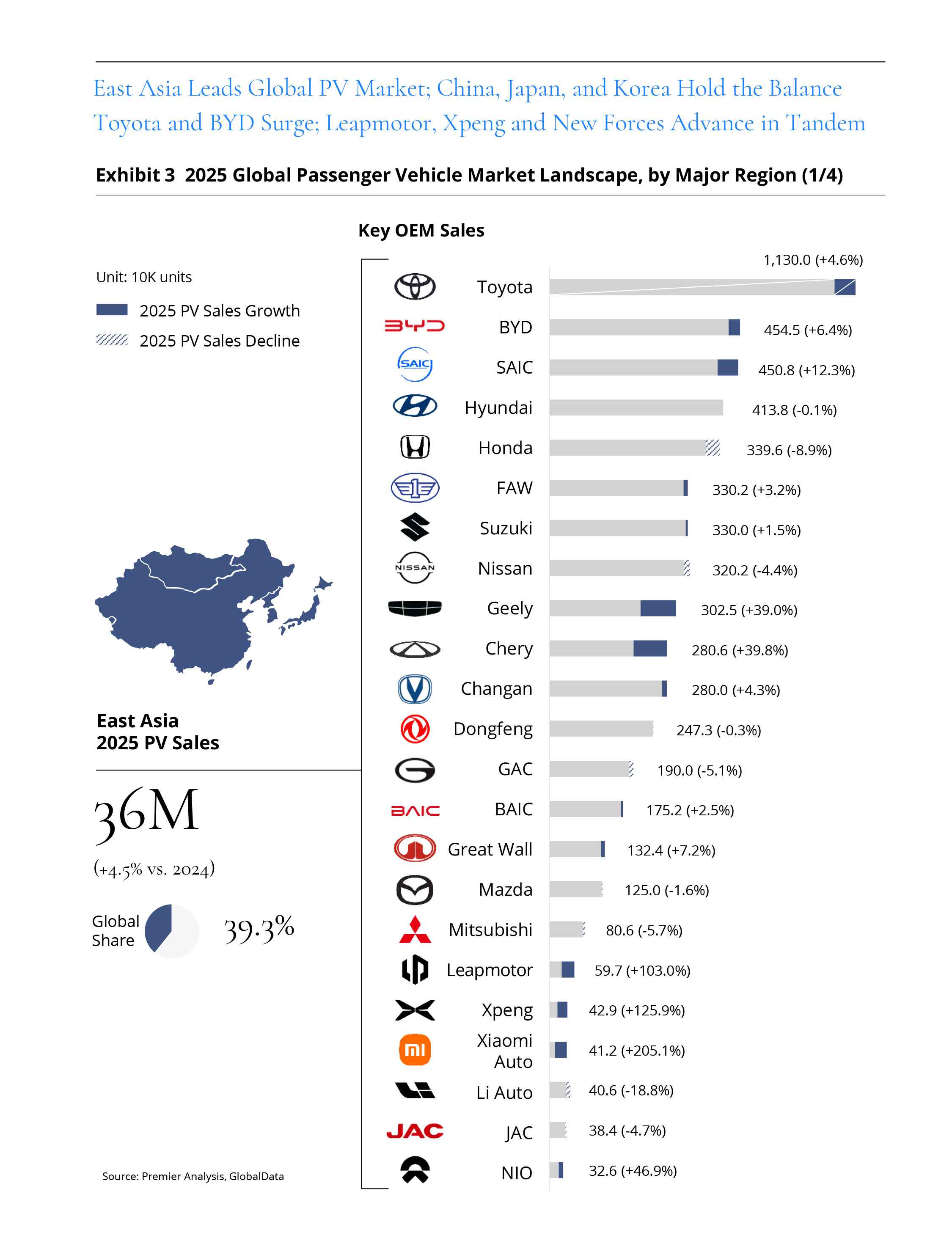

In 2025, total passenger vehicle sales in East Asia reached approximately 36 million units, accounting for 39.3% of global sales. As one of the most consequential “primary engines” of the global automotive industry, East Asia—underpinned by China, Japan, and South Korea—demonstrates increasingly pronounced growth resilience alongside structural divergence:

On one hand, regional sales volume remains firmly anchored in the global core range; on the other, the electrification journey is accelerating toward “systemic upgrading,” with the territorial shift between conventional ICE vehicles and NEVs becoming more defined. Whether in terms of sustained demand-side release or efficient supply-side organization, East Asia’s role as a critical hub and bellwether in the global automotive value chain is growing ever more prominent.

In China, the rapid scaling of electric vehicles continues to consolidate its position as the world’s largest passenger vehicle market. Rising NEV penetration makes China not only the largest electrification market globally, but also the preeminent “proving ground” for technology iteration and business model evolution.

By comparison, Japan and South Korea, while still predominantly driven by conventional fuel and hybrid powertrains, have not been absent from electrification and intelligent mobility investments: they are advancing product and technology roadmaps at a more measured pace, steering domestic markets toward lower-carbon and smarter mobility. Overall, East Asia’s combined advantage of “strong demand + strong manufacturing” ensures its irreplaceable strategic position in the global competitive landscape.

From an OEM performance perspective, Chinese automakers’ upward sales trajectory stands out prominently. BYD, leveraging its comprehensive and competitive NEV product matrix, continued to cement its global leadership, with full-year sales approaching 4.6 million units. Geely and Chery likewise delivered impressive results, with YoY sales growth of approximately 40%, further affirming the rising competitiveness of Chinese indigenous brands in the global industry chain. Meanwhile, emerging players such as Leapmotor, XPeng, and Xiaomi delivered even more disruptive performances, with sales doubling and rapidly ascending to the top ranks of Chinese OEMs. By contrast, under the dual squeeze of electrification trends and NEV competition, legacy OEMs such as Dongfeng and GAC faced more pronounced pressure, with declining sales trends highlighting the deepening challenges of transformation and innovation.

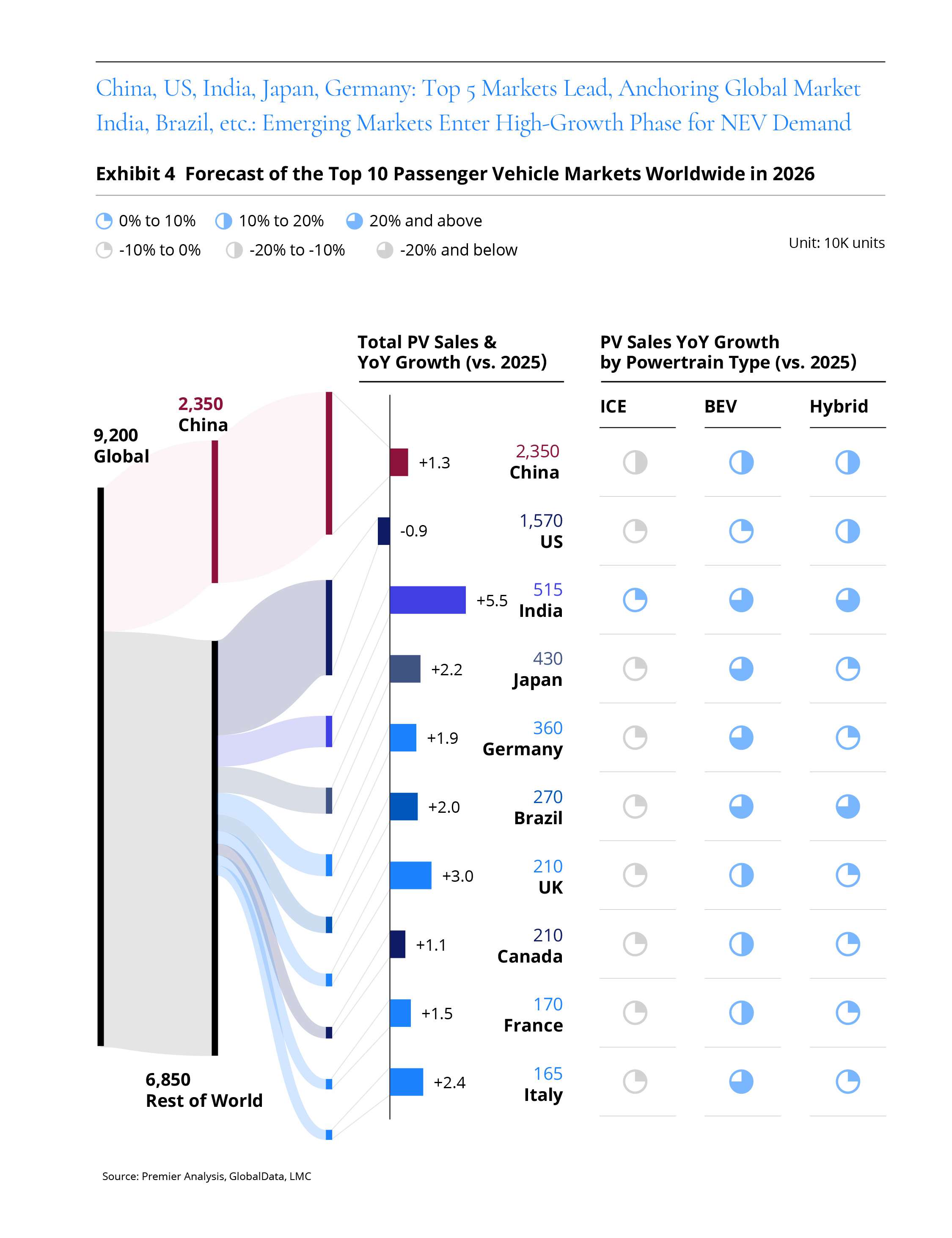

Under the combined pull of higher interest rates, heightened price sensitivity, and diverging electrification tempos, the global passenger vehicle market in 2026 will most likely sustain its overarching theme of “moderate recovery, structural reshaping”:

Under the combined pull of higher interest rates, heightened price sensitivity, and diverging electrification tempos, the global passenger vehicle market in 2026 will most likely sustain its overarching theme of “moderate recovery, structural reshaping”:

On the supply side, disruptions have largely dissipated and channel inventories are trending healthier, with global light-vehicle sales having recovered to approximately 91.70 million units in 2025—the industry’s “resilience” is returning to a predictable trajectory; on the demand side, however, the intensity of recovery has yet to fully reach the heights of the previous upcycle. Compounded by mature-market penetration rates and fleet-age structures gradually entering a “replacement-dominated” phase, the growth logic will shift from “broad-based expansion” to “structural divergence”—the differentiation across regions, powertrain pathways, and brand tiers will sharpen, with the competitive edge increasingly hinging on the integrated capability of cost discipline, technology commercialization, and channel efficiency.

China’s 2026 passenger vehicle sales are projected at 23.50 million units, up 1.3% YoY. The market will continue to exhibit a dual profile of “high-level steady state + structural gear-shifting”: at the aggregate level, stability prevails on a high base, with incremental growth primarily driven by NEV penetration and product-mix upgrading; exports will continue to serve as an important “pressure valve” for capacity and scale efficiency.

According to Premier estimates, NEV sales as a share of total are expected to rise further to approximately 55% in 2026, implying that the competitive focus will accelerate its shift from “chasing scale” to “competing on cost, technology commercialization, and channel efficiency”—leaders will consolidate their moats through systematic cost reduction and technology platformization, while laggards face accelerated divergence amid price wars and resource constraints, with the top-to-tail competitive race intensifying in parallel.

03. REGULATION SYSTEM

Regulatory Cadence Intensifies

as Regional Rulebooks

Diverge Market-Entry Controls

Shift Upstream,

Closed-Loop Compliance Becomes the Norm

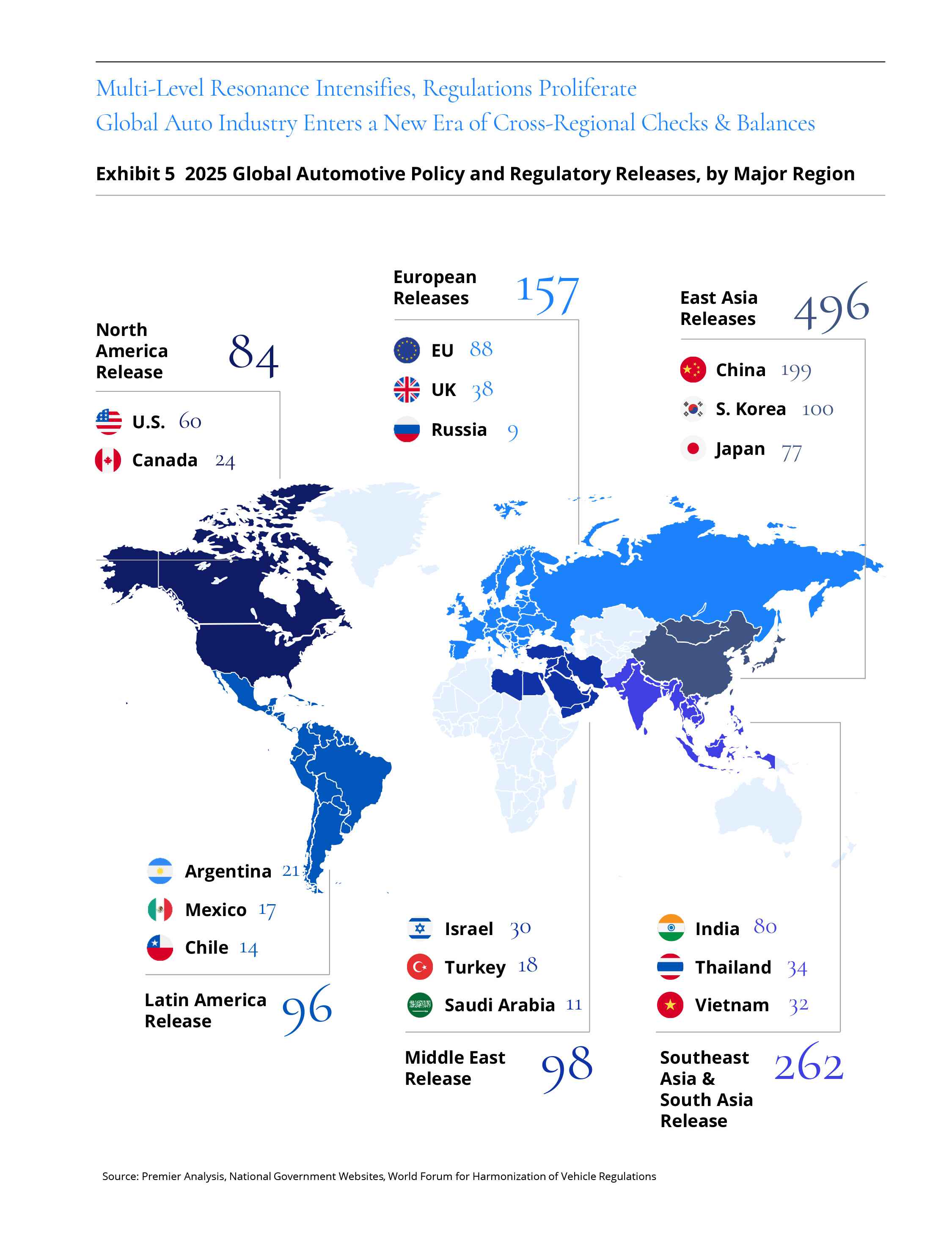

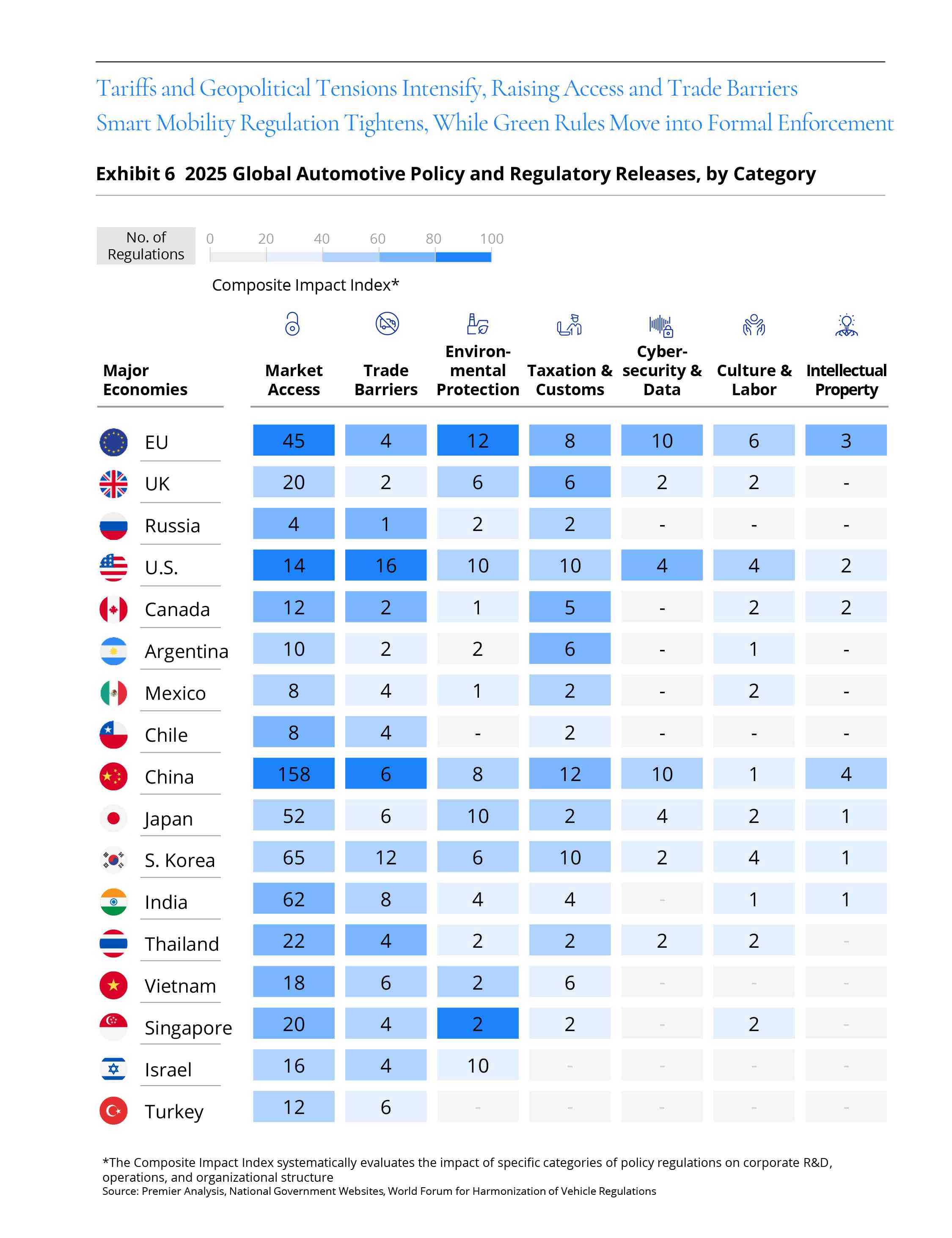

In 2025, global automotive policy and regulations exhibited stronger “hard constraint” characteristics: on one end, market access thresholds are shifting upward toward connected/software-defined vehicles, with regulators incorporating “combined driving assistance, OTA updates, cybersecurity, and recall closed-loops” into auditable and traceable governance frameworks; on the other end, trade and industrial policies are being reinforced, with tariffs, rules of origin, and local content requirements deployed more frequently to reshape supply chains and capacity footprints. The policy logic has shifted from “encouraging development” to “drawing red lines + strengthening governance,” with compliance costs and organizational coordination costs rising in tandem.

On the environmental and energy consumption front, 2025 continued the prevailing tone of unwavering decarbonization targets with enforcement mechanisms prioritizing pacing and operability: on one hand, emission reduction targets remain the policy mainline; on the other, certain markets are creating transitional buffer windows through phased mechanism adjustments to help the industry navigate between demand weakness and transformation investment. This also signals that electrification is not being “loosened”—rather, it is evolving from single-metric constraints to a more systematic policy mix, seeking new equilibria among emissions, energy, safety, supply chains, and industrial competitiveness.

Focusing on key policy directions by region: East Asia’s policy emphasis leans toward strengthened market access and front-loaded software governance, establishing more stringent technical parameters, filing requirements, and closed-loop management around connected vehicle functions, combined driving assistance, OTA updates, and quality/safety accountability.

North America’s policy mix more prominently features “industrial security + onshoring,” with trade barriers and tax/customs instruments (tariffs, rules of origin, domestic value ratios, etc.) directly impacting the cost structure of vehicles and key components, with spillover effects driving supply chain “ally-shoring/regionalization” restructuring.

Europe continues its underlying logic of “using environmental targets to drive industrial transformation,” with environmental protection regulations remaining the most critical policy anchor, while enforcement mechanisms place greater emphasis on actionable pacing management; in parallel, cybersecurity, data, and compliance governance continue to intensify, clarifying the safety, update, and liability boundaries of software-defined vehicles.

Southeast Asia and South Asia generally lean toward “growth-oriented regulation”, leveraging the interplay of tax/customs policies, market access rules, and localization requirements to attract investment and catalyze domestic supply chain development; environmental and NEV-related policies are gradually strengthening, though deployment pacing is more constrained by infrastructure readiness and consumer affordability.

Latin America’s policy focus typically centers on tax structures, import mechanisms, and local production incentives to drive local assembly of vehicles and components and supply chain localization; market access and certification systems are primarily oriented toward “facilitating model introduction and capacity landing.”

The Middle East’s policies emphasize balancing the consumer market with industrial upgrading, with market access and tax incentives often tied to economic diversification objectives; ICE vehicles retain practical advantages, but policies related to high-efficiency powertrains and new energy are gradually gaining prominence; growing attention to connected vehicles and data security, combined with labor and localization requirements, demands stronger on-the-ground operational capabilities from enterprises across distribution, service, and compliance systems.

Looking ahead to 2026, global automotive regulation will most likely continue to deepen along three principal threads:

1. Normalization of connected vehicle “access—operation—recall” closed-loop regulation, with requirements around OTA classification, software version governance, Cyber Security Management Systems (CSMS), and data compliance becoming increasingly granular and frequent;

2. Greater institutionalization of trade barriers and tax/customs instruments, reshaping cost curves and investment priorities through “local manufacturing + local value” mandates;

3. Environmental policies entering a phase of “targets maintained, pathways refined”, where enterprises will simultaneously face emission reduction constraints and industrial competitiveness constraints—the ability to convert compliance into scalable engineering and organizational capabilities will be the decisive differentiator.

04. BRAND LANDSCAPE

Brand Hierarchies Crystallize,

New Forces Gain a

Foothold Value Gravity Shifts,

Profit Divergence Sharpens

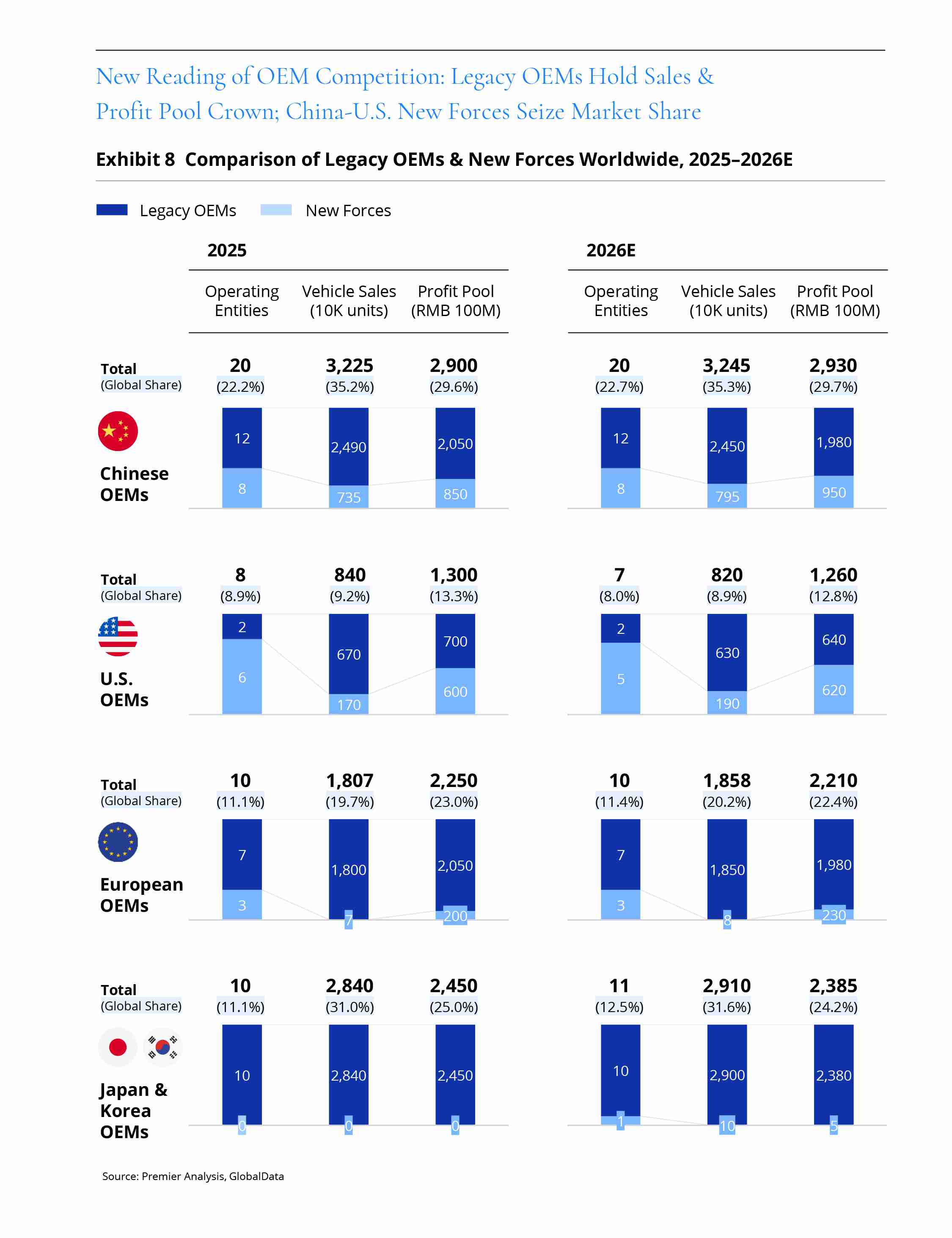

From a macro perspective, the Chinese automotive industry has entered a new phase of “multi-polar coexistence and structural reconfiguration”: legacy OEMs, leveraging their comprehensive manufacturing systems, dense distribution networks, and resilient supply chain integration capabilities, still command the industry’s scale foundation, dominating in terms of operating entity count and capacity coverage; emerging players, by contrast, are rapidly prying open market share in NEV sub-segments through more agile product definition, more focused intelligent experiences, and faster iteration cadences.

The U.S. automotive industry exhibits a “highly concentrated, clearly delineated” industrial order. Legacy OEMs emphasize systematic operations and capital efficiency at the entity level, forming a stable base through mature manufacturing platforms, high-margin segments such as pickups and SUVs, and well-established financial and distribution ecosystems; emerging players occupy the commanding heights of the electrification and software narrative, wielding stronger influence in brand mindshare and technology roadmap leadership.

The European automotive industry reflects the structural tension of “systemic advantages coexisting with transformation pressures.” Legacy OEMs retain overwhelming advantages in engineering capabilities, brand equity, and global distribution, yet rising organizational complexity and compliance costs increasingly constrain their transformation pace. Emerging players in Europe face higher regulatory, certification, and service network barriers, making scaling significantly more difficult than in other regions—they must not only sell the product but also build out the entire operational system.

The Japanese and South Korean automotive industries feature more concentrated industrial organization, with legacy OEMs having accumulated deep strengths in operating entities, supply chain integration, and global production-sales systems, leaving relatively limited room for emerging players. The sales landscape is highly stable: legacy OEMs not only dominate domestically but also maintain scale advantages through their globalized footprint. Their profit pools derive more from manufacturing efficiency, global division-of-labor systems, and the long-term returns of high-reliability technology pathways.

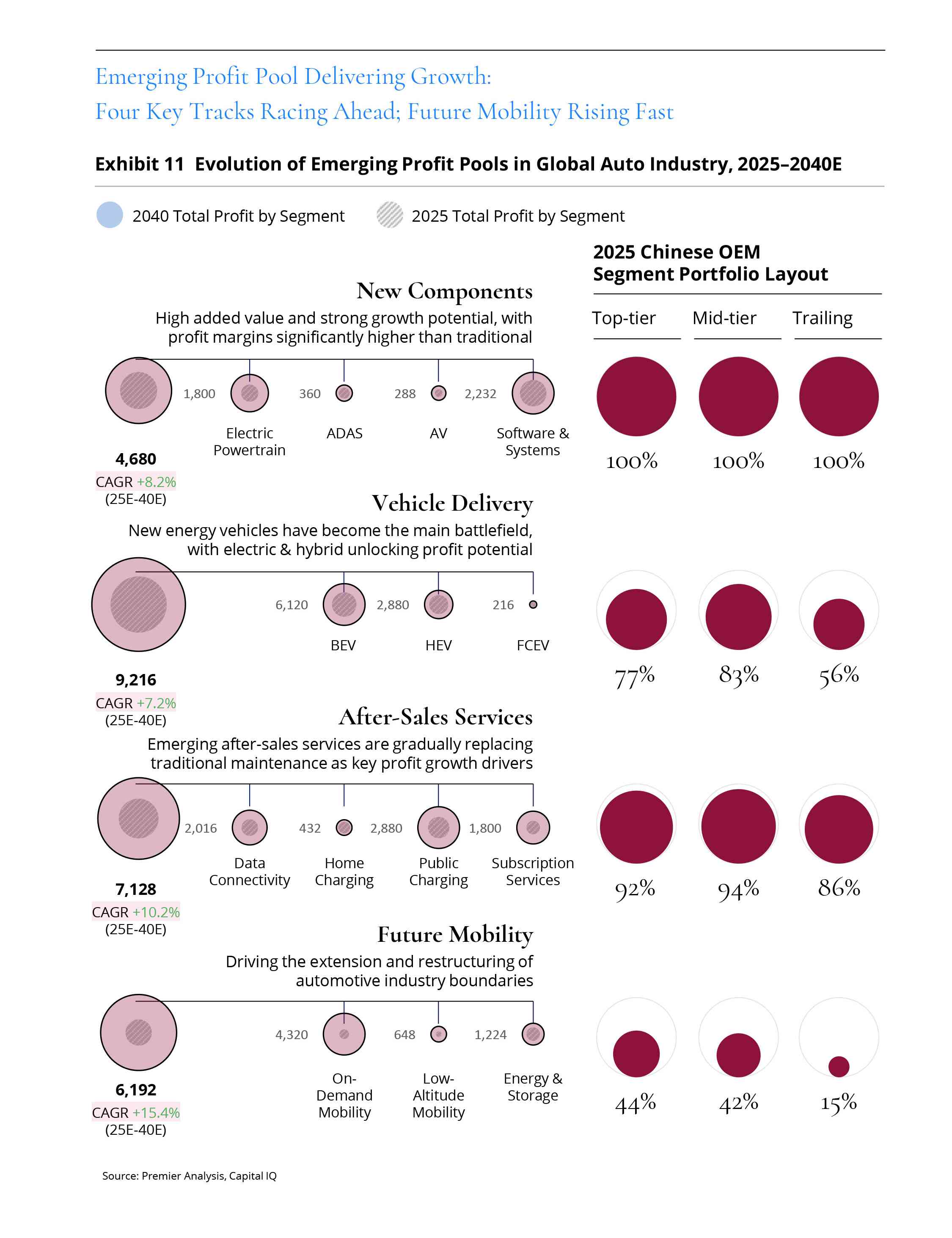

From the medium-to-long-term perspective of 2025–2040E, emerging profit pools are becoming the core engine driving the profitability reconfiguration of the global automotive industry. Compared with the deceleration or even contraction of traditional segments, four sectors—next-generation components, NEV-centric vehicle delivery, data-driven aftersales services, and future mobility—are exhibiting clearer expansion trajectories.

In the new components domain, the profit structure exhibits a dual profile of “high value-add + high growth.” Electrified powertrains, Advanced Driver Assistance Systems (ADAS), autonomous driving-related hardware and software, and software/system platforms are progressively replacing traditional mechanical components to become the “new heart” of vehicle value. Unlike traditional components that rely more heavily on scale effects, next-generation components emphasize technology barriers and algorithmic capabilities, with gross margins and return on capital significantly outperforming conventional hardware manufacturing segments. As the software-defined vehicle trend deepens, in-vehicle operating systems, domain controller architectures, and vehicle-cloud synergy capabilities will continue to amplify the profit leverage effect.

The profit logic of the vehicle delivery segment is also undergoing a qualitative transformation. NEV models have become the primary global competitive battleground, with BEV and hybrid penetration rates continuing to rise, driving structural profitability improvements in vehicle delivery. Scalable platform reuse, declining three-electric-system costs, and differentiated product pricing power are significantly enhancing the earnings elasticity of NEVs. Going forward, vehicle profits will no longer depend purely on sales volume, but increasingly on the combined strength of technology platform capabilities and brand premium power.

The after-sales services segment is transitioning from “repair-driven” to “data-and-energy-driven.” Growth headroom for traditional maintenance and repair is becoming increasingly constrained, while data-connected remote diagnostics, software upgrades, feature subscriptions, and charging/refueling ecosystem operations are gradually emerging as new profit growth poles. The continuous accumulation of data assets enables OEMs to extend into full-lifecycle customer management, converting one-time deliveries into sustainable service revenue models.

The future mobility segment represents the direction and imaginative space for industry profit extension. Business models such as mobility-on-demand, low-altitude mobility, and energy synergy are driving the automotive industry’s upgrade from “manufacturing” to a “comprehensive mobility and energy operations platform,” with potential profit levels and value creation logic far exceeding the traditional vehicle sales model. Although near-term commercialization pathways still require validation, over the long term this segment is poised to become the fastest-growing area with the greatest marginal headroom within the profit pool.

At the enterprise positioning level, Chinese automakers—building on a decade of capability accumulation in electrification, supply chain integration, and platform-based R&D—are progressively completing their overall deployment across emerging profit pools.

Leading players have already established scale advantages in next-generation components and NEV delivery; mid-tier players are accelerating their extension into intelligent and software capabilities; and tail-end players are beginning to seek breakthroughs around charging infrastructure and data services. Future mobility is becoming the next strategic frontier, though its profit potential still requires “translation into reality” through business model innovation and operational capability maturation.

05. CONSUMER INSIGHTS

Willing-To-Pay Benchmarks Ascend,

Value Earned By Verifiable Need

Decision Criteria Anchor Reputation Confers Trust,

Smart-Mobility Experience Delivers Validation

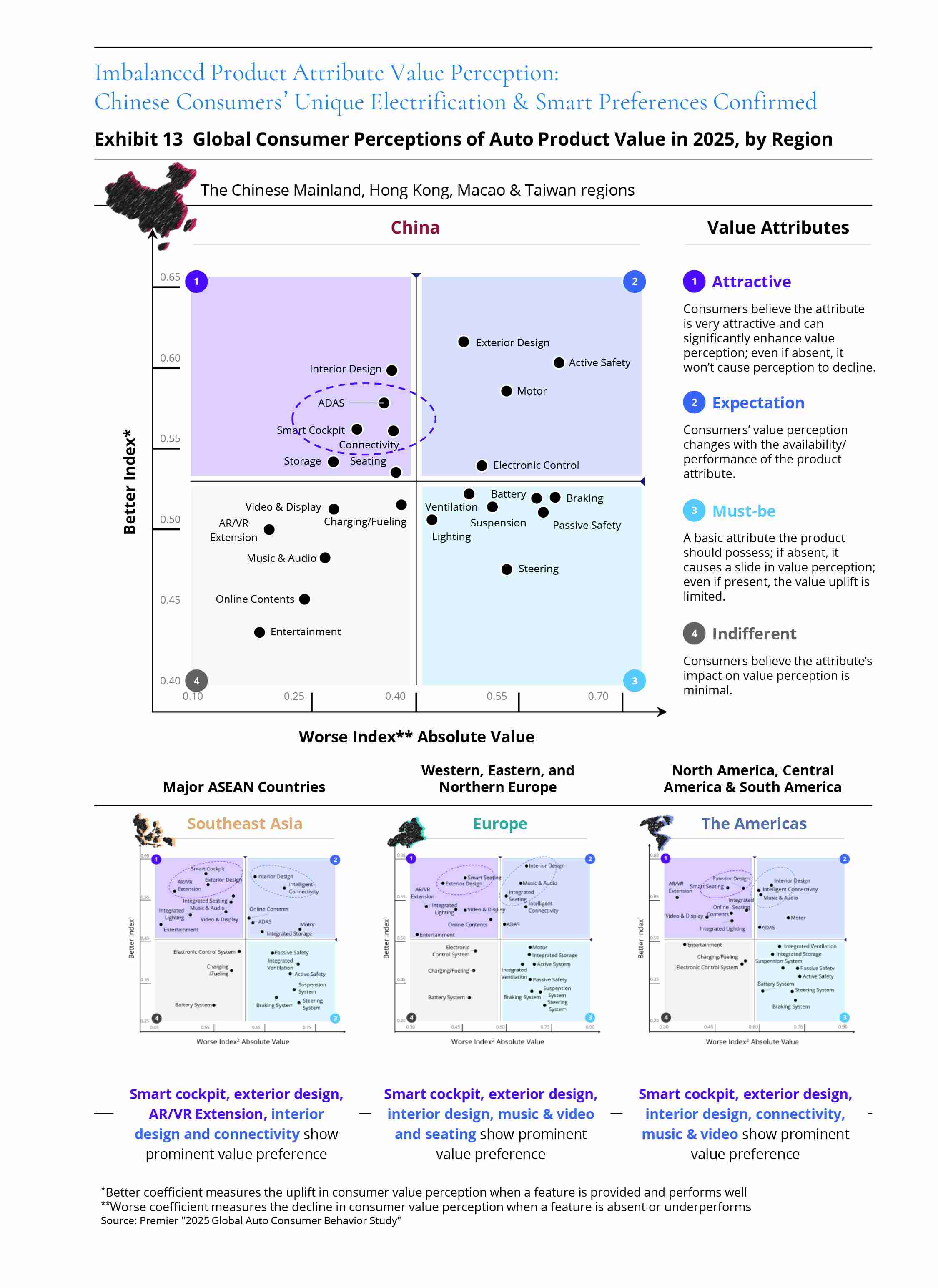

Focusing on global automotive consumers’ purchase decisions and product value preferences, Premier conducted the “2025 Global Automotive Consumer Behavior Study” in the preceding year, providing a comprehensive assessment of how consumers across major global regions perceive the value of different vehicle product attributes. Through detailed analysis of consumer responses to changes in product attributes, the study revealed differentiated demand across global markets in areas such as electrification, intelligent features, and design aesthetics.

Based on these findings, we have categorized consumers’ value perceptions of various vehicle attributes into the following four types:

Consumers perceive this product attribute as having significant appeal in enhancing product value, greatly boosting their overall assessment of the product. However, even if this attribute is absent, consumers’ value perception does not decline significantly.

Consumers’ value perception is directly correlated with the performance of this product attribute. The degree of functional completeness directly influences the overall product value assessment—the better the functional performance, the higher the perceived value.

Consumers regard this attribute as a fundamental product requirement—its absence leads to a significant decline in perceived product value. While its fulfillment may not deliver a notable value uplift, its absence is unacceptable.

Consumers perceive this attribute as having virtually no impact on their value assessment—regardless of whether the attribute is present, absent, or modified, it produces no discernible change in consumer evaluation.

When comparing the value preferences of Chinese consumers with those in other regions, distinct geographic divergence emerges. In the electrification technology dimension, core capabilities represented by battery systems and electronic control systems are largely classified by Chinese consumers as “Must-be” and “Expectation” attributes—meaning electrification features are no longer optional configurations but pivotal factors influencing vehicle purchase decisions.

In the intelligent mobility domain, particularly driving assistance, intelligent cockpit, and connected vehicle features, Chinese consumers demonstrate markedly stronger preferences. Notably, in the driving assistance dimension, only Chinese consumers tend to classify it as “Attractive”—meaning it is perceived not merely as providing safety and convenience.

In other regions, driving assistance is more commonly categorized as “Expectation”, considered something that “should be available” but not necessarily sufficient to generate strong purchase appeal. This finding indicates that Chinese consumers’ expectations for intelligent features have transcended the basic functionality level, with intelligent experiences increasingly serving as a yardstick for measuring product advancement and brand perception.

Equally intriguing is that the value perception of interior design also reflects a distinctive “aesthetic leap” in the Chinese market. In other global regions, interior design tends to be categorized as “Performance” or regarded as a basic expectation; in the Chinese market, however, interior design is more frequently classified as “Attractive”—consumers’ pursuit of refinement, craftsmanship, and emotional value is on the rise, with vehicles no longer merely a means of transportation but an extension of personal taste and lifestyle. This reflects a shift among Chinese consumers from purely functional demands toward an emphasis on holistic user experience and aesthetic sensibility.

In summary, the differentiated consumer demands across global regions in electrification, intelligent features, and design aesthetics are driving divergent development in the global automotive industry’s product positioning, technology R&D, and market strategies. For OEMs, the real challenge lies not only in developing the technology, but in deploying it in “the right market, the right context, and at the right value anchor”: understanding each market’s consumer value weightings and formulating more precisely targeted product portfolios and marketing narratives is essential to converting advantages into winning positions in global competition.

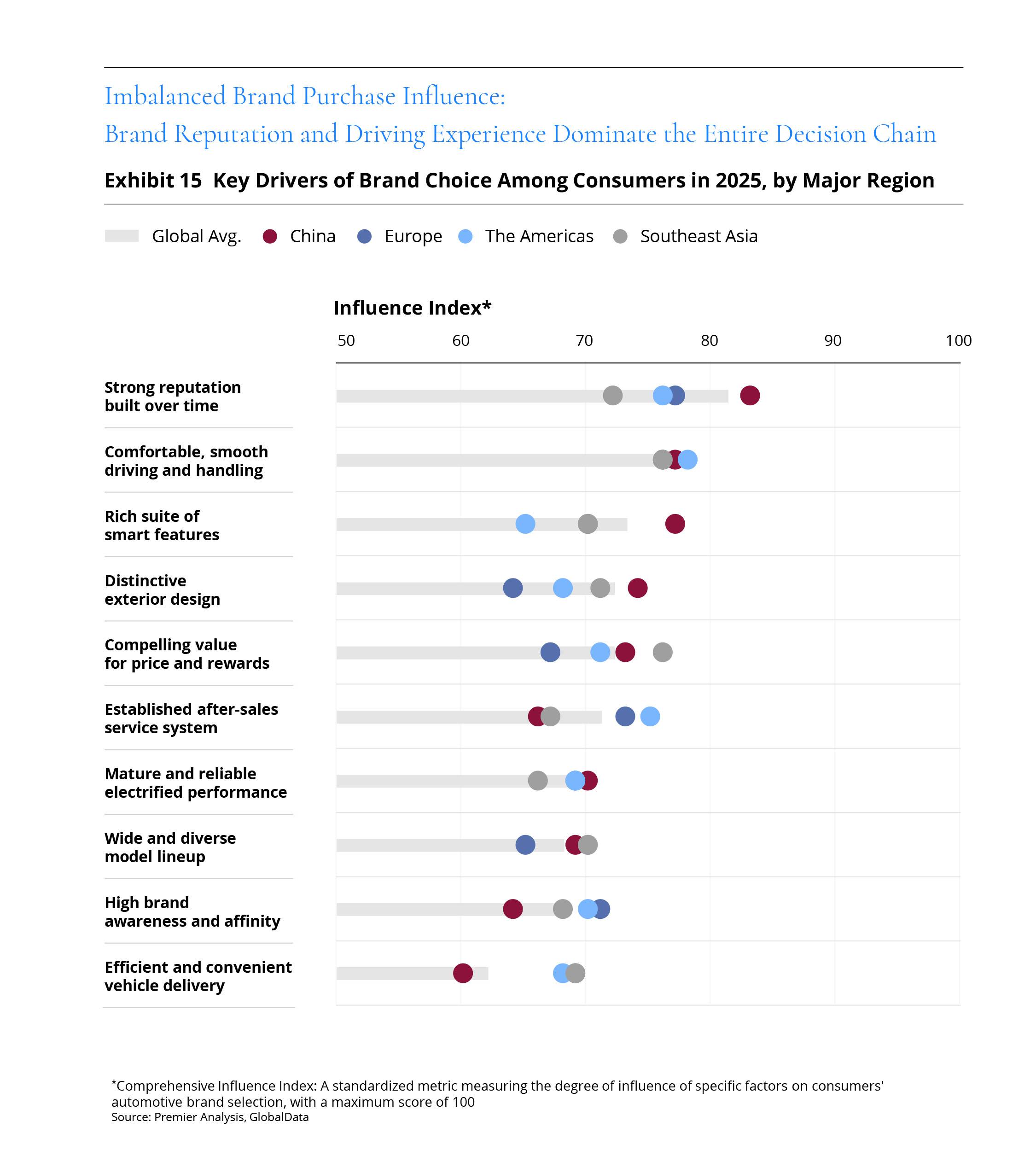

In the actual purchasing process, global consumers universally regard brand reputation and driving experience as the core drivers of vehicle purchase decisions.

Brand reputation reflects consumers’ emphasis on a manufacturer’s history, word-of-mouth, innovation capability, and long-term value, often serving as a critical benchmark when consumers weigh multiple options. Brand standing not only relates to consumer trust but also directly influences product expectations and loyalty.

Driving experience—particularly comfort and stability of handling—is a key factor determining day-to-day usability. Whether for daily urban commuting or long-distance highway travel, a superior driving experience significantly enhances consumer satisfaction and a vehicle’s added value.

Looking more specifically, Chinese consumers place higher demands on brand reputation and intelligent feature configurations. Brand image has become a major consideration in purchase decisions, representing not only consumer trust and identification with the manufacturer, but also closely tied to the manufacturer’s social responsibility, environmental contribution, and innovation capacity. As intelligent technologies become increasingly mainstream, Chinese consumers’ preference for smart features continues to intensify, with demand for intelligent cockpits, driving assistance, and connected vehicle functions growing particularly pronounced.

Southeast Asian consumers place greater emphasis on value for money in their purchase decisions, reflecting their heightened focus on vehicle practicality and cost-effectiveness. Given the region’s relatively lower levels of economic development and household income, with automotive markets not yet fully matured, consumers are more inclined to choose moderately priced models with reliable performance. Although electrification and intelligent technologies are gradually entering the Southeast Asian market, consumer demand for these innovations remains relatively conservative, primarily centered on fundamental attributes such as fuel economy, durability, and low maintenance costs.

European and American consumers place comparatively greater importance on the vehicle delivery experience and aftersales service, while exhibiting relatively lower demand for electrification and intelligent technologies. Consumers in Europe and the Americas continue to value traditional automotive virtues, particularly driving experience, handling dynamics, and comfort. In Europe especially, driving pleasure and vehicle handling stability remain critical considerations when selecting a vehicle. Although electrification and smart technologies are gradually gaining traction in these markets, consumer requirements for intelligent features are more moderate—they tend to favor established automotive brands that deliver stability, high-quality driving experiences, and long-term durability over the pursuit of technological novelty. Even when considering electrified models, consumers typically focus on driving feel, range capability, and charging convenience.

06. TECHNOLOGY FRONTIER

AI Investment Surges,

R&D Returns Approach Inflection

Hardware Rationalizes Into The Stack,

Vehicle–Cloud Software Convergence Accelerates

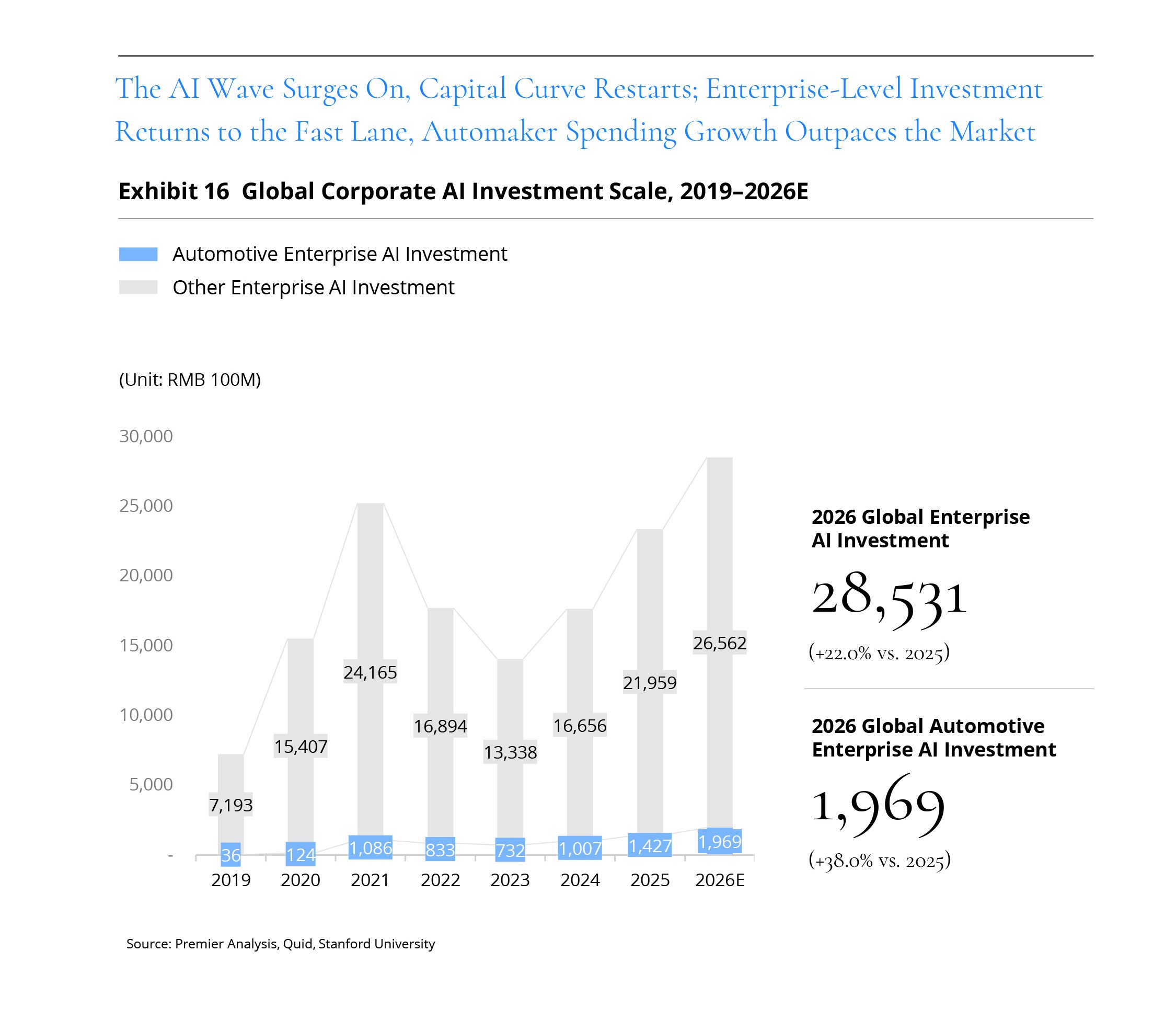

Since 2019, global corporate investment in artificial intelligence has exhibited distinct phased characteristics of “initial acceleration, subsequent pullback, and renewed surge.” From 2019 to 2021, as digital transformation and automation upgrades deepened, enterprises significantly increased their AI technology investments—particularly in enhancing operational efficiency, improving user experiences, and supporting new business models—with AI becoming an integral component of digital strategies.

However, from 2022 to 2023, shifting global economic conditions, combined with the dual pressures of macroeconomic uncertainty and capital contraction, led to a cyclical retreat in overall AI investment. Capital market caution and uncertain growth expectations prompted some enterprises to decelerate their AI spending.

Nevertheless, beginning in 2024, with the maturation of generative AI technologies and large language model capabilities, and the accelerating deployment of industrial-grade AI applications, global corporate AI investment re-entered an upward trajectory. This recovery reflects not only advancing technological maturity but also signals AI’s progression from “exploratory spending” to “strategic capital allocation”.

Against this backdrop, automotive enterprises’ AI investment growth has significantly outpaced the global corporate average, demonstrating stronger cyclical resilience and strategic conviction. AI has become deeply embedded across core automotive industry segments—from autonomous driving algorithm training and data closed-loop capability building, to intelligent cockpits, voice interaction, and vehicle-cloud synergy, through to R&D simulation, supply chain optimization, and manufacturing automation.

Compared with other industries, automakers not only possess high computing-power demands and massive data foundations but also bear the frontline pressure of intelligent competition, making AI a decisive variable in determining product competitiveness and brand premium. As overall corporate AI investment returns to a growth trajectory, the automotive industry has established a “technology-pulls-capital” investment logic, with the strategic nature and long-term orientation of AI spending becoming increasingly prominent.

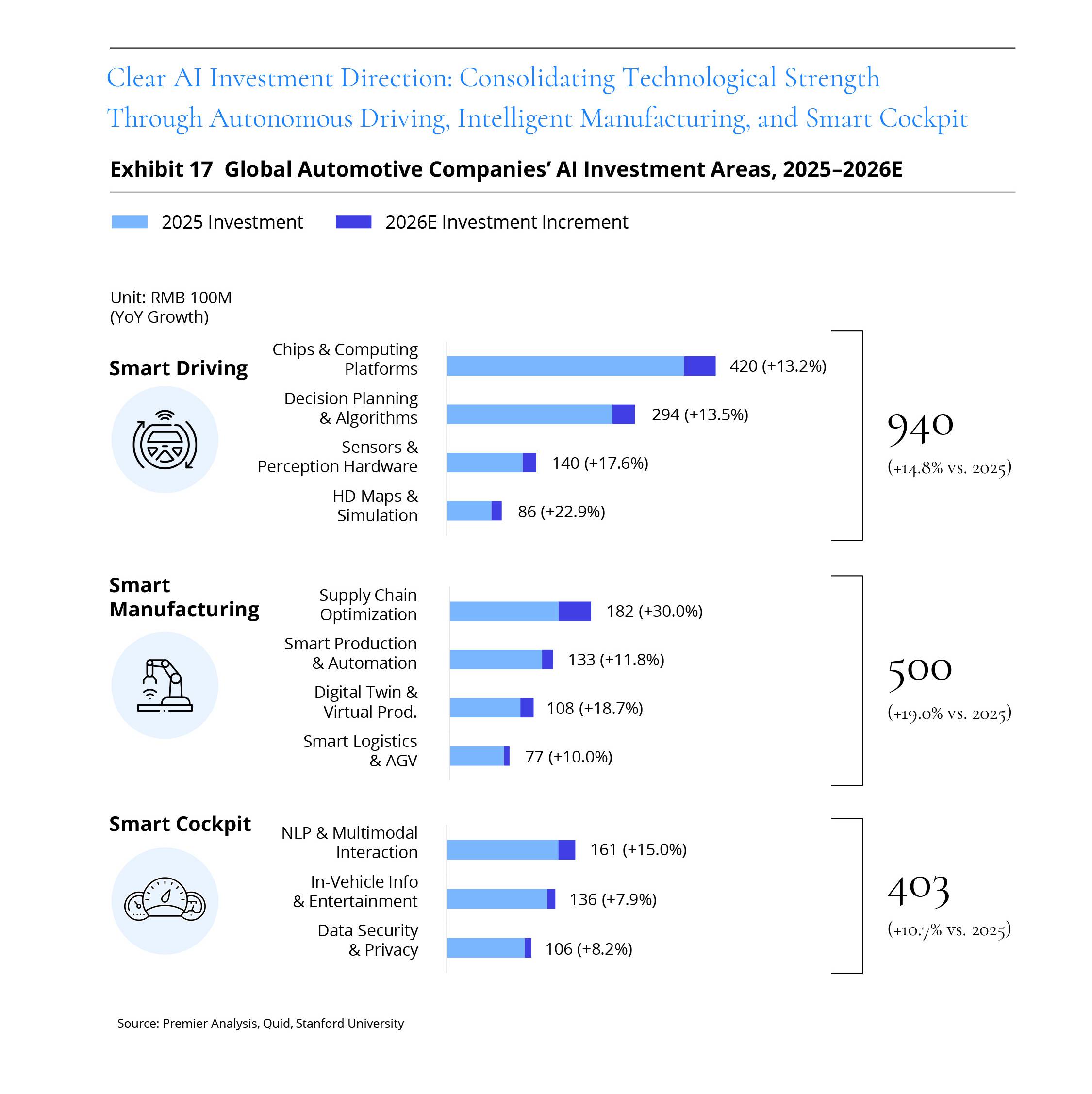

Overall, global automotive enterprises’ AI investment has formed a “three-pillar” structure—autonomous driving, intelligent manufacturing, and intelligent cockpit have emerged as the three core directions commanding the most concentrated capital and resource deployment. This distribution reflects that OEMs’ AI application logic has evolved from isolated feature upgrades to a full-chain reconfiguration spanning “product—production—user experience.” AI is no longer merely an auxiliary technology but is directly embedded in the core value-creation process, becoming a decisive variable in vehicle competitiveness and organizational efficiency.

In the autonomous driving domain, investment priorities are concentrated on chips and computing platforms, decision-planning algorithms, sensors and perception hardware, and HD maps and simulation platforms. Among these, chips and computing platforms form the foundational computing layer and serve as the core enabler for autonomous driving capability iteration; decision-making and algorithms determine system performance and safety boundaries, constituting the key barrier for OEM differentiation; sensors and perception hardware form the data entry point, tightly coupled with algorithms; while HD maps and simulation platforms support scalable testing and continuous optimization.

In the intelligent manufacturing domain, AI investment revolves around intelligent supply chain optimization, smart production lines and automation, digital twins and virtual production, and intelligent logistics and AGV coordination. Compared with autonomous driving’s product-oriented nature, intelligent manufacturing places greater emphasis on structural optimization of efficiency and cost. Supply chain intelligence enhances inventory turnover and risk forecasting capabilities, strengthening organizational resilience; smart production lines and automation improve manufacturing consistency and quality control; digital twin technology reinforces R&D-production synergy and shortens development cycles; intelligent logistics elevates intra-plant and cross-regional coordination efficiency.

In the intelligent cockpit domain, investment priorities center on natural language and multimodal interaction, in-vehicle entertainment and infotainment systems, and data security and privacy protection. As generative AI and large model capabilities mature, the cockpit has become the core high-frequency interaction interface between OEMs and users, with natural language and multimodal interaction emerging as key enablers for enhancing brand stickiness and user experience; in-vehicle infotainment platforms are strengthening content ecosystem development, driving the transition from one-time sales to continuous services; data security and privacy protection serve as the compliance foundation for commercialization.

In essence, autonomous driving determines product height, intelligent manufacturing determines efficiency depth, and the intelligent cockpit determines user engagement depth. Together, they constitute the core pillars of OEMs’ AI strategies, forming a highly interconnected system across the technology foundation, system integration, and business model layers.

07. CROSS-SECTOR EXTENSION

Mobility Boundaries Expand,

Platform Operating Models Reset Roles

Tri Sectors Shape The Blueprint,

Eight Archetypes Define The Playbook

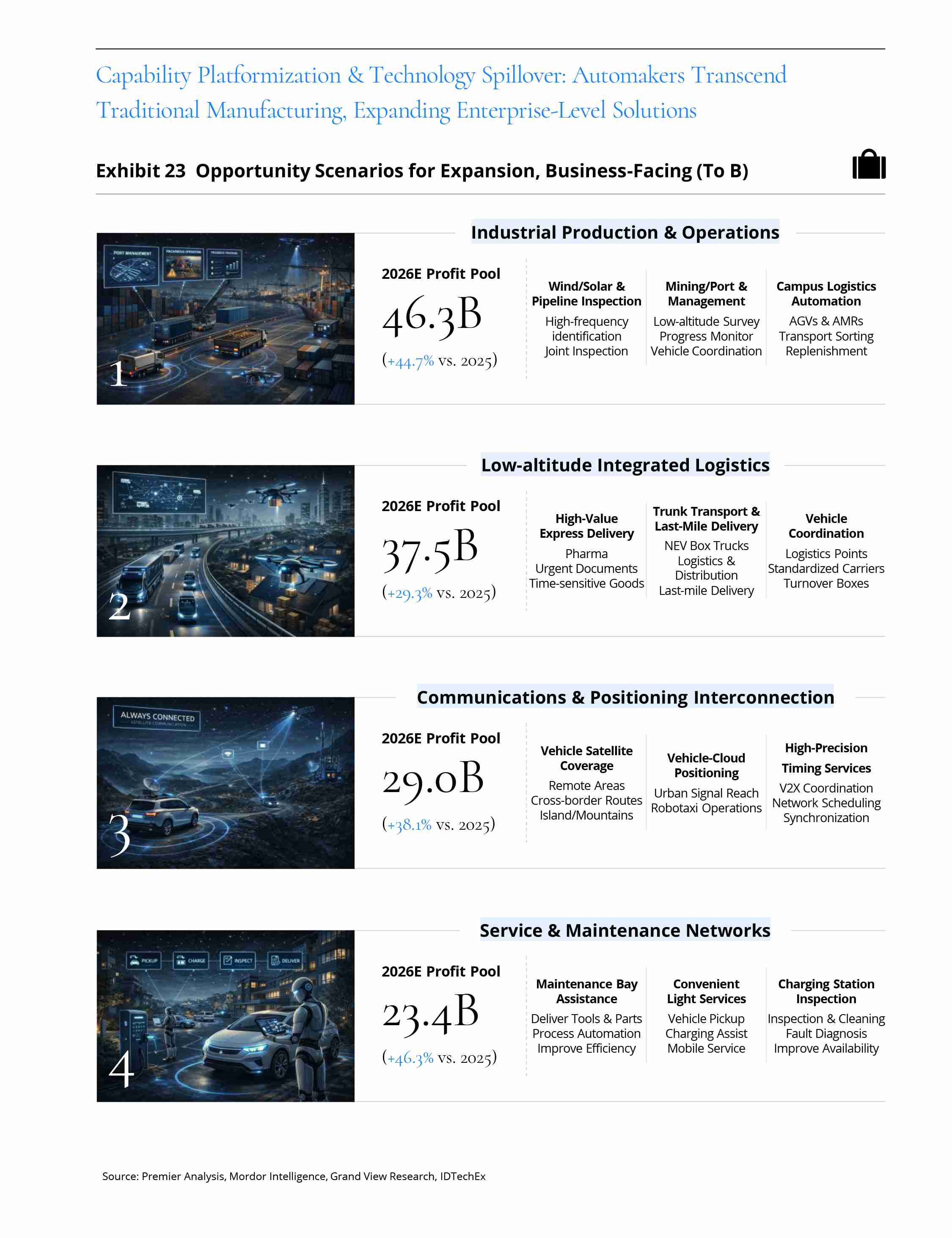

Global automakers are progressively breaking beyond the traditional boundaries of vehicle manufacturing and sales, leveraging their core capabilities accumulated in electrification system integration, autonomous driving algorithms, vehicle-road coordination, and digital operations to spill over into broader enterprise-grade application scenarios.

As industry competition shifts from single-product performance to systems solution capability, OEMs are assuming the role of “technology platform exporters”, participating in diverse ecosystems including industrial operations, logistics systems, communications infrastructure, and service networks, opening up enterprise-level businesses as new profit growth curves.

This capability migration not only enhances asset utilization efficiency but also drives the automotive industry’s transformation toward a comprehensive platform combining “mobile intelligent terminals + systematic operational capabilities”.

In industrial production and operations scenarios, automakers can leverage their accumulated strengths in autonomous driving algorithms, intelligent dispatching systems, and vehicle-side perception capabilities to enter application domains such as port management, mining transportation, unmanned campus logistics, and warehouse coordination.

Integrated low-altitude logistics represents one of the frontier directions for automakers’ cross-sector expansion. Building on vehicle-side autonomous perception, path planning, and remote monitoring capabilities, OEMs can collaborate with drone enterprises and local governments to construct “air-ground coordinated” transportation networks, enabling task allocation and route linkage between drones and ground intelligent vehicles.

Communications and positioning connectivity serves as the foundational enablement layer for OEM capability export. Leveraging V2X connectivity, high-precision positioning, satellite communications, and edge computing capabilities, automakers can participate in intelligent transportation infrastructure construction and vehicle-road coordination system deployment. In remote areas, highly complex road conditions, or disaster environments, building a “vehicle–road–cloud” integrated communications network enables real-time data transmission, remote control, and dynamic route optimization.

Service and maintenance networks reflect automakers’ extension potential in aftermarket capabilities. Through remote diagnostics, OTA upgrades, and predictive maintenance algorithms, OEMs can offer enterprise clients full-lifecycle equipment management solutions, encompassing fleet management, energy replenishment optimization, and maintenance resource scheduling.

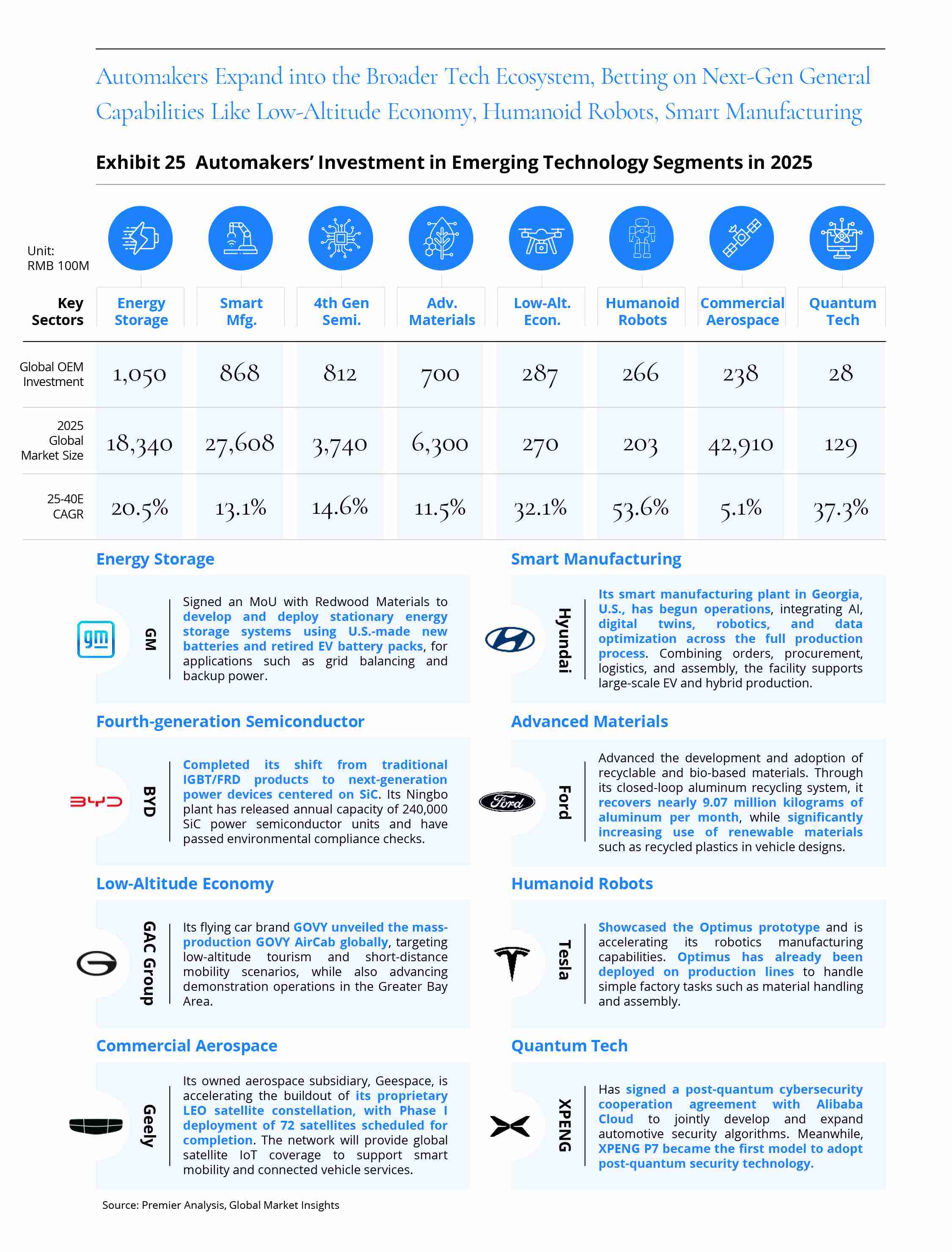

In 2025, global automakers’ investment in emerging technology sectors has shifted from single-domain breakthroughs to a broader technology industry deployment, exhibiting strategic characteristics of “front-loaded capabilities, boundary extension, and ecosystem synergy.”

From next-generation energy storage to fourth-generation semiconductors, from intelligent manufacturing to the low-altitude economy and commercial aerospace, OEMs’ investment directions clearly demonstrate that electrification and intelligent mobility have become core growth drivers, with cross-industry technology integration and ecosystem expansion accelerating.

Technology iteration in the next-generation energy storage domain is reshaping the traditional automotive industry’s energy architecture. Battery systems are no longer confined to drivetrain applications but are beginning to permeate broader energy management systems. Through tight integration of battery and electronic control technologies, OEMs can not only enhance vehicle range but also participate in global energy market construction, driving the formation of “vehicle–storage–grid” systems and elevating overall value chain efficiency.

In intelligent manufacturing, automakers are progressively optimizing the efficiency and flexibility of their production systems through smart production lines, AI-powered quality inspection, and flexible manufacturing. The continuous advancement of intelligent manufacturing enables OEMs to respond more efficiently to market demand shifts, enhance customization and quality control capabilities, and thereby secure competitive advantages in cost management and innovation speed.

The application of fourth-generation semiconductors, particularly in electrification and autonomous driving technologies, has become a key factor in enhancing vehicle performance. Through investment in advanced materials such as SiC (silicon carbide) and GaN (gallium nitride), OEMs can achieve breakthroughs in power density, thermal management, and efficiency, providing robust support for EV battery management and drivetrain systems.

In the advanced materials domain, automakers are actively pursuing lightweight, eco-friendly, and recyclable materials, steering the entire automotive industry toward sustainable development. Innovation in advanced materials not only helps reduce vehicle energy consumption and emissions but also plays a significant role in enhancing vehicle safety and driving experience, further consolidating OEMs’ competitive positioning.

The low-altitude economy, as a vital component of future mobility, is emerging as a frontier for automakers’ cross-sector expansion. By combining autonomous perception, path planning, and drone technologies, OEMs can participate in air-ground integrated transportation networks, driving the intelligent upgrading of logistics and mobility. As policies gradually liberalize, this domain is poised to become a critical entry point for OEMs’ expansion into smart cities and regional logistics.

In the humanoid robotics domain, automakers are leveraging their accumulated expertise in perception, power control, and battery management to progressively expand into service applications. These robots can not only enhance production and operational efficiency but also create new market opportunities in the service industry, household, and personal domains.

Commercial aerospace presents automakers with new opportunities for breakthroughs in communications and positioning technologies. By participating in the construction of low-Earth orbit satellite networks, OEMs can enhance their global network coordination capabilities and provide high-precision data support for autonomous driving technologies worldwide.

Although quantum technology remains in its early stages, its potential in big data processing and complex system optimization offers automakers a more far-reaching strategic perspective. As quantum computing matures, OEMs stand to gain competitive advantages in data analytics, algorithm optimization, and the performance enhancement of automotive intelligent systems.

08. OVERSEAS EXPANSION

Vehicle Exports Set A High Baseline,

Value-Chain Synergy Extends The Upcycle Five Strategic Plays Define The Path,

Tighten Execution Handoffs,

Restore Key Linkages

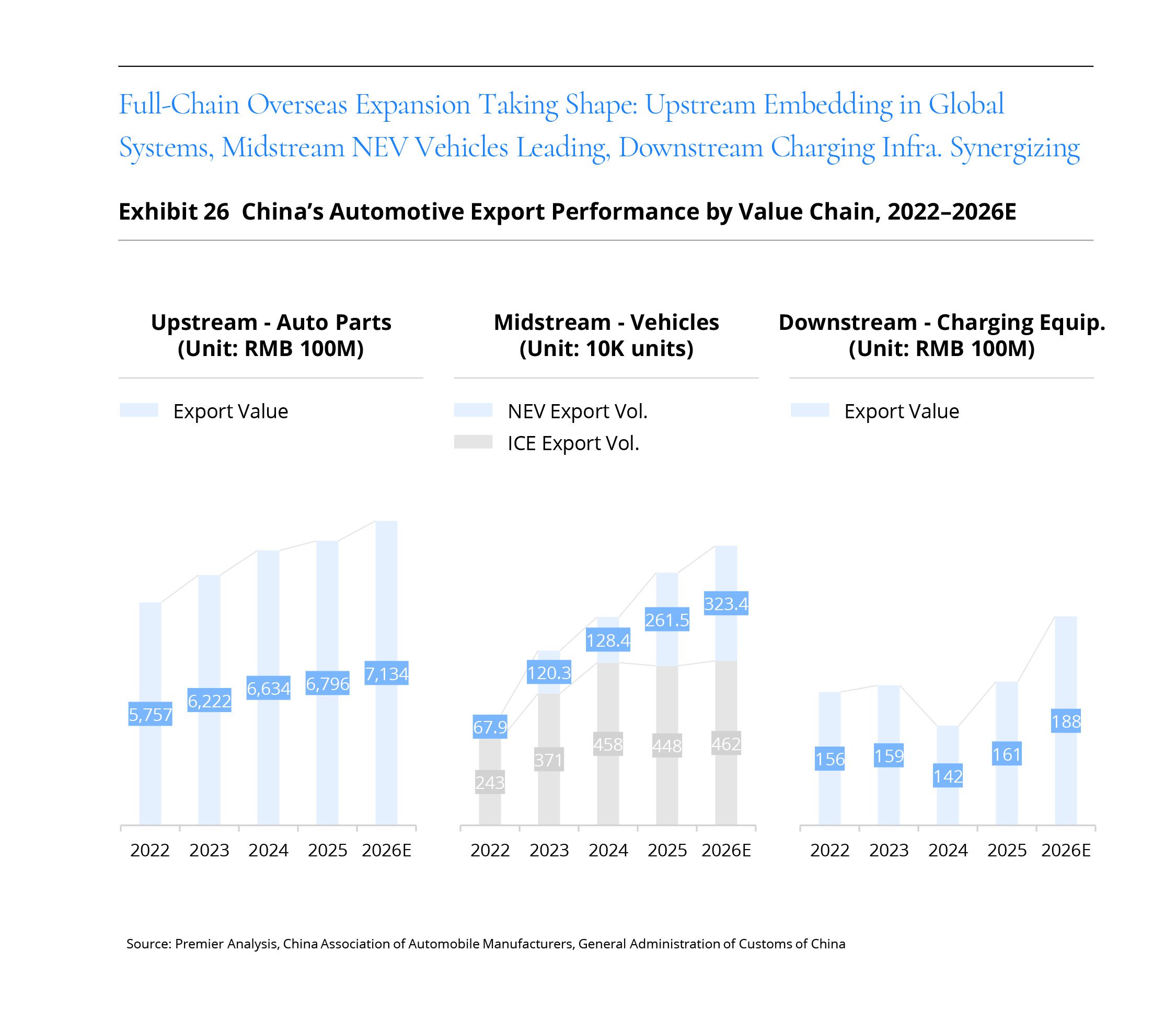

In recent years, China’s automotive export landscape has evolved from “scale expansion” to “structural optimization,” with upstream, midstream, and downstream segments driving a coordinated, systematic overseas push.

Upstream component manufacturers, leveraging cost advantages and technology upgrades, continue to deepen their integration into global supply chains; midstream vehicle exports, propelled by the NEV wave, have achieved leapfrog growth to become the core engine of Chinese manufacturing’s globalization; downstream charging/refueling and ancillary equipment exports are demonstrating strong extension potential as global electrification infrastructure buildout accelerates.

In the upstream components segment, the export structure continues to upgrade toward higher value-add. Key core components such as power batteries, electric drive systems, intelligent electronic controls, and thermal management systems have become the primary drivers of export growth, with certain sub-segments already occupying core positions in the global supply chain. Concurrently, traditional components including chassis systems, body structural parts, and electrical/electronic assemblies maintain stable output in terms of scale and maturity.

In the upstream components segment, the export structure continues to upgrade toward higher value-add. Key core components such as power batteries, electric drive systems, intelligent electronic controls, and thermal management systems have become the primary drivers of export growth, with certain sub-segments already occupying core positions in the global supply chain. Concurrently, traditional components including chassis systems, body structural parts, and electrical/electronic assemblies maintain stable output in terms of scale and maturity.

Midstream vehicle exports represent the most iconic growth segment in recent years. NEVs have become the primary incremental source of vehicle exports, with BEV and PHEV penetration rates rising rapidly across European, Southeast Asian, Latin American, and Middle Eastern markets.

On one hand, cost dilution effects from domestic market scale advantages give Chinese OEMs strong competitiveness in price-configuration combinations; on the other, first-mover accumulation in electrification and intelligent capabilities provides differentiated product advantages in range, intelligent cockpit, and driving assistance dimensions. The vehicle export mix is also progressively upgrading from low-end models to mid-to-high-end NEV offerings, with brand premium power beginning to materialize and the export logic transitioning from “supplementing capacity” to “strategic global deployment.”

In the downstream segment, EV charging and refueling equipment exports have grown significantly alongside the acceleration of global electrification infrastructure construction. Export volumes of charging stations, charging modules, integrated energy storage equipment, and related power electronics components continue to expand, with particularly rapid demand release in emerging markets and select European countries. Chinese enterprises have established strong overseas competitiveness through their mature expertise in charging technology standards, modular design, and cost control.

Furthermore, the export of “vehicle–charger–grid” integrated solutions signifies that Chinese companies are upgrading from single-equipment exporters to systematic energy solution providers. As the global NEV fleet continues to grow, charging and energy storage equipment exports are poised to become a significant profit extension domain across the future value chain.

Facing a new round of global industrial restructuring and trade landscape reshaping, the Chinese automotive industry’s overseas strategy is no longer a simple matter of “taking products abroad.” Only by achieving synergy across strategic pacing, organizational capabilities, and compliance systems can enterprises build truly sustainable global operational capabilities in the complex international competitive environment. To this end, Premier proposes a “Five-in-One” globalization strategy framework:

At the regional portfolio and market entry prioritization level, the core lies in establishing a “priority matrix” that dynamically sequences market entry based on key variables including market size potential, profitability structure, access barriers, and competitive intensity. Enterprises should preferentially select markets with “differentiated competitive space,” forming replicable blueprint pathways through product adaptation, channel integration, and supply chain optimization. Simultaneously, exit thresholds and resource reallocation triggers should be established so that when demand, policy, or exchange rate conditions deviate, the company can promptly consolidate its front, safeguarding overall capital efficiency. Through regional portfolio management, the risk of resource dilution from “blanket expansion” is avoided, achieving strategic focus.

Regarding market entry mode and channel architecture design, structured arrangements should be made according to different development stages. In the initial entry phase, general distributors or dealer groups enable rapid footprint establishment, achieving low-cost market testing and compliance landing; during the growth stage, pricing systems and brand experience consistency are reinforced through unified quotations, delivery standards, and service commitments to enhance brand control; in the mature stage, direct retail, online direct sales, or agency model reforms are progressively introduced to improve data visibility and end-customer reach efficiency. The key to channel design lies not in the superiority of any single model, but in the ability to dynamically iterate as market maturity evolves.

For aftersales and full-lifecycle service system development, a “service-first” philosophy should be upheld. Key cities require advance deployment of quick-repair networks, parts pre-positioning warehouses, and coordinated maintenance systems, with service efficiency enhanced through remote diagnostics, software upgrades, and online service platforms. Concurrently, quality closed-loop mechanisms and recall traceability systems should be established, embedding issue management into the brand operating structure. As overseas markets demand increasingly higher service experience standards, aftersales capability will become a critical pillar for brand trust and repurchase rates.

In terms of local manufacturing and trade barrier hedging, phased capacity deployment and local assembly (KD/CKD) strategies should be employed to flexibly respond to tariff and rules-of-origin changes. By setting capacity trigger conditions—using “order volume—policy certainty—cost advantage” as expansion thresholds—and simultaneously elevating quality management and supplier capability building, the structural risk of “capacity leading, delivery lagging” can be avoided. Local manufacturing is not merely a cost and tariff instrument but a long-term lever for integrating into local industrial ecosystems and enhancing policy stability.

At the localized technology capability and data compliance level, certification, security, and privacy-by-design should be front-loaded, with localized R&D and testing capabilities established. Through local data storage, local algorithm iteration, and cross-border data governance mechanisms, autonomous driving, connected vehicle, and software services are ensured to meet the regulatory requirements of different jurisdictions. Simultaneously, unified processes, logging, and version management systems should be established to achieve integrated management of product safety and compliance capabilities. Against the backdrop of strengthening global data sovereignty awareness, technology localization has become a prerequisite for entering high-standard markets.

From Value-Added to Value-Expansive,

Redefining China's Automotive

Value Horizon

Five Pivotal Roles Orchestrating

Glocal Organization Integration

Escaping the Value Trap

in the Intelligent Driving Era

25/26 PRMC Forward Mobility Index Review & Prospect

Intelligence in Motion,

Value Reimagined:

Automotive Industry Outlook 2026

Aug 02, 2026

Eight key trends help automakers stay focused on intelligent transformation and capability upgrading amid a rapidly reshaping industry, turning technology investment into scalable value and unlocking new growth in an increasingly competitive market.

Turbulent times, diverging trajectories.

In 2025, amid intensifying macroeconomic uncertainty and the normalization of supply chain disruptions, the global automotive industry maintained overall resilience, yet structural tensions became increasingly pronounced:

Weak demand recovery and subdued consumer confidence in Europe and the United States have made the chain of “slowing growth, excess capacity, and margin pressure” increasingly pronounced. By contrast, China’s economy has remained relatively resilient amid a broader adjustment in its growth model and ongoing structural upgrading. Under the overarching principle of pursuing progress while maintaining stability, China’s economic growth is gradually moving beyond the traditional factor-driven path and entering a new stage centered on innovation-led development and total factor productivity improvement. Meanwhile, China’s automotive market has continued to operate at a high level. Through export-driven growth and product mix upgrading, it has partly offset capacity pressure and become an important anchor for the rebalancing of global automotive supply and demand.

Meanwhile, new energy vehicle (NEV) penetration continued its steady ascent. Hybrid powertrains served as a vital buffer for both volume and profitability under transitional "technology—cost—charging infrastructure" constraints; power batteries and core components drove robust upstream expansion, while the aftermarket—including charging networks and auto finance—accelerated its penetration, collectively propelling the industry from "single-OEM competition" toward a paradigm of "full value chain, multi-profit-pool competition."

On the competitive landscape front, the industry is shifting from "scale-driven competition dominated by legacy OEMs" to "capability-led divergence competition". Legacy automakers still command the global volume and profit base, yet emerging players and leading Chinese OEMs are continuously reshaping cost curves and technology diffusion pathways through electrification platformization, accelerated intelligent iteration, and scaling overseas expansion.

Taking China as an example, BYD, Geely, and Chery have built stronger offensive-defensive capabilities through scale and broadened product portfolios, while Leapmotor, XPeng, and Xiaomi are reinforcing differentiation via intelligent user experiences and customer engagement—driving Chinese automakers’ migration from traditional profit pools toward new revenue streams defined by "software, service ecosystems, data, and experience," and increasingly contesting global standards and mindshare.

Looking ahead to 2026, industry evolution will converge around three principal themes:

First, electrification transitions from "penetration growth" to "structural substitution"—NEV models will continue to serve as the core incremental driver of exports and global expansion, particularly in emerging markets such as Brazil, Southeast Asia, and Africa, where the confluence of demand release and industrial policy will accelerate market opening;

Second, intelligent mobility enters the "capital-intensive + scale monetization" phase—AI investment is concentrating on autonomous driving, intelligent cockpits, and smart manufacturing. The competitive focus is shifting from feature stacking to systemic capabilities in data closed-loops, algorithm iteration efficiency, and hardware-software synergy, with the brand landscape entering an initial phase of consolidation and winner-take-more dynamics;

Third, corporate growth logic extends from "selling vehicles" to "cross-sector positioning"—strategic initiatives in future mobility and next-generation components will become new profit-pool entry points, with automakers accelerating capability spillover and business extension into low-altitude economy, intelligent manufacturing, and advanced materials.

Intelligence leads the leap; value finds its new frontier.

2026 is not merely a continuation of cyclical recovery—it represents a repricing window for the global automotive industry amid growth-model transitions and profit-pool redistribution.

Premier offers a strategic lens on eight key automotive trends shaping 2026, underpinned by critical charts and case analyses, to help automakers assess the landscape, set benchmarks, chart their course, and seize the competitive advantage at this pivotal juncture.

Shanghai

11/F · WSH Building

POLY GREENLAND PLAZA

198 Jingzhou Road

Shanghai PRC · 200082

London

OFFICE SUITE 29A · 3/F

23 Wharf Street

London England · SE8 3GG

Hongkong

9/F · Tower A

NEW MANDARIN PLAZA

14 Science Museum Road

Hongkong SAR · 999077