From the Illusion of “Democratization” to the Reality of “Disparity”:

Escaping the Value Trap

in the Intelligent Driving Era

From the Illusion of “Democratization” to the Reality of “Disparity”:

Escaping the Value Trap

in the Intelligent Driving Era

Taking value as the strategic lens, map the global industry landscape, pinpoint the pivotal links across the value chain, and uncover authentic consumer needs to identify resilient anchors of industry value—thereby enabling relevant companies to navigate the next chapter of intelligent mobility with greater clarity and conviction.

As the wave of intelligence surges, the global automotive industry is undergoing a profound transformation from "traditional manufacturing" to "intelligent mobility." The widespread adoption of technologies such as autonomous driving, smart cockpits, and intelligent connectivity seems to have fostered a facade of technological ubiquity—a "phenomenon of democratization." Yet, this facade masks a starker "reality of disparity": high-value strongholds—core algorithms, advanced chips, and data platforms—remain monopolized by the few, while the majority are trapped in a "low-value quagmire," struggling in a race to the bottom.

Against this backdrop, select Chinese intelligent driving enterprises are striving to break out of this Value Trap and explore new paths to disrupt the status quo. Represented by innovative forces like Pony.ai, these companies have achieved a secondary listing on the HKEX within the year through sustained technological breakthroughs and global commercial pilots. This not only demonstrates the growth potential of Chinese enterprises in the autonomous driving sector but also reflects the phased achievements of their upward climb within this "unequal" structure.

Nevertheless, capital markets are fickle, and short-term valuations do not constitute a solid moat. Chinese intelligent driving enterprises must penetrate the fog, lucidly identify their advantages and disconnects within the value chain, and promote the deep integration of technology and commerce to systemically break the fate of being trapped in low-value-added tiers.

Only by forging an autonomous and controllable "value highland" can they define the new rules of future competition and ascend as distinct luminaries on the global intelligent driving map.

On November 6, 2025, Pony.ai successfully completed its dual listing by landing on the Hong Kong Stock Exchange (HKEX) as "The Global First Robotaxi Stock," enjoying a moment of immense prestige.

However, the capital maneuvering of a dual listing failed to assuage the capital market's concerns regarding Pony.ai's profitability prospects. On its first day of trading in Hong Kong, Pony.ai's stock price broke its issue price, falling 12.95% from the offering price of HK$139. The capital market subsequently maintained a tepid response, with the stock price continuing to trend downward throughout the month.

Although the company raised over USD 1 billion through its dual listings in the US and Hong Kong—and explicitly allocated 50% of the net proceeds from the HK listing to advance large-scale commercialization—its model of long-term high investment with low output remains unsustainable. At the current cash burn rate, if commercial deployment falls short of expectations, the company will face renewed pressure for subsequent financing. Meanwhile, industry competition has entered a "white-hot" phase: domestic rivals WeRide and Baidu’s Apollo Go are accelerating their pursuit, international giants Waymo and Cruise are expanding aggressively, and traditional OEMs are entering the fray.

Pony.ai’s predicament profoundly reveals a distinct structural contradiction in the era of intelligent driving:

On one side is the "Consumer Democratization" brought by tech proliferation: Intelligent driving functions are reaching the mass market with unprecedented speed and breadth, bringing universally accessible experiences.

On the other is the brutal reality of "Industrial Value Disparity": Exorbitant R&D costs, prolonged commercialization pathways, and thin short-term profits have trapped the vast majority of enterprises in a value prison, making it difficult to achieve healthy profitability while promoting ubiquity.

Clearly, the industry is collectively experiencing a grueling transition from "cash-burning expansion" to "sustainable organic growth."

In this context, Premier aims to deconstruct this conundrum through a prismatic lens. By taking value as the path, mapping the global industrial landscape, positioning key links in the value chain, and discerning genuine consumer needs, we seek to find a solid anchor point for industry value. Furthermore, through the Intelligent Integrated Product Development (IPD) framework, we aim to achieve a bidirectional coupling of demand matching and value perception, assisting relevant enterprises in navigating the new journey of intelligent driving:

1. Intelligent Driving Carries High Value-Add Expectations:The reality gap highlights the disparity between Chinese and foreign enterprises

2. Decoding "Democratization" vs. "Disparity":Unclear demands and R&D misalignment

3. Essence of Intelligent Integrated Product Development: User-Driven, Value-First

SECTION1

Intelligent Driving Carries High Value-Add Expectations: The reality gap highlights the disparity between Chinese and foreign enterprises.

Differentiation in Tech Realization: Chinese Enterprises Approach Half of the Global Market

In recent years, the intelligent driving industry has collectively entered a new stage of development: technical capabilities are no longer limited to Proof of Concept (POC) or laboratory breakthroughs but are progressively moving towards scaled deployment and application in real-world scenarios. Whether it is the maturity of autonomous driving algorithms, the enhancement of computing power and sensor technologies, or the gradual relaxation of regulatory environments, the technical elements accumulated over the past years are now facing a critical moment of concentrated release.

With the continuous iteration and breakthroughs in intelligent driving technology, constructing a scientific and widely applicable classification system has become increasingly necessary. In this context, various countries have summarized multiple sets of grading standards based on their own industry practices. Among them, GB/T 40429-2021 "Taxonomy of Driving Automation for Vehicles" released by China's Ministry of Industry and Information Technology, and SAE J3016 "Taxonomy and Definitions for Terms Related to Driving Automation Systems for On-Road Motor Vehicles" released by SAE International, are the most widely used.

Although these two standards differ in specific definitions and details, their core classification basis revolves around the "human-vehicle relationship" and the "division of driving responsibility." This classification method based on responsibility and role division helps clarify the interaction boundary between the driver and the automated system, providing guidance for the further evolution and practical application of the technology.

According to these core frameworks, autonomous driving can be divided into the following six levels, covering the entire spectrum from manual driving to fully autonomous driving:

- L0 | No Driving Automation (Emergency Assistance): The vehicle does not possess any automation features; all driving tasks are performed entirely by the driver. The vehicle may offer warnings but no sustained vehicle control.

- L1 | Driver Assistance: The vehicle features a single automated system for either steering or acceleration/deceleration (e.g., Adaptive Cruise Control or Lane Keeping Assist). The driver must maintain control of the vehicle at all times and is responsible for all other driving tasks.

- L2 | Partial Driving Automation: The vehicle can control both steering and acceleration/deceleration simultaneously. However, the driver must remain alert and ready to take over driving tasks at any time. The system can execute tasks in specific environments (e.g., highways) but cannot replace the driver.

- L3 | Conditional Driving Automation: The vehicle can achieve fully autonomous driving in specific environments (e.g., traffic jams on highways). The driver does not need to monitor the environment continuously but must be prepared to take back control when requested by the system (fallback-ready user).

- L4 | High Driving Automation: The vehicle can perform all driving tasks and monitor the driving environment within a specific Operational Design Domain (ODD), such as urban environments. The driver does not need to intervene; the system can handle fallbacks autonomously within its ODD.

- L5 | Full Driving Automation: The vehicle is capable of performing all driving tasks under all conditions and environments that a human driver can manage, without the need for human intervention. This represents the ultimate form of future mobility.

Based on this classification, we observe a distinct stratification in the adoption of intelligent driving technologies. L2 autonomous driving solutions, as the core driver of "Intelligent Driving Democratization," have widely penetrated the passenger vehicle market in recent years, becoming a mainstream configuration. However, L3 and higher autonomous driving solutions remain in the early stages of commercialization; enterprises truly possessing L3 or L4 capabilities remain a minority in the industry.

In this context, Chinese and Western OEMs have chosen two distinctly different paths for intelligent driving implementation based on their respective market demands and resource advantages. Chinese OEMs generally adopt a strategy of "preemptive market layout and localized deployment," focusing on rapid accumulation of technical experience through independent R&D and commercial pilots. By collaborating with local governments, tech companies, and internet platforms, they accelerate the application of intelligent driving in major cities and core scenarios. This model allows Chinese OEMs to respond quickly to market demand and balance technical validation with scaled application.

In contrast, Western OEMs place greater emphasis on the "gradual advancement of technology and strict regulatory compliance." They rely on advanced perception systems and AI algorithms, verifying technological maturity through long-term, large-scale testing and data collection. Although this strategy results in a relatively slower commercialization process, it places a higher premium on system safety and reliability.

Benefiting from the chosen path of rapid realization, Chinese OEMs have steadily moved towards a leading position in the intelligent driving field. Their penetration rates in key dimensions such as autonomous driving, smart cockpits, and intelligent connectivity are already ahead of foreign OEMs. According to Premier's forecast, by 2025, Chinese OEMs will account for more than one-third of the global passenger vehicle market share. Furthermore, despite lagging in total volume, the sales of L2 passenger vehicles by Chinese OEMs (14.85 million) have already surpassed those of foreign OEMs (14.25 million), reaffirming Chinese leadership in the scaled application of lower-level intelligent driving solutions.

Looking ahead, Chinese OEMs are expected to solidify their lead in L2 penetration. Original L0 and L1 models will be upgraded to L2 solutions en masse. Between 2025 and 2030, the L2 penetration rate is projected to grow from 44% to 52%, exceeding half of the market. While the L2 penetration rate of Western OEMs will rise to 40%, they are expected to retain a significant volume of L0 models.

In the realm of high-level autonomous driving, Chinese OEMs are expected to initiate L4 commercial deployment by 2030 and achieve large-scale application around 2035. The key milestones for L5 are projected to be 2040 and 2045, respectively. Driven by sustained policy support, rapid technical iteration, and market expansion, Chinese OEMs are expected to further widen the gap with Western OEMs in this domain, maintaining a lead of several years.

Four Key Technical Architectures Enabling Intelligent Driving: Imbalance in Critical Technology Ownership

In the technical domain, as intelligent driving evolves from L0 to L2/L3, the on-board intelligent driving modules have matured, evolving into a system constructed of four key modules: the Perception Layer, Transmission Layer, Decision Layer, and Execution Layer. Each layer plays a vital role:

- Perception Layer: Collects and fuses environmental and vehicle status information through multi-source sensors to construct a structured cognitive map of the external environment and the vehicle's pose. Key components include cameras, LiDAR, millimeter-wave radar, high-precision maps, and navigation systems.

- Transmission Layer: Responsible for the low-latency, high-reliability transmission of data, instructions, and status information between units, ensuring real-time coordinated system operation. Key components include C-V2X, high-speed connectors, vehicle telematics (TSP), communication modules, and cloud services.

- Decision Layer: Based on perception and positioning results, this layer understands and predicts traffic scenarios to formulate driving trajectory plans that meet safety and efficiency standards. Key components include computing platforms, operating systems, automotive-grade chips, intelligent driving algorithms, and domain controllers.

Execution Layer: Converts the output from the decision layer into precise control of the powertrain and handling systems, achieving stable, predictable, and safe vehicle motion. Key components include drive-by-wire chassis, chassis domain controllers, power batteries, electronic control systems, and electric drive systems.

These four layers of technical architecture are transmitted level by level and combined organically. This integration allows functions we are now familiar with—such as Adaptive Cruise Control (ACC), Pedestrian Detection, Collision Avoidance, and Cross-Traffic Alert—to be realized with the aid of technical solutions like millimeter-wave radar, HD cameras, and LiDAR.

However, despite significant progress by Chinese enterprises in multiple technical fields and partial realization of domestic substitution, foreign companies still firmly hold technical advantages and discourse power in certain critical components, particularly high-end sensors and algorithmic platforms.

Taking sensors as an example, while Chinese enterprises like Huawei and Baidu have made breakthroughs in LiDAR and millimeter-wave radar—possessing advantages in cost control and market promotion—international brands such as Velodyne and Bosch still dominate in terms of precision, stability, and large-scale application capabilities.

In the field of intelligent driving algorithms and data processing platforms, companies like Tesla and Mobileye maintain a sustained industry advantage due to robust R&D investment and global data accumulation. Although Chinese enterprises like Momenta and Pony.ai have achieved breakthroughs in algorithm optimization and autonomous driving technology, Western enterprises remain ahead in global data support and algorithm optimization capabilities.

As the intelligent driving market expands, despite Chinese enterprises holding advantages in technology adoption speed and market share, they are expected to face technical challenges and intense competition from foreign enterprises in the commercialization of high-level autonomous driving technologies and innovative applications.

Financial Performance: Asymmetry in Financial Health Between Chinese and Foreign Enterprises

While the accumulation of intelligent driving technology continues to deepen, financial risks have not been effectively mitigated. Taking Pony.ai as a case study: in the first three quarters of 2025, the company recorded a total cumulative revenue of USD 60.88 million, a year-on-year increase of 54.1%. While this appears to represent a significant expansion in business scale, core profitability indicators have continued to deteriorate.

Specifically, the Net Loss reached USD 157 million, widening by 68.9% year-on-year; the Net Profit Margin was recorded at -258.5%, a year-on-year expansion of 22.6%. The magnitude of losses far exceeds the growth rate of revenue, reflecting that the company's cost control capabilities have yet to match the pace of its business expansion.

From the perspective of Cost Structure, soaring R&D investment is the core driver of expanding losses. R&D expenses in the first three quarters reached USD 144 million (approx.), accounting for over 230% of total revenue. This figure underscores the brutal reality of the autonomous driving industry where "technological iteration equals survival." To maintain a leading position in intelligent driving technology, companies must continuously invest heavily in core areas such as sensor fusion, algorithm optimization, and simulation platform construction.

Simultaneously, as an upstream solution provider, the company faces the risk of inequality in customer structure and Bargaining Power during the commercialization process. Once high dependency forms on key solutions or ecosystem partners, the company will be significantly constrained in price negotiations, the pace of technological evolution, and strategic choices. In a fiercely competitive environment, exchanging price for short-term scale may accelerate functional adoption but risks further compressing already thin profit margins.

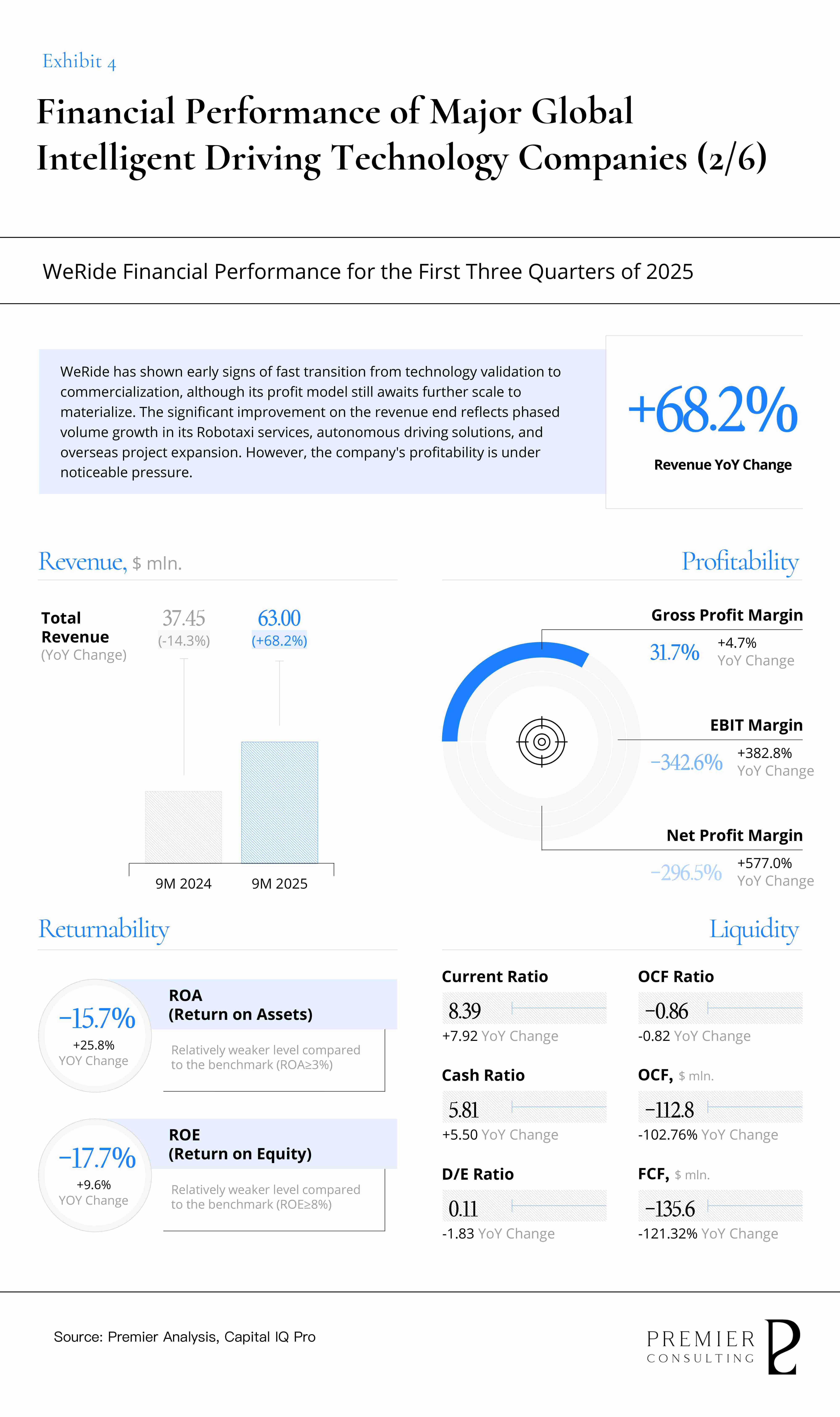

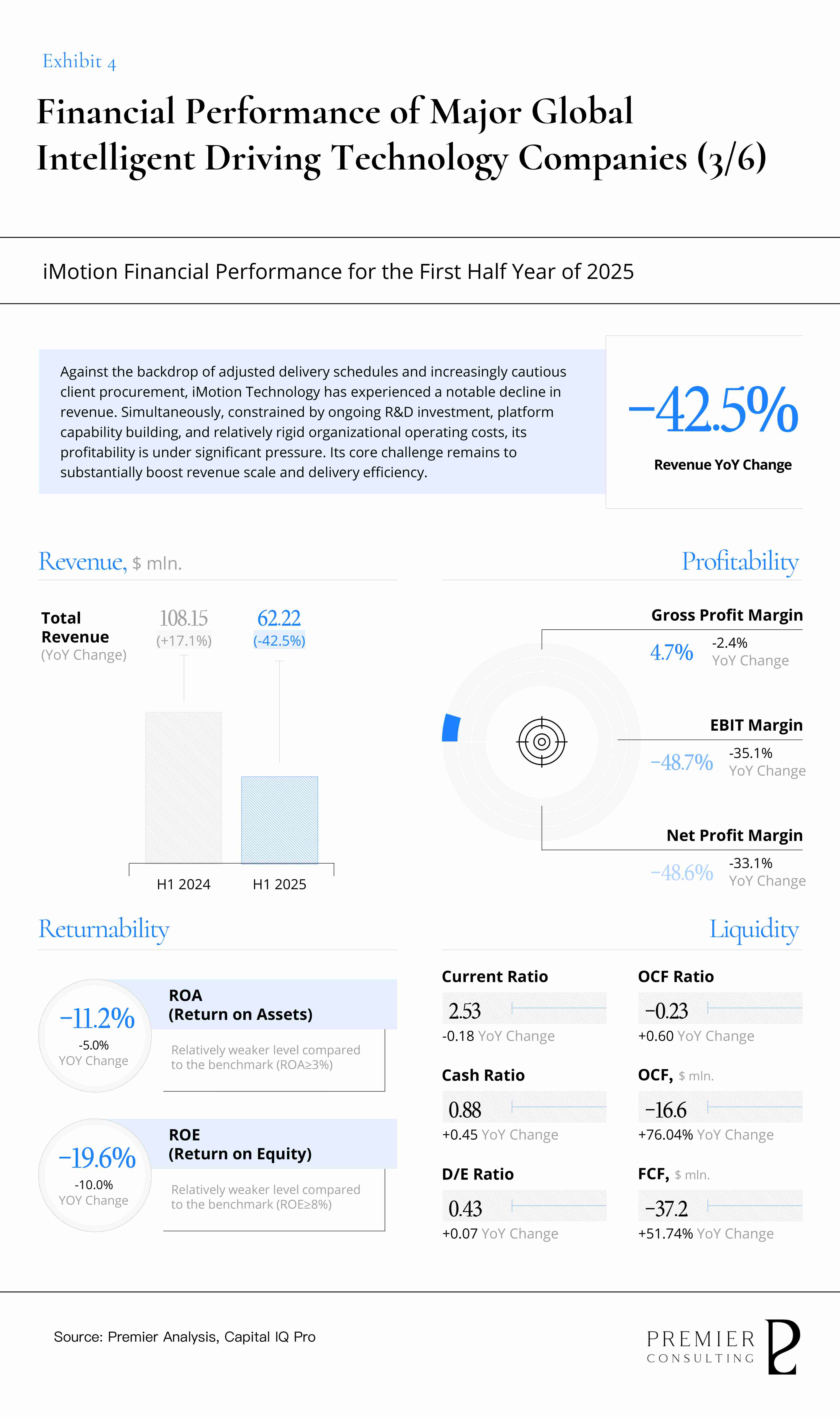

Observing other domestic players in the intelligent driving sector—WeRide and iMotion, their financial performance generally exhibits the characteristic of "Revenue Surge, Profit Decline." WeRide has achieved phased growth in Robotaxi, autonomous driving solutions, and overseas market expansion, significantly improving its revenue profile. However, due to continued heavy investment in overseas markets, profitability remains under significant pressure. iMotion has seen a notable retraction in revenue due to adjustments in delivery pacing and cautious procurement by clients. Meanwhile, sustained R&D investment, platform capability construction, and relatively rigid operating costs continue to weigh heavily on profitability.

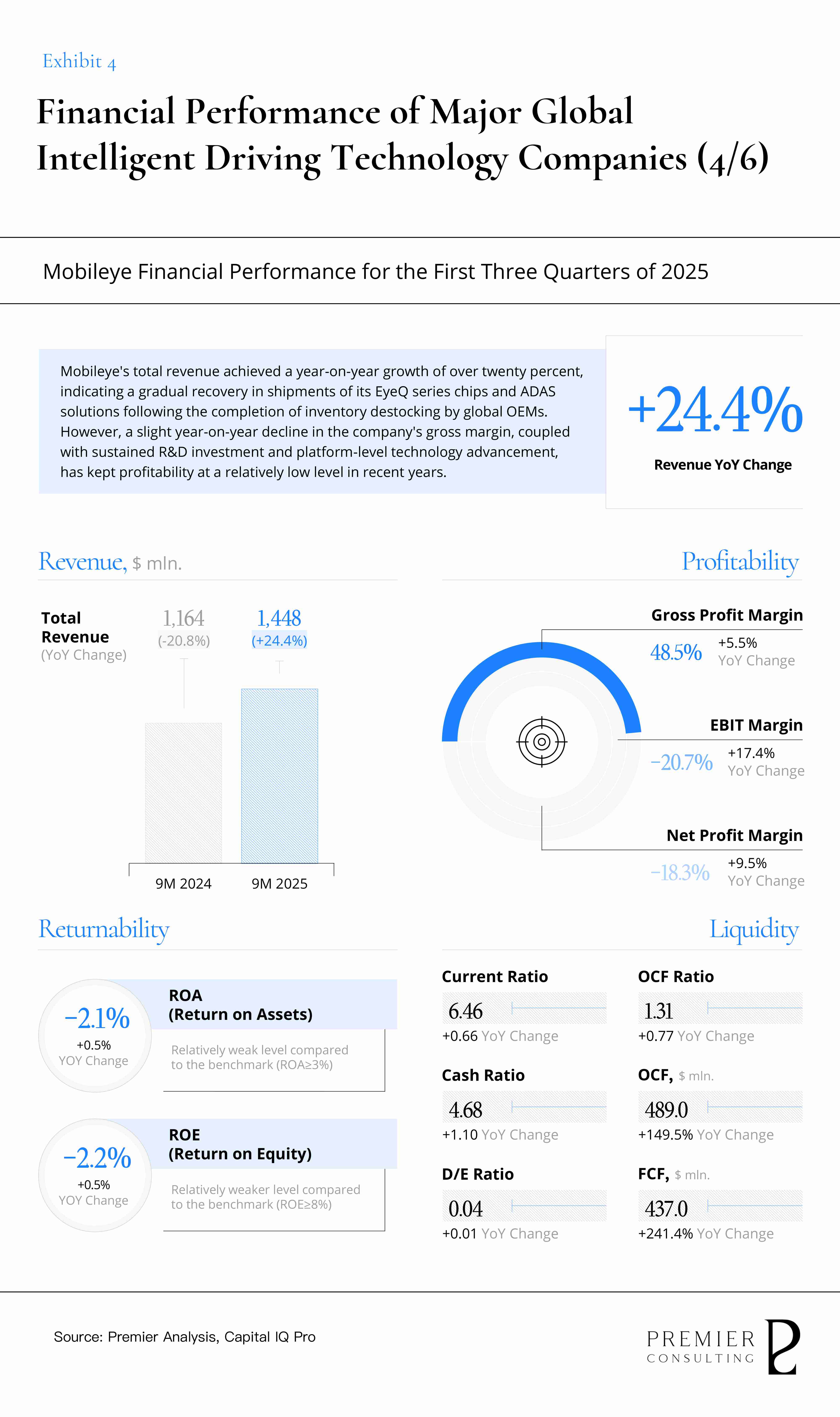

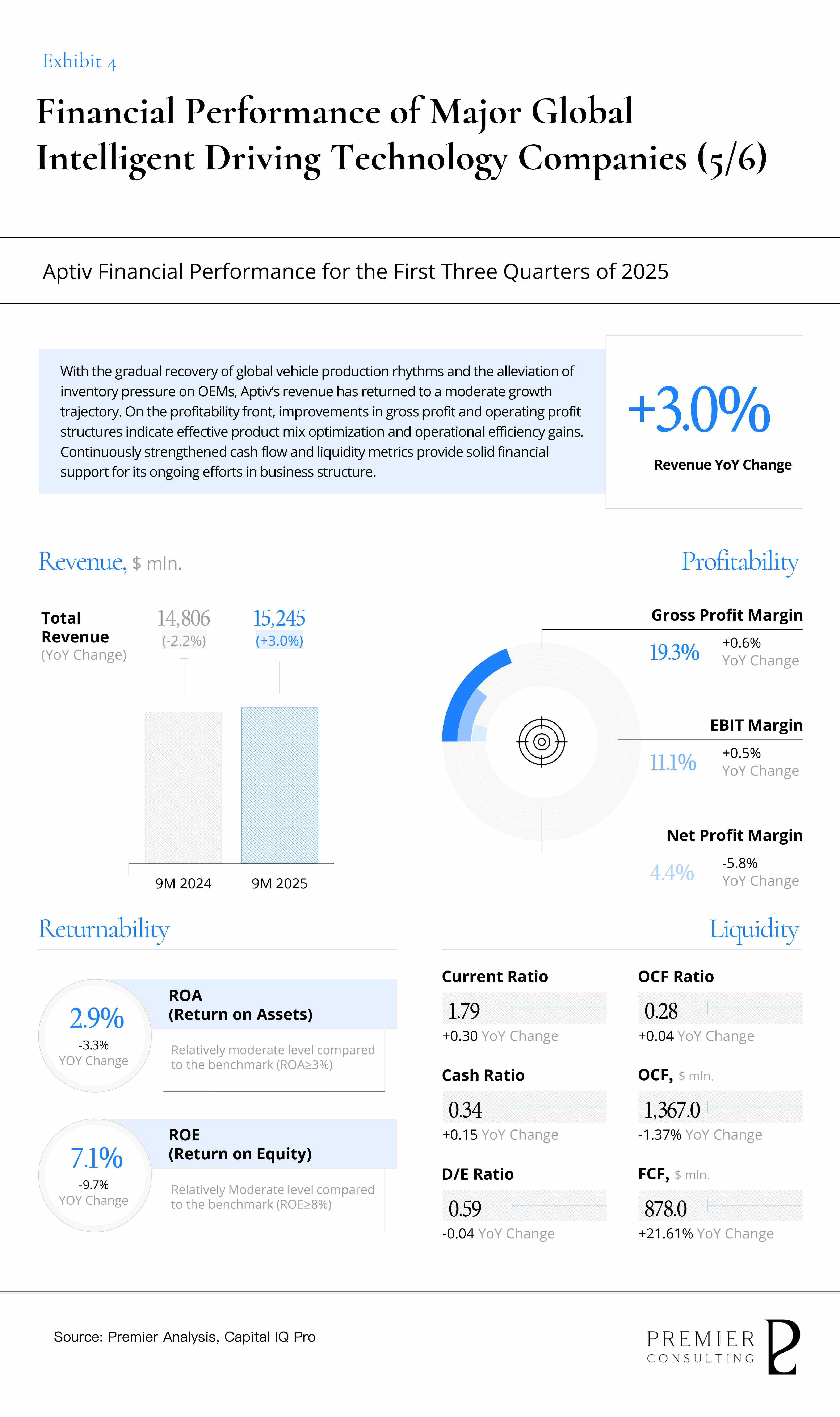

In contrast, foreign intelligent driving companies represented by Mobileye, Aptiv, and Valeo have seen a recovery in recent financial performance, benefiting from solid order backlogs, robust client partnerships, and significant first-mover advantages.

Mobileye total revenue grew by over 30% year-on-year, reflecting a gradual recovery in chip shipments following inventory destocking by OEMs. However, gross margins dipped slightly year-on-year, indicating that sustained R&D investment and platform technology advancement keep profitability at a lower level.

Aptiv returned to a moderate growth trajectory through the recovery of global vehicle production and the alleviation of inventory pressure on OEMs. Its gross profit and operating profit structures have improved, reflecting the results of product portfolio optimization and operational efficiency enhancements.

While advancing its transformation strategy towards electrification and green technology, Valeo has steadily increased its gross margin and EBIT margin, striving to optimize internal resource allocation to cope with external market uncertainties.

Stock Performance: The Disconnect Between Capital Confidence and Valuation Logic

The divergence in performance between Chinese and foreign intelligent driving enterprises is further corroborated in the secondary market.

As of the close on December 26, the PRMC Forward Mobility Index closed at 1,539.59 points, a cumulative year-to-date increase of 152.54 points (11.00%). This performance was primarily driven by the rapid rise of the upstream sector, with the PRMC FM Supply Index rising 320.77 points cumulatively for the year (31.30%), closing at 1,345.67 points.

However, as a crucial component of the upstream sector, the stock performance of intelligent driving companies shows distinct differentiation. Observing year-to-date price movements: among the three Chinese enterprises, only Pony.ai recorded a gain (4.25%), while WeRide and iMotion saw their share prices fall by 38.58% and 65.53% respectively from the beginning of the year. Conversely, foreign enterprises Valeo and Aptiv recorded strong gains of 28.08% and 27.17%, respectively.

Analyzing performance since 2020, the stock prices of Valeo, Aptiv, and Mobileye have been relatively stable, exhibiting a "Performance-Based" valuation logic, reflecting their robust business operations and broad market recognition. In contrast, Pony.ai, WeRide, and iMotion—due to their smaller scale and being in the business expansion phase—lack solid financial performance to support valuation. Their stock prices exhibit an "Event-Driven" valuation logic, typically fluctuating significantly in response to major events such as commercial partnerships, capital operations, or new product/technology releases.

Notably, in February 2024, global GPU giant NVIDIA disclosed its latest 13F filing, explicitly mentioning a holding of 1,738,563 American Depositary Shares (ADS) of WeRide, valued at approximately USD 24.65 million. This move was interpreted as a significant investment endorsement, triggering a follow-on effect from global investors and a massive capital inflow. However, WeRide failed to consolidate this market sentiment through steady earnings, leading to a sharp retracement in share price over the following months, reflecting the gap between market expectations for short-term performance and actual results.

A similar situation occurred with Pony.ai. Since the beginning of the year, announcements regarding cooperation with the Stellantis Group to operate Robotaxis in Europe and obtaining autonomous driving test permits in multiple cities temporarily stimulated stock price increases. However, the subsequent correction indicates significant volatility in market expectations regarding its short-term performance.

Synthesizing financial and stock performance, it is evident that only by achieving scaled positive operating cash flow and converting it into sustainable profitability can enterprises win deep trust in the capital market. Capital market recognition relies not only on short-term capital maneuvering or market hype but fundamentally on robust operations and continuous profit growth. Only by steadily advancing technological innovation and business expansion can enterprises consolidate confidence in fierce competition, attracting more attention and ultimately realizing the true value of intelligent driving in their share price.

Downstream Sector Unleashing Incremental Value: Imbalance in Profit Pool Value Density

As a complex industrial chain interwoven with upstream, midstream, and downstream links, every segment of the automotive industry is inextricably linked to the concept of intelligent driving. In this context, how Chinese enterprises precisely select strategic entry points and meticulously lay out their plans to secure a position in this incremental market will be key to realizing long-term value.

According to Premier's forecast, the global automotive industry's total Profit Pool will reach RMB 3.1 trillion in 2025.

The profit pool of Upstream Sector is RMB 917.2 billion (29%). Currently, profits are concentrated in traditional components such as internal combustion engine powertrains, chassis systems, and electrical/electronic systems.

However, as intelligent driving commercialization advances, its contribution to the profit pool is emerging, especially in sub-sectors like High-Level Driver Assistance, Autonomous Driving, and Automotive Software & Systems. Intelligent driving contributes up to 45% to the profit pool of new component sub-sectors, expected to be the main driver of future upstream growth.

The profit pool of Midstream Sector is RMB 1,065.6 billion (34%). Although ICE models remain the primary profit source, profit growth from BEVs and Hybrids has accelerated significantly due to increased consumer demand for environmental sustainability and intelligence. Hydrogen models, despite policy support, remain limited in profit scale due to technological maturity and slow commercialization.

Downstream Sector is the largest portion of the profit pool, reaching RMB 1,115.6 billion (37%). This sector also has the highest contribution from intelligent driving, particularly in Mobility-as-a-Service (MaaS) and Aftermarket Services.

Sub-sectors such as On-Demand Mobility, Low-Altitude Economy, Data Interconnectivity, and Subscription Services are closely related to intelligent driving. With the ubiquity of AD technology, the profit pools of these sectors will expand continuously. Meanwhile, traditional sub-sectors like tires and body parts face pressure from functional standardization and margin compression, losing market share to technology-driven innovative products.

In summary, as intelligent driving gradually becomes the new growth engine for the global automotive value chain's profit pool, deep reflection on its strategic significance is paramount. With the "14th Five-Year Plan" in China providing policy support, the structural change will accelerate over the next five years. Future profit pools will rely more on technology-driven innovation capabilities and the improvement of Total Factor Productivity (TFP).

Enterprises that can achieve breakthroughs in core intelligent driving technologies while accelerating their layout in downstream services stand to gain continuous incremental value. The opportunity for Chinese enterprises lies in redefining the automotive value chain in the global market, seizing the dual dividends of technological innovation and consumption upgrades to achieve leapfrog development.

SECTION2

Decoding "Democratization" vs. "Disparity":

Unclear demands and R&D misalignment.

In the race for intelligent driving, enterprises act as artisans, weaving unique driving experiences with sophisticated intelligent functions. However, whether these innovations can cross the market threshold depends on consumer cognition and choice.

Intelligent Appeal Occupies Consumer Mindshare: Asymmetry in Product Attribute Value Perception

To deeply understand global automotive consumer purchasing decisions, Premier conducted the 2025 Global Automotive Consumer Behavior Study. Based on this research, we categorized consumer value perception of various attributes into four types:

- Attractive: Significantly enhances value perception; absence does not lower value.

- Performance/Expectation: Value perception correlates linearly with performance.

- Must-be: Basic requirement; absence causes significant value drop.

- Indifferent: Minimal impact on value perception.

As core elements of vehicle electrification, battery systems and electronic control systems are perceived by Chinese consumers as “must-have” and “performance” attributes, whereas consumers in Southeast Asia and Europe tend to view them as largely “indifferent.” This divergence highlights meaningful regional differences in the acceptance of electrification technologies, shaped by factors such as market maturity, the strength of policy incentives, and varying levels of awareness around sustainable consumption.

In the domain of vehicle intelligence—particularly advanced driver-assistance systems, intelligent cockpits, and connected features—Chinese consumers exhibit a markedly stronger preference. Notably, driver-assistance functions are regarded as a “delighter” only in China, while consumers in other regions classify them merely as “performance” attributes. This suggests that Chinese consumers’ expectations for intelligent features have moved beyond basic safety and convenience, positioning them instead as key contributors to driving experience enhancement and brand value perception.

A similar pattern emerges in interior design. Only Chinese consumers identify interior design as a “delighter,” reflecting an ongoing upgrade in consumption mindset. Attention is gradually shifting away from fundamental vehicle performance and functionality toward aesthetics and design quality, alongside a growing demand for refined craftsmanship and premium detailing.

Taken together, these regional differences in expectations around electrification, intelligence, and design aesthetics are driving increasingly differentiated approaches to product positioning, technology development, and go-to-market strategies across regions. To compete effectively on a global scale, automakers must develop a nuanced understanding of local demand characteristics and tailor their product and marketing strategies to address the diverse value priorities of different regional markets.

Coexistence of Demand Saturation and Value Reshaping: Mismatch Between Willingness to Pay (WTP) and Budget Spending

A closer examination of changes in Chinese consumers’ willingness to pay and budget allocation across vehicle attributes between 2024 and 2025 reveals several noteworthy trends.

First, willingness to pay and budget allocation for advanced driver-assistance systems, intelligent cockpits, and connected-vehicle functions have risen markedly, reflecting sustained growth in demand for intelligent and connected driving experiences. As intelligent technologies continue to mature, consumers are paying increasing attention to in-vehicle digitalization and smart interaction. Driving intelligence and connectivity have become core considerations in purchase decisions, and this trend is likely to persist as consumers place greater value on efficient, convenient, and technologically enhanced driving experiences.

First, willingness to pay and budget allocation for advanced driver-assistance systems, intelligent cockpits, and connected-vehicle functions have risen markedly, reflecting sustained growth in demand for intelligent and connected driving experiences. As intelligent technologies continue to mature, consumers are paying increasing attention to in-vehicle digitalization and smart interaction. Driving intelligence and connectivity have become core considerations in purchase decisions, and this trend is likely to persist as consumers place greater value on efficient, convenient, and technologically enhanced driving experiences.

Second, the increase in willingness to pay for electronic control systems points to a growing focus on driving feel and vehicle dynamics. With the ongoing advancement of electrification and intelligence, electronic control systems—critical to improving handling precision, ride stability, and overall driving quality—have emerged as a key value proposition, particularly in higher-end models.

In addition, rising willingness to pay for interior design underscores Chinese consumers’ increasing emphasis on vehicle aesthetics and personalization, consistent with its classification as a “delighter” attribute. As consumer mindsets continue to upgrade, interior design is no longer viewed merely as a functional component, but rather as an expression of personal taste, lifestyle, and identity.

By contrast, willingness to pay and budget allocation have declined for certain attributes, notably battery systems and integrated lighting. As electric vehicle technologies mature, consumer expectations around battery performance—such as power output and driving range—have largely been met, leading to a normalization of perceived value. Similarly, integrated lighting solutions have reached a level of technological maturity, resulting in more stable demand and a contraction in incremental spending.

The decline in willingness to pay for video and display features as well as online content suggests that Chinese consumers’ acceptance of the “car as a third living space” concept remains limited. While automakers have sought to position vehicles as extensions of living and working environments, demand for in-vehicle entertainment and multimedia services is still at an early stage and has yet to translate into higher spending intentions.

For automakers, these trends highlight the importance of guarding against the risk of “overdevelopment” amid rapid technological iteration. Rather than indiscriminately following high-frequency innovation cycles, manufacturers must critically assess true market demand and strike a disciplined balance between technological ambition and consumer value realization, avoiding excessive investment that fails to generate proportional returns.

Brand Reputation and Driving Experience Dominate Decisions: Inconsistency in Global Selection Factors

In actual purchase decisions, global consumers consistently view brand reputation and driving experience as the primary drivers of vehicle choice. Brand reputation reflects trust in a manufacturer’s heritage, credibility, and long-term value, while comfort and stability in driving and handling define the quality of everyday use. As demand for intelligence and design continues to rise, consumers are placing greater emphasis on technological innovation and personalization, making the sophistication of intelligent features and exterior design increasingly important reference points in modern vehicle selection.

Chinese consumers exhibit particularly high expectations regarding brand reputation and intelligent feature configurations. Brand image has become a critical consideration in the decision-making process, while the rapid diffusion of intelligent technologies and ongoing innovation have significantly strengthened preferences for smart functions. By contrast, demand for after-sales services remains at an early stage. With maintenance, charging, and related infrastructure now widely established across China, basic service needs are largely perceived as adequately met.

Chinese consumers exhibit particularly high expectations regarding brand reputation and intelligent feature configurations. Brand image has become a critical consideration in the decision-making process, while the rapid diffusion of intelligent technologies and ongoing innovation have significantly strengthened preferences for smart functions. By contrast, demand for after-sales services remains at an early stage. With maintenance, charging, and related infrastructure now widely established across China, basic service needs are largely perceived as adequately met.

Consumers in Southeast Asia tend to place greater emphasis on value for money, reflecting a strong focus on practicality and affordability. Given relatively lower income levels and a less mature automotive market, demand for advanced intelligent features remains more conservative. However, as electrification and intelligent technologies gradually penetrate these markets, related consumer demand is expected to rise meaningfully over time.

Consumers in Europe and the Americas place greater weight on the vehicle delivery experience and after-sales services, while showing comparatively lower demand for electrification and intelligent technologies. These markets continue to prioritize traditional automotive values, driving enjoyment, and comfort—particularly in terms of handling and overall driving feel. Although intelligent technologies are becoming more widespread, consumer expectations remain moderate, with a preference for vehicles that deliver stability and high-quality driving experiences rather than those that pursue technological novelty alone.

By conducting an in-depth analysis of the findings from the Global Automotive Consumer Behavior Study 2025, this report not only sheds light on how consumers perceive the value of intelligent driving functions, but also provides insight into the future trajectory of their importance in consumer decision-making. For automakers, the ability to accurately anticipate and respond to these shifts—while proactively investing in emerging mobility models, intelligent connectivity, and personalized services—will be critical to securing competitive advantage and establishing long-term market leadership on a global scale.

SECTION3

Essence of Intelligent Integrated Product Development:

User-Driven, Value-First

“Intelligent driving for all” is rapidly becoming the industry norm. Yet long-term corporate survival ultimately depends on how each player defines its own path. As waves of mass adoption blur competitive boundaries, the true point of divergence lies in who can remain clear-headed amid the noise and complete the critical leap from reacting to change to actively shaping change.

This leap goes beyond technological catch-up; it requires a fundamental reconfiguration of the product innovation system and the underlying logic of value creation.

In response, Premier introduces the CAPE IPD (Intelligent Integrated Product Development) framework to provide systematic support for this pivotal transition. Anchored in the core strategy of user-driven, value-first development, CAPE IPD activates a coordinated rotation of four critical capability dimensions, ensuring that strategic foresight is translated into executable development roadmaps. By integrating fragmented intelligent capabilities into a collaborative innovation ecosystem, the framework enables enterprises to proactively define the competitive arena and secure long-term growth.

Within this framework, the UserVantage Excellence Principles serve as a concrete guiding beacon for strategic decomposition and are deeply integrated with the CAPE agile doctrine. Together, they activate the four key capability dimensions. By placing user needs at the center and focusing on deep value creation, the UserVantage principles align tightly with the full lifecycle of intelligent product development. They simultaneously ignite the dual engines of product innovation and commercialization, embedding a strong fit between product innovation and market demand, and ultimately enhancing an automaker’s distinctive competitiveness and sustainable value creation potential in the intelligent automotive industry.

Within this framework, the UserVantage Excellence Principles serve as a concrete guiding beacon for strategic decomposition and are deeply integrated with the CAPE agile doctrine. Together, they activate the four key capability dimensions. By placing user needs at the center and focusing on deep value creation, the UserVantage principles align tightly with the full lifecycle of intelligent product development. They simultaneously ignite the dual engines of product innovation and commercialization, embedding a strong fit between product innovation and market demand, and ultimately enhancing an automaker’s distinctive competitiveness and sustainable value creation potential in the intelligent automotive industry.

1. Excellence in User-Centric Deep Insight

The user-oriented approach of precise guidance requires all product strategies and decisions to be closely aligned with user needs. Through scientific data modeling and forward-looking market insights, it deeply understands unmet user needs, enabling the transition from early product concepts to innovative implementation, thereby achieving a competitive advantage ahead of the market.

Core Initiatives:

- Integrate behavioral data, market trends, and third-party insights to form a lifecycle-spanning data model.

- Deploy AI agents to extract latent pain points and opportunities, enhancing demand prediction accuracy.

- Accelerate new feature validation and commercial potential assessment through rigorous scenario modeling.

- Combine quantitative and qualitative methods to distill emotional drivers from consumer behavior models.

- Develop a dynamic insight matrix to maximize value alignment across specific user segments.

2. Excellence in Value-Driven, Market-Led Innovation

Innovation-driven value creation emphasizes dual breakthroughs in both technology and commercial value. Market leadership requires innovation not only to lead on the technological frontier, but also to be rapidly translated into tangible market advantages and sustainable commercial returns, positioning products as benchmarks of value in competitive landscapes.

Core Initiatives:

- Establish a priority system for market potential to align R&D focus with maximum value creation.

- Leverage Generative AI and agentic AI to expand design space exploration and efficiency.

- Implement mechanisms to balance resource allocation between long-term R&D and short-term yield.

- Ensure technical breakthroughs have a clear, rapid path to commercialization.

- Foster synergetic innovation across technology, marketing, and operations teams.

3. Excellence in Smart Collaboration, Enhancing Product Development Efficiency

Intelligent collaboration calls for breaking down organizational silos through digital platforms and cross-functional coordination mechanisms, thereby enhancing efficiency and alignment in product development. In the context of intelligent product development, collaboration extends beyond communication to become a capability for data-driven, tool-enabled, real-time collective decision-making.

Core Initiatives:

- Enable real-time data sharing and process linkage across R&D, manufacturing, supply chain, and sales channels.

- Enforce standardization to drastically shorten integration testing time across teams.

- Implement a closed-loop quality enhancement system from simulation to vehicle validation.

- Utilize AI to optimize cross-departmental task coordination and priority matching.

- Continuously refine development efficiency using real-project data feedback.

4. Excellence in Continuous Innovation & Adaptation

Sustained innovation requires organizations to remain dynamic in the face of rapidly evolving technologies and market conditions, while agility emphasizes the ability to swiftly recalibrate strategy, organizational structures, and product direction—ensuring that innovation functions as a dynamic capability rather than a static outcome.

Core Initiatives:

- Implement agile lifecycle management to achieve rapid iteration and closed-loop market feedback.

- Build strategic robustness through real-time monitoring of market signals and performance metrics.

- Accelerate the innovation validation cycle through strategic pilot testing.

- Predict and respond to external shifts in policy, supply chain, and technology.

- Establish cross-departmental groups to drive swift internal decision-making and execution.

5. Excellence in Global Vision, Building Sustained Competitiveness

A global perspective calls for moving beyond a purely local-market lens to design products and business models informed by worldwide strategic dynamics and regional differentiation. Enduring competitiveness is built on globally adaptable capabilities, sustainable value creation, and cross-market learning mechanisms.

Core Initiatives:

- Formulate cross-regional landing strategies based on deep analysis of local competitive environments.

- Enhance cross-market learning capabilities to leverage innovation globally.

- Design architectures ready for localization to improve global deployment efficiency.

- Co-construct value networks with overseas partners.

- Track long-term ecosystem value and strategic outcomes to ensure enduring competitiveness.

Furthermore, Premier empowers the intelligent transformation through the AI-driven engine, CAPE AInspire, which integrates smart capabilities across all stages, ensuring a seamless connection from strategic conception to product implementation. This enables businesses to achieve leapfrog development in their digital transformation, driving continuous value creation and solidifying their market leadership.

In market management, through in-depth market forecasting, intelligence analysis, and pricing optimization, businesses gain precise insights into consumer needs and market trends, enabling the formulation of effective commercial strategies. By leveraging big data and AI algorithms, real-time market monitoring and dynamic pricing adjustments are achieved, ensuring businesses remain at the forefront of rapidly evolving markets.

In technology R&D and shared management, intelligent collaboration and automation tools enhance cross-department and cross-regional innovation efficiency and resource integration. By breaking down information silos and accelerating the R&D process, real-time feedback optimizes decision-making, ensuring alignment between technological innovation and market demand.

In product development management, AI-driven design and development cycle optimization automate the rapid iteration of products from concept to prototype, accelerating market validation and product launch. Leveraging intelligent tools, businesses can quickly identify and adjust shortcomings in product design, ensuring new products meet changing market demands at the fastest pace.

SECTION4

Closing Remarks

The "Phenomenon of Democratization" in intelligent driving is either a grand narrative painted by capital or the solid soil of tangible commerce.

Time remains silent, yet it relentlessly pushes waves of contenders to succeed one another, discarding the old for the new.

Enterprises represented by Pony.ai have forged technology into a hammer and business models into an anvil, shaping a striking capital landscape. Yet, a deep scrutiny of their financial musculature reveals scars that invite hesitation and profound reflection.

From the "Phenomenon of Democratization" to the "Reality of Disparity," what Chinese intelligent driving enterprises must truly break through is far more than technology itself. The true breakthrough lies in leveraging continuous, iterative technological breakthroughs to penetrate the inherent barriers of the value chain, achieving tangible commercial contributions that are evergreen and sustainable.

When the tide rises, the masses chase the frothing waves;

But those anchored by Value navigate the depths with quiet resolve.

The spray is ephemeral, vanishing with the wind.

Yet, when the clamor fades to silence,

It is the keel—forged in resilience and depth—

That bears the weight of a certain future.

From Value-Added to Value-Expansive,

Redefining China's Automotive

Value Horizon

Five Pivotal Roles Orchestrating

Glocal Organization Integration

From the Illusion of “Democratization” to the Reality of “Disparity”:

Escaping the Value Trap

in the Intelligent Driving Era

Aug 02, 2026

Taking value as the strategic lens, map the global industry landscape, pinpoint the pivotal links across the value chain, and uncover authentic consumer needs to identify resilient anchors of industry value—thereby enabling relevant companies to navigate the next chapter of intelligent mobility with greater clarity and conviction.

As the wave of intelligence surges, the global automotive industry is undergoing a profound transformation from "traditional manufacturing" to "intelligent mobility." The widespread adoption of technologies such as autonomous driving, smart cockpits, and intelligent connectivity seems to have fostered a facade of technological ubiquity—a "phenomenon of democratization." Yet, this facade masks a starker "reality of disparity": high-value strongholds—core algorithms, advanced chips, and data platforms—remain monopolized by the few, while the majority are trapped in a "low-value quagmire," struggling in a race to the bottom.

Against this backdrop, select Chinese intelligent driving enterprises are striving to break out of this Value Trap and explore new paths to disrupt the status quo. Represented by innovative forces like Pony.ai, these companies have achieved a secondary listing on the HKEX within the year through sustained technological breakthroughs and global commercial pilots. This not only demonstrates the growth potential of Chinese enterprises in the autonomous driving sector but also reflects the phased achievements of their upward climb within this "unequal" structure.

Nevertheless, capital markets are fickle, and short-term valuations do not constitute a solid moat. Chinese intelligent driving enterprises must penetrate the fog, lucidly identify their advantages and disconnects within the value chain, and promote the deep integration of technology and commerce to systemically break the fate of being trapped in low-value-added tiers.

Only by forging an autonomous and controllable "value highland" can they define the new rules of future competition and ascend as distinct luminaries on the global intelligent driving map.

On November 6, 2025, Pony.ai successfully completed its dual listing by landing on the Hong Kong Stock Exchange (HKEX) as "The Global First Robotaxi Stock," enjoying a moment of immense prestige.

However, the capital maneuvering of a dual listing failed to assuage the capital market's concerns regarding Pony.ai's profitability prospects. On its first day of trading in Hong Kong, Pony.ai's stock price broke its issue price, falling 12.95% from the offering price of HK$139. The capital market subsequently maintained a tepid response, with the stock price continuing to trend downward throughout the month.

Although the company raised over USD 1 billion through its dual listings in the US and Hong Kong—and explicitly allocated 50% of the net proceeds from the HK listing to advance large-scale commercialization—its model of long-term high investment with low output remains unsustainable. At the current cash burn rate, if commercial deployment falls short of expectations, the company will face renewed pressure for subsequent financing. Meanwhile, industry competition has entered a "white-hot" phase: domestic rivals WeRide and Baidu’s Apollo Go are accelerating their pursuit, international giants Waymo and Cruise are expanding aggressively, and traditional OEMs are entering the fray.

Pony.ai’s predicament profoundly reveals a distinct structural contradiction in the era of intelligent driving:

On one side is the "Consumer Democratization" brought by tech proliferation: Intelligent driving functions are reaching the mass market with unprecedented speed and breadth, bringing universally accessible experiences.

On the other is the brutal reality of "Industrial Value Disparity": Exorbitant R&D costs, prolonged commercialization pathways, and thin short-term profits have trapped the vast majority of enterprises in a value prison, making it difficult to achieve healthy profitability while promoting ubiquity.

Clearly, the industry is collectively experiencing a grueling transition from "cash-burning expansion" to "sustainable organic growth."

In this context, Premier aims to deconstruct this conundrum through a prismatic lens. By taking value as the path, mapping the global industrial landscape, positioning key links in the value chain, and discerning genuine consumer needs, we seek to find a solid anchor point for industry value. Furthermore, through the Intelligent Integrated Product Development (IPD) framework, we aim to achieve a bidirectional coupling of demand matching and value perception, assisting relevant enterprises in navigating the new journey of intelligent driving:

1. Intelligent Driving Carries High Value-Add Expectations:The reality gap highlights the disparity between Chinese and foreign enterprises

2. Decoding "Democratization" vs. "Disparity":Unclear demands and R&D misalignment

3. Essence of Intelligent Integrated Product Development: User-Driven, Value-First

Shanghai

11/F · WSH Building

POLY GREENLAND PLAZA

198 Jingzhou Road

Shanghai PRC · 200082

London

OFFICE SUITE 29A · 3/F

23 Wharf Street

London England · SE8 3GG

Hongkong

9/F · Tower A

NEW MANDARIN PLAZA

14 Science Museum Road

Hongkong SAR · 999077