Resilience in Foundation,

Authentic Value Renewed:

25/26 PRMC Luxe Index

Review & Prospect

Resilience in Foundation,

Authentic Value Renewed:

25/26 PRMC Luxe Index

Review & Prospect

Review the index performance across 2025, help investors understand shifting market trends, navigate short-term volatility with agility, capture key opportunities in 2026, and chart a new path for luxury growth guided by long-term value.

[2025 in a Nutshell]

• Primary Index: The index faced downward pressure on its valuation anchor throughout 2025 due to a repricing of growth expectations. Extended inventory destocking, asynchronous regional recovery, and earnings volatility made it difficult to stabilize the valuation baseline. The index exhibited range-bound fluctuations with limited rebound potential.

[2026 Outlook]

• Primary Index: 2026 is expected to enter a phase of structural recovery, with signals of fundamental bottoming and rebound likely to strengthen. The driving logic will shift from sentiment and valuation recovery to earnings improvement and growth delivery.

Looking back at 2025, the luxury sector’s performance logic shifted from “valuation expansion under a high-growth narrative” to “sentiment repair in search of certainty amid uncertainty” .The pullbacks and volatility in the index were not driven by a single shock, but rather reflected a repricing process shaped jointly by macro interest and exchange rate conditions, the pace of demand and channel inventory clearing, and brands’ pricing and supply discipline.

On the demand side, rising price sensitivity, prolonged channel destocking, and misaligned regional recovery cycles raised the bar for growth visibility and sustainability. At the same time, “wealth stratification and scenario migration” within the sector further widened divergence, prompting capital markets to move from “paying for imagination” to “pricing earnings quality and cash flow resilience.”Rising price sensitivity, extended destocking, and asynchronous regional recovery raised the market's threshold for growth visibility. Capital markets shifted from paying premiums for imagination to pricing earnings quality and cash flow resilience.

Against this backdrop, the re-anchoring of valuation for the primary index, structural divergence across secondary index, and convergence toward quality-based pricing at the stock level together defined the core evolution of the luxury sector in 2025.

More specifically, after the late-2024 correction, the market undertook a more thorough repricing of growth expectations in 2025. Although the primary index still posted full-year gains, the visibility and sustainability of growth were insufficient to support a higher valuation center. Pricing focus shifted forward from long-term narratives to current operating quality and delivery pace.

Meanwhile, the structural performance of secondary index was shaped by “wealth stratification plus scenario preference shifts”. Jewelry and watches, supported by stronger value-preservation narratives and gifting/collectible attributes, served as a stable earnings base for the Core Luxe Index. Demand from ultra-high-net-worth consumers stabilized, and segments such as private yachts and private jets, backed by scarce supply and high average order value, showed stronger momentum, lifting the Ultra Luxe Index.

By contrast, divergence within the Mass Luxe Index was more pronounced. Under shifting preferences and intensifying competition, wines and spirits became a drag, highlighting the vulnerability of discretionary consumption in a soft environment. The Experiential Luxe Index, supported by the recovery of experience-led spending and supply expansion, strengthened steadily, with boutique retail, cruise travel, and hotel services contributing from multiple fronts, underscoring the long-term trend of rising priority for experience spending.

As divergence deepened, capital market pricing became more concentrated. At the stock level, capital preference showed clear quality stratification. Leading Performers, backed by more stable cash flows, stronger pricing power, and tighter channel control, were positioned as core “defensive growth” holdings. Mid-tier Stocks relied more on event-driven catalysts or cyclical operational recovery for upside during rotation windows. Tail-end Stocks, facing weaker demand, deeper discounting, and mounting inventory pressure, fell into a negative feedback loop of “revenue decline–margin compression–investment cuts–brand erosion”.

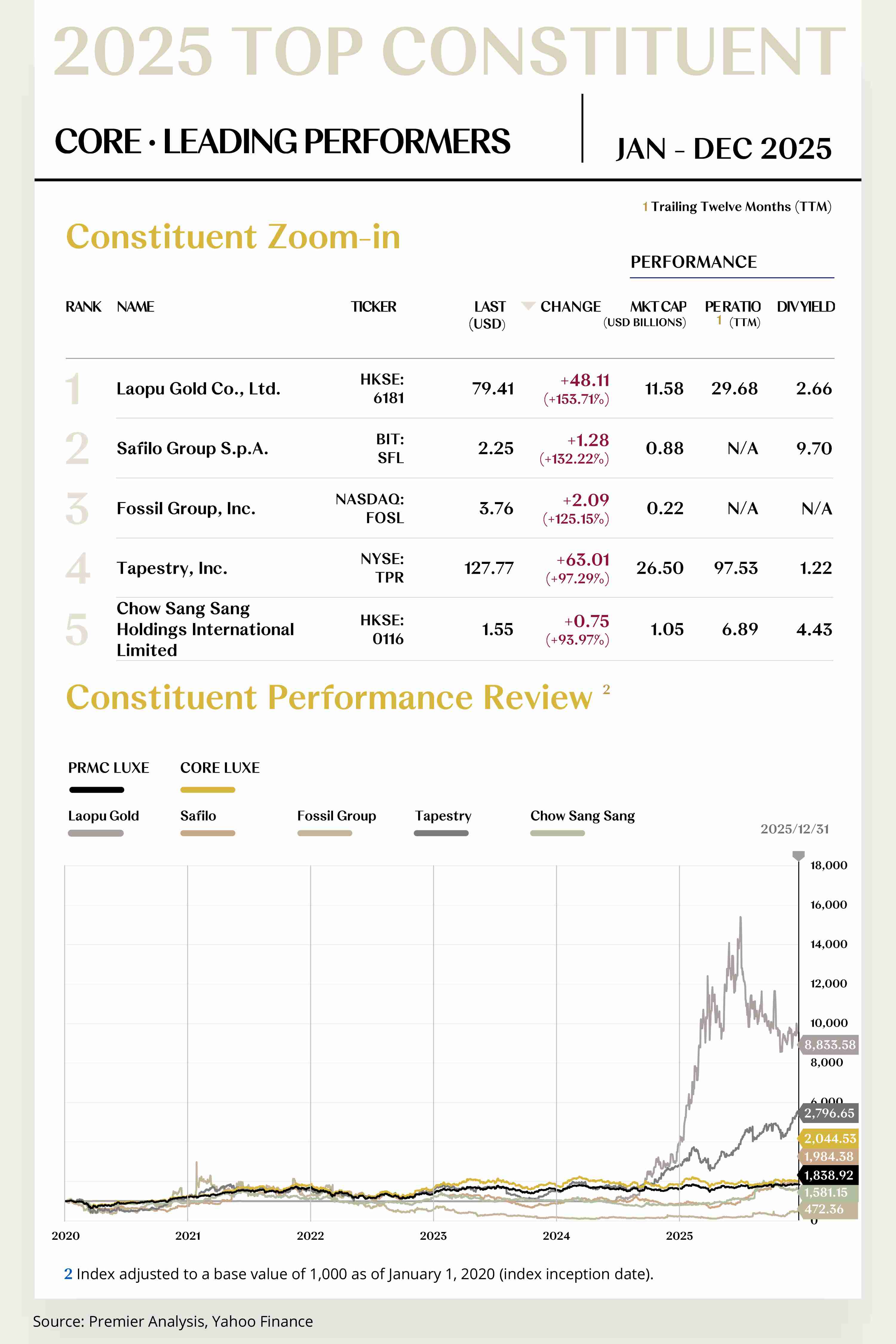

Under this logic, leading names such as Laopu Gold, Bombardier, Safilo, Fossil Group, and Pop Mart stood out and became market favorites.

From a macro perspective, rate cuts in multiple countries and financial market rebounds generated a tangible wealth effect that underpinned high-end consumption, while marginal rate declines offered temporary valuation relief. At the same time, exchange rate volatility, trade frictions, and tariff uncertainty amplified regional sales divergence, making cross-border tourism and duty-free channels more sensitive to external variables.

Overall, the macro environment did not provide a clear one-way driver. Instead, multiple variables jointly reshaped the regional demand gradient, pushing the luxury sector into a regime characterized by “widening divergence and normalized volatility”.

Looking ahead to 2026, the main index narrative is likely to shift from “sentiment repair” to “fundamental repricing”. As policy and liquidity support gradually fade at the margin, external frictions persist, and operational divergence deepens, the market’s tolerance for distant narratives will decline further. Pricing anchors will concentrate more on verifiable earnings quality, cash flow resilience, and delivery pace.

Index upside is expected to come primarily from valuation stability and selective re-rating driven by earnings certainty, rather than broad-based multiple expansion. Companies capable of consistently delivering profits and free cash flow are likely to form the core of index resilience.

Under the constraints of a high base and softer expectations, secondary index will show clearer divergence. For Core Luxe Index, a recovery in ready-to-wear and leather goods, supported by disciplined channel control and product cadence, together with the steady contribution of jewelry and watches, could restore sector leadership. The Ultra Luxe Index may see marginally slower momentum, but its attributes of scarce supply and high certainty should continue to support allocation value.

DOWNLOADS

Lite Report (107 pages)

CORE LUXE CONSTITUENT ZOOM-IN

Immersive Experience Elevating

Brand Premium,

Channel Synergy Accelerating

Market Penetration

The Core Luxe Index comprises 36 stocks, with 28 rising and 8 falling.

Leading Performers

1. Laopu Gold Co., Ltd. (HKSE: 6181)

Laopu Gold is dedicated to inheriting China’s traditional hand-crafted goldsmithing, featuring high-purity pure-gold products and exquisite techniques recognized as intangible cultural heritage. For full year 2025, the company’s share price increased by $48.11 to close at $79.41, up 153.71%.

In 2025, Laopu Gold saw strong momentum right from the beginning of the year and the post-Spring Festival period, repeatedly breaking out across social channels. On February 20, the company issued a positive profit alert for full-year 2024, expecting net profit of approximately RMB 1.4–1.5 billion, a year-over-year increase of 236%–260%, laying a high base for the year’s results.

On June 21, its first overseas store opened at The Shoppes at Marina Bay Sands in Singapore; on June 28, the Shanghai IFC store officially opened, driving high growth across both offline and online channels in the first half, and expanding the nationwide store network to 41 locations across 16 cities as of June 30.

On July 27, the company issued its interim results forecast: first‑half revenue of approximately RMB 12.0–12.5 billion and net profit of approximately RMB 2.23–2.28 billion, maintaining high prosperity. On August 20, the company officially disclosed its interim report: revenue of RMB 12.354 billion and net profit of RMB 2.268 billion, and announced an interim dividend of RMB 9.59 per share, reflecting robust profitability and cash flow.

In 2026, Laopu Gold will continue to deepen its presence in core shopping districts across tier‑one and new tier-one cities and increase penetration in high‑end malls. Against a backdrop of elevated gold prices and recovering wedding and gifting demand, and supported by a rising mix of higher-margin cultural IP/non-standard customization and co-branded series as well as platformized cost reductions in supply chain and craftsmanship, the company is poised to deliver double-digit growth in revenue and profit, maintain healthy operating cash flow, and further optimize gross margin and inventory turnover days.

2. Safilo Group S.p.A. (BIT: SFL)

Safilo Group is a renowned Italian eyewear manufacturer and distributor, specializing in the design, production, and sale of sunglasses, optical frames, and sports eyewear across owned and licensed brands. For full year 2025, the company’s share price increased by $1.28 to close at $2.25, up 132.22%.

On January 14, the company renewed its global eyewear license with Under Armour through 2031, consolidating its position in performance sports. On February 6, it renewed its partnership with Dsquared2 ahead of schedule through 2031, strengthening its high‑end fashion portfolio.

On June 9, it sold its stake in subsidiary Lenti Srl to optimize its asset structure and renewed its global license with Carolina Herrera through 2031.

On June 24, the company formally launched a share repurchase program. On June 30, Safilo signed a 10‑year global license agreement with Victoria Beckham, extending the term to December 2035.

Looking ahead to 2026, Safilo is expected to achieve low-to mid-single-digit revenue growth at constant currency and a modest improvement in profitability under the combination of “license stability + new product ramp‑up + operational efficiency.”

The full‑line Victoria Beckham collection launched in January will contribute its first year of scaling, while the renewals with Under Armour, Dsquared2, and Carolina Herrera will provide clear revenue visibility.

[For more insights, please download the full report]

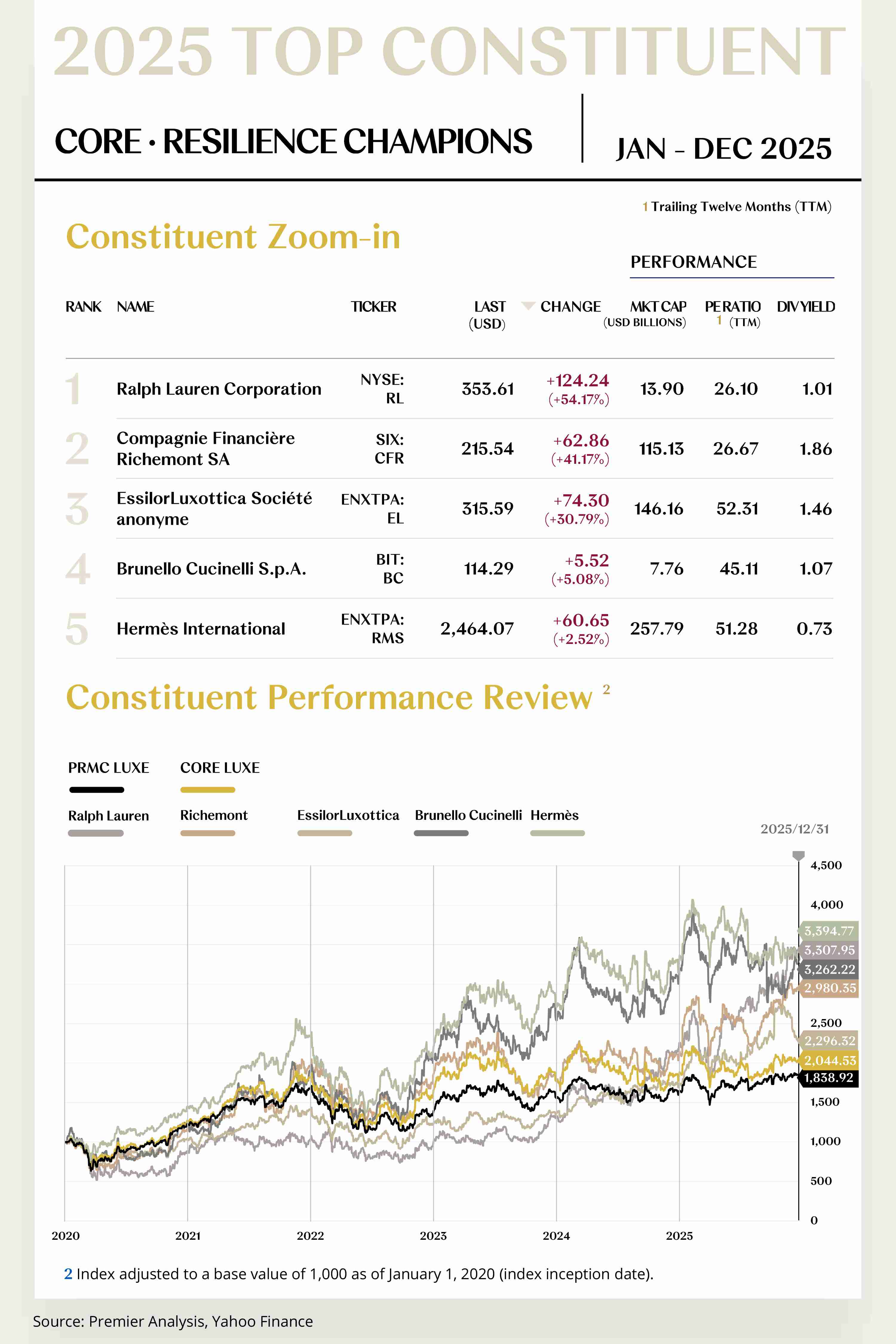

Resilience Champions

1. Ralph Lauren Corporation (NYSE: RL)

Founded in 1967, Ralph Lauren is a global luxury lifestyle group spanning apparel, accessories, home, and fragrances. For full year 2025, the company’s share price increased by $124.24 to close at $353.61, up 54.17%.

On January 4, founder Ralph Lauren received the Presidential Medal of Freedom, significantly amplifying the brand’s cultural resonance. On January 16 during Milan Men’s Fashion Week, the brand staged a presentation at Palazzo Ralph Lauren, with Purple Label and Polo shown together to strengthen cross-generational connection and immersive in-person show experiences.

On February 6, the company reported a fiscal third-quarter beat and raised full-year guidance; global DTC revenue grew 12% year over year, adding 1.9 million new direct-to-consumer customers.

On April 18, Ralph Lauren purchased the flagship freehold at 109 Prince Street in New York’s SoHo for US$132 million, securing long-term traffic and a theatrical brand showcase via owned landmark retail—and prevailed over LVMH in the process.

On December 4, the company unveiled Team USA’s opening and closing ceremony looks for the 2026 Milano-Cortina Winter Olympics; the partnership extending through 2028 continues to bring “national moments” onto the global stage.

Looking ahead to 2026, under the “Next Great Chapter: Drive” framework, Ralph Lauren is expected to continue key-city and DTC-led growth, delivering low single-digit revenue growth and a slight expansion in operating margin per prior company framing.

2. Compagnie Financière Richemont SA (SIX: CFR)

Richemont is a leading global luxury group focused on jewelry and high watchmaking, with renowned Maisons including Cartier, Van Cleef & Arpels, Panerai, and Jaeger-LeCoultre. For full year 2025, the company’s share price increased by $62.86 to close at $215.54, up 41.17%.

On January 16, the Group issued a Q3 FY2025 trading update: quarterly sales of €6.15 billion, up 10% year over year at constant exchange rates, with double-digit growth across the Americas, Europe, the Middle East & Africa, and Japan.

On April 14, EU regulators approved the sale of YOOX NET-A-PORTER (YNAP) by the Group to Mytheresa. Upon completion, the Group received a 33% stake in the renamed LuxExperience B.V. and €550 million in net cash.

On November 14, the Group reported H1 FY2026 interim results: sales of around €10 billion, up approximately 10% at constant exchange rates; operating profit of €2.36 billion, up 7% year over year, with operating margin at 22.2%, up 3 percentage points.

Looking ahead to 2026, Richemont’s base case calls for low- to mid-single-digit sales growth and a moderate recovery in operating margin, with core drivers from the continued strength of the jewelry division and channel-mix optimization.

[For more insights, please download the full report]

Experience-refined Value Picks

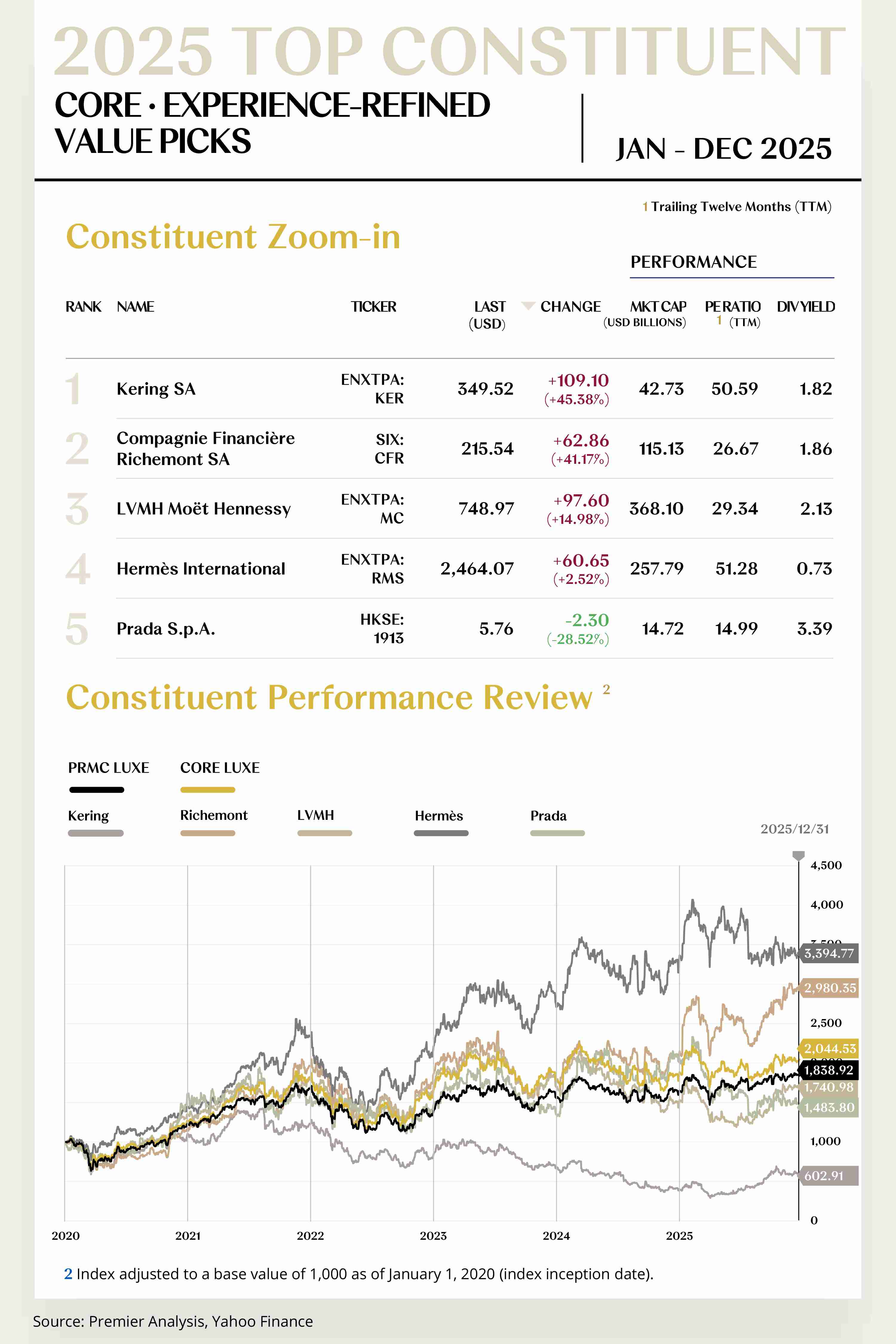

1. Kering SA (ENXTPA: KER)

Kering is a global leading luxury group whose houses include Gucci, Saint Laurent, and Bottega Veneta, spanning fashion, leather goods, jewelry, and watches. For full year 2025, the company’s share price rose by $109.10 to close at $349.52, up 45.38%.

In 2025, Kering continued its “experiential excellence” agenda through both subtraction and addition. In January, it formed a joint venture with Ardian covering three core properties at Place Vendôme and Avenue Montaigne in Paris, netting approximately €837 million in cash. At the end of the month, it sold The Mall Luxury Outlets in Italy to Simon, sharpening focus on high-end boutiques and selected outlet channels and netting about €350 million.

In February, the Group announced its separation from Sabato De Sarno; in March, it appointed Demna as Gucci’s Artistic Director effective July, injecting a highly distinctive aesthetic and strong cultural buzz into the brand relaunch.

In May, the Group reached an Android XR smart-glasses cooperation with Google to extend immersive, wearable luxury scenarios, and acquired Italian lens and component partners Visard and Mistral to reinforce supply-chain autonomy and control.

In December, the Group hosted the inaugural “Night at the Museum” biodiversity evening, deepening emotional ties through cultural settings. In the same month, it announced a phased acquisition of Italian high-end jewelry manufacturer Raselli Franco Group, further vertically integrating high jewelry and fine jewelry capacity to support the long-term value elevation of experiential maisons such as Boucheron, Pomellato, and Qeelin.

Looking to 2026, Kering is expected to return to moderate growth under the “experiential excellence” strategy: at Gucci, a full product cycle under Demna drives full-price sell-through, higher ticket sizes, and better store productivity; owned retail comps are expected to turn from negative to positive and accelerate to low- to mid-single digits in the second half.

For the full year, operating margin may expand by 0.5–1.5 percentage points; free cash flow should be significantly stronger than in 2025; asset and inventory turns improve, and financial flexibility supports continued dividends and buybacks.

2. Compagnie Financière Richemont SA (SIX: CFR)

Richemont is a global leading luxury group engaged in high-end jewelry and fine watchmaking, with maisons including Cartier, Van Cleef & Arpels, IWC, and Jaeger-LeCoultre. For full year 2025, the company’s share price rose by $62.86 to close at $215.54, up 41.17%.

The Group ran 2025 through the lens of “immersive experiences + brand power deepening + portfolio optimization.”

In early April, its 12 watch maisons appeared collectively at Watches & Wonders Geneva 2025, using in-person showcases and new-product storytelling to expand “tangible luxury experiences.”

On the 24th of the same month, the Group completed the sale of YNAP to Mytheresa, receiving a 33% stake in the renamed LuxExperience B.V., marking its exit from e-commerce operations and a refocus on high-margin “fine luxury” core businesses.

In December, the Group intensified its “travel + destination experience” footprint: A. Lange & Söhne opened flagships in London and Singapore, Piaget unveiled its Singapore flagship, Chloé entered Australia with its first store, and Van Cleef & Arpels’ L’ÉCOLE School of Jewelry Arts brought a new exhibition, “Stones and Reveries,” building on its Paris/Hong Kong/Shanghai presence to extend client journeys and emotional stickiness through cultural curation and craftsmanship education.

Looking ahead to 2026, Richemont’s base case is low- to mid-single-digit sales growth and a moderate recovery in operating margin, driven primarily by sustained strength in jewelry and optimization of channel mix.

[For more insights, please download the full report]

ULTRA LUXE CONSTITUENT ZOOM-IN

Order Backlogs Securing Earnings Visibility,

Positive Cash Flow Supporting Strategic Investment

The Ultra Luxe Index comprises 20 stocks, with 14 rising and 6 falling.

Leading Performers

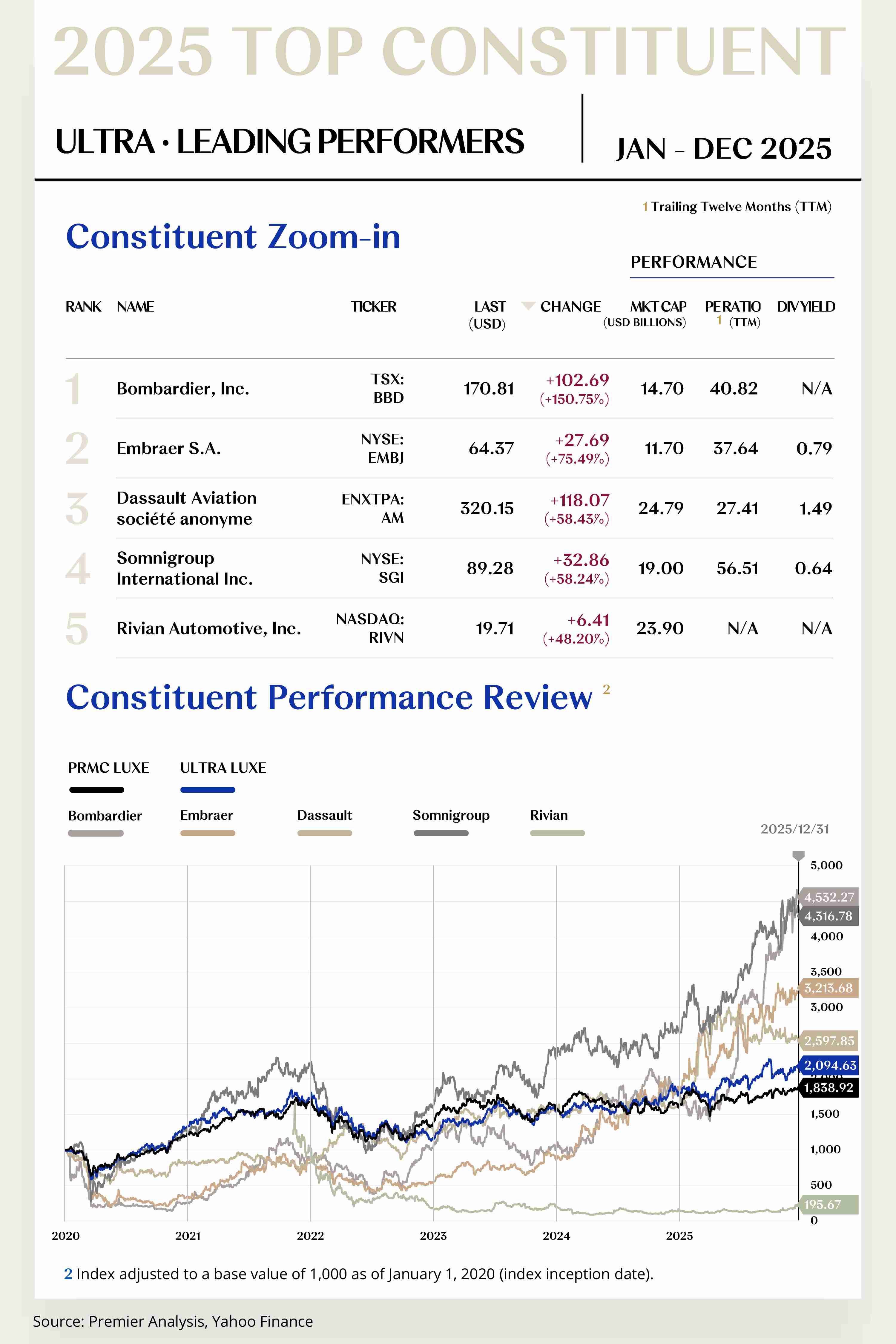

1. Bombardier, Inc. (TSX: BBD)

Bombardier is a global leader in business aviation, focused on the design, manufacture, and after-sales services of high-performance jets, with product lines including the Global and Challenger families. For full year 2025, the company’s share price rose by $102.69 to close at $170.81, up 150.75%.

On June 16, at the Paris Air Show, the company signed a defense technology innovation MoU with Safran to strengthen platform conversion and mission-system capabilities. In the same month, it announced a milestone order for 50 aircraft (plus 70 options) with a “first-of-its-kind” full lifecycle services agreement.

On the experience side, in December the company introduced an onboard smart-router upgrade to enhance connectivity, accelerated construction of the Abu Dhabi service center, and advanced defense programs in Germany and elsewhere.

Throughout the year, Bombardier continued publishing updates to its 2025 Environmental Product Declarations and advocated/tested SAF in multiple settings, enhancing perceived client value across the journey through the consistency of “sustainability × high-end services.”

Looking to 2026, deliveries and revenue are expected to grow steadily, with the services business lifting margins and cash flow on network expansion and a maturing in-service fleet.

2. Embraer S.A. (NYSE: ERJ)

Embraer’s core businesses encompass the design and manufacture of commercial, executive, and defense aircraft, as well as aviation services. For full year 2025, the company’s share price rose by $27.69 to close at $64.37, up 75.49%.

On May 6, the company posted first-quarter results: revenue of US$1.103 billion, up 23% year over year; 30 new aircraft delivered; and maintained a high full-year revenue outlook—providing a financial backbone for “steady, sustainable experience investments.”

During the Paris Air Show in June, subsidiary Eve Air Mobility announced multiple ecosystem collaborations, funding, and order arrangements—including a FINEP grant and agreements with Revo/FFG—building immersive “urban air mobility” scenarios for eVTOL entry into service in 2027.

Looking to 2026, backed by a record order backlog, the company expects steady gains in revenue and free cash flow under a dual engine of smoother production and high-margin services, consolidating margins and investor interest.

[For more insights, please download the full report]

Resilience Champions

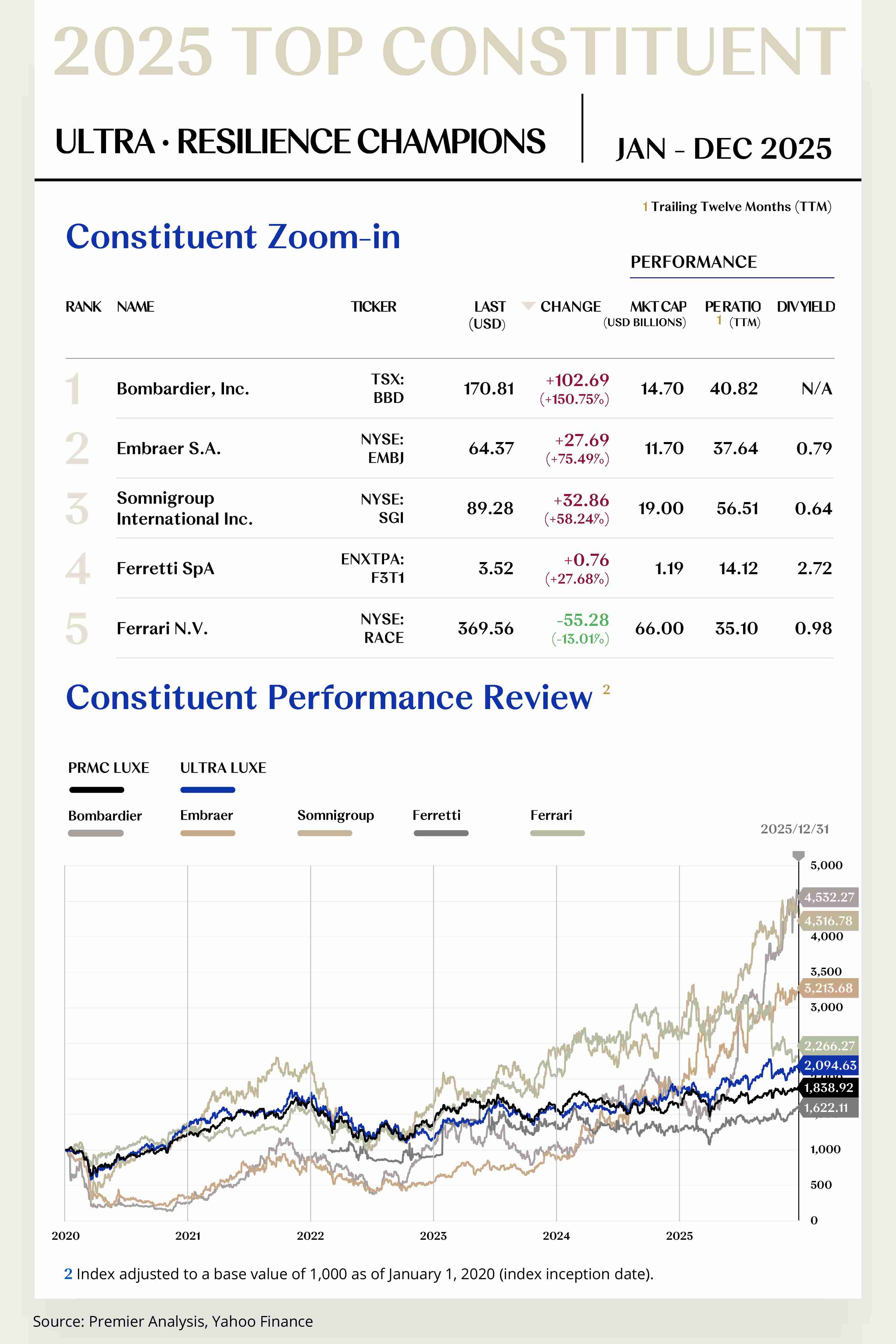

1. Bombardier, Inc. (TSX: BBD)

Bombardier is a global leader in business aviation, focused on the design, manufacture, and after-sales services of high-performance jets, with product lines including the Global and Challenger families. For full year 2025, the company’s share price rose by $102.69 to close at $170.81, up 150.75%.

On May 1, the company reported first-quarter results: revenue of US$1.5 billion, up 19% year over year; adjusted EBITDA of US$248 million; backlog of US$14.2 billion; and raised its full-year targets, emphasizing faster deliveries and improved free cash flow.

On July 11, the company announced the Global 7500 had achieved its 135th speed record, connecting multiple city pairs at an average ground speed exceeding 1,000 km/h, reinforcing its “speed + smoothness” experience credentials.

On December 8, the Global 8000 completed its first delivery in Mississauga and entered service, setting an experience benchmark for ultra-long-range business jets with “faster + farther + healthier.”

Looking to 2026, deliveries and revenue are expected to grow steadily, with services lifting margins and cash flow as the network expands and the fleet matures.

2. Embraer S.A. (NYSE: ERJ)

Embraer’s core businesses encompass the design and manufacture of commercial, executive, and defense aircraft, as well as aviation services. For full year 2025, the company’s share price rose by $27.69 to close at $64.37, up 75.49%.

The year’s theme was “product-experience upgrades + cross-cycle resilience in deliveries and orders.”

On February 25, ANA Holdings confirmed an order for 15 E190-E2s with 5 options, refreshing Japanese regional routes with a quieter, no-middle-seat cabin experience. On the 27th, the company raised full-year delivery and revenue guidance, stressing steady production increases despite supply-chain constraints.

At the Paris Air Show in June, the company announced up to 110 E175s from SkyWest, a leasing order for 10 E195-E2s for Airlink, and launched the E-Freighter. Dual-aircraft flight displays on site embodied the “low noise, low fuel burn” passenger experience.

Looking to 2026, backed by a record order backlog, Embraer expects steady gains in revenue and free cash flow under a dual engine of smoother production and high-margin services, consolidating margins and capital appeal.

[For more insights, please download the full report]

Experience-refined Value Picks

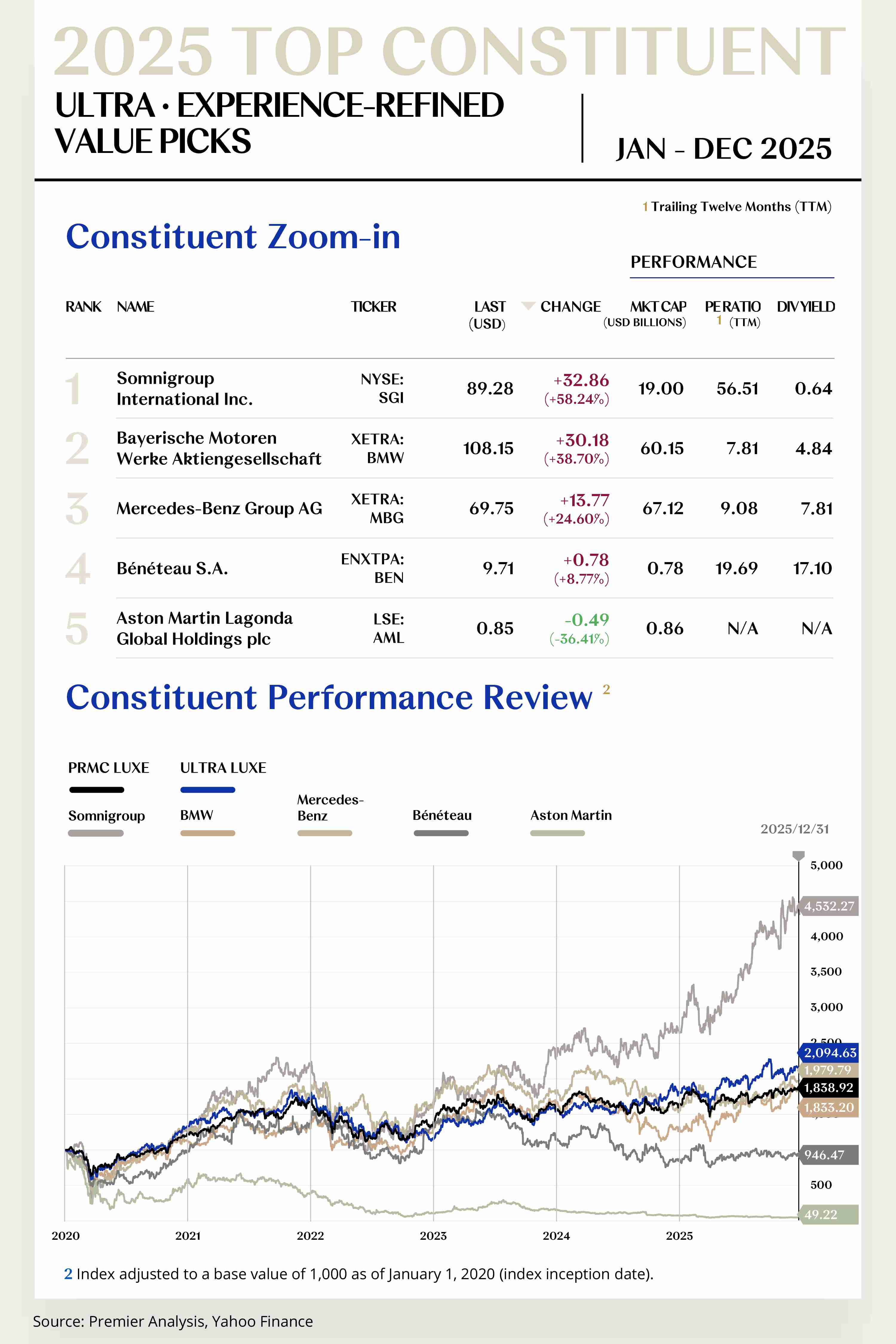

1. Somnigroup International Inc. (NYSE: SGI)

Somnigroup is a global leader in bedding with brands including Tempur-Pedic, Sealy, and Stearns & Foster, offering premium mattresses, pillows, and sleep accessories. For full year 2025, the company’s share price rose by $32.86 to close at $89.28, up 58.24%.

In 2025, the company operated through “M&A integration + omnichannel experiences + brand content + travel-industry touchpoints.”

On January 27, it announced the Tempur-Pedic × Calm collaboration, adding meditation and sleep content to the TEMPUR-Ergo smart base, and launched a new Sealy Posturepedic line.

On May 8, it released the first consolidated quarter and updated full-year guidance, emphasizing “M&A + store refresh” and deleveraging. On August 7, it reported second-quarter net sales up 52.5% year over year to about US$1.881 billion on consolidation, with D2C mix up to 66%; GAAP EPS was under short-term pressure due to merger-related costs and higher interest expense, but management reaffirmed synergy and cash-flow deleveraging cadence.

On the same day, the company raised its full-year EPS guidance and announced a 10-year global license plus a US$25 million strategic investment with Fullpower-AI to bolster the Sleeptracker-AI smart-sleep ecosystem; meanwhile, the North American Sealy new lines launched and integration synergies exceeded expectations, validating its dual engine of product and channel.

Reviewing 2025, through executed M&A, network refreshes, smart-hardware experience upgrades, and scenario penetration, Tempur Sealy completed the transmission chain of “brand experience—emotional connection—long-term value refinement—valuation uplift.” In 2026, “channels + product + experience” is expected to continue driving revenue and gross-margin expansion.

2. BMW AG (XETRA: BMW)

BMW is a Munich-headquartered automotive group with three car brands—BMW, MINI, and Rolls-Royce—and the BMW Motorrad motorcycle brand. For full year 2025, the company’s share price rose by $30.18 to close at $108.15, up 38.70%.

In 2025, the Group’s year was anchored by “Neue Klasse production kickoff + full-stack software and charging ecosystems + multi-brand immersive events.”

From June 13–15, at MY BMW World 2025 in Malaysia, “Heritage in Motion” presented multi-propulsion showcases for BMW/MINI/BMW Motorrad, with immersive displays, local test drives, coffee culture, and merchandise—closing the loop from “show—play—purchase.”

On June 3, the Group disclosed scenario partnerships with a well-known hotel chain to unify “long-haul—urban ring roads—hotel stays” into a perceivable travel-experience flow. In the U.S./Europe/China, it expanded networks via joint ventures IONNA/IONITY/IONCHI to enable cross-border “plug-and-charge” with multi-contract access through a single ID.

On November 1, Chengdu’s “BMW M Heat Carnival” blended track days, cultural performances, and new-model debuts to cultivate an immersive “festivalized” owner community, continuously converting “driving joy—community—content” into reputation and premium.

Looking to 2026, BMW will roll out 600 kW ultra-fast charging and Spark Alliance cross-network interconnection, with IONNA in North America and IONCHI in China expanding; faster and simpler cross-border and urban charging will feed BEV adoption and strengthen word-of-mouth in travel scenarios among high-value users.

[For more insights, please download the full report]

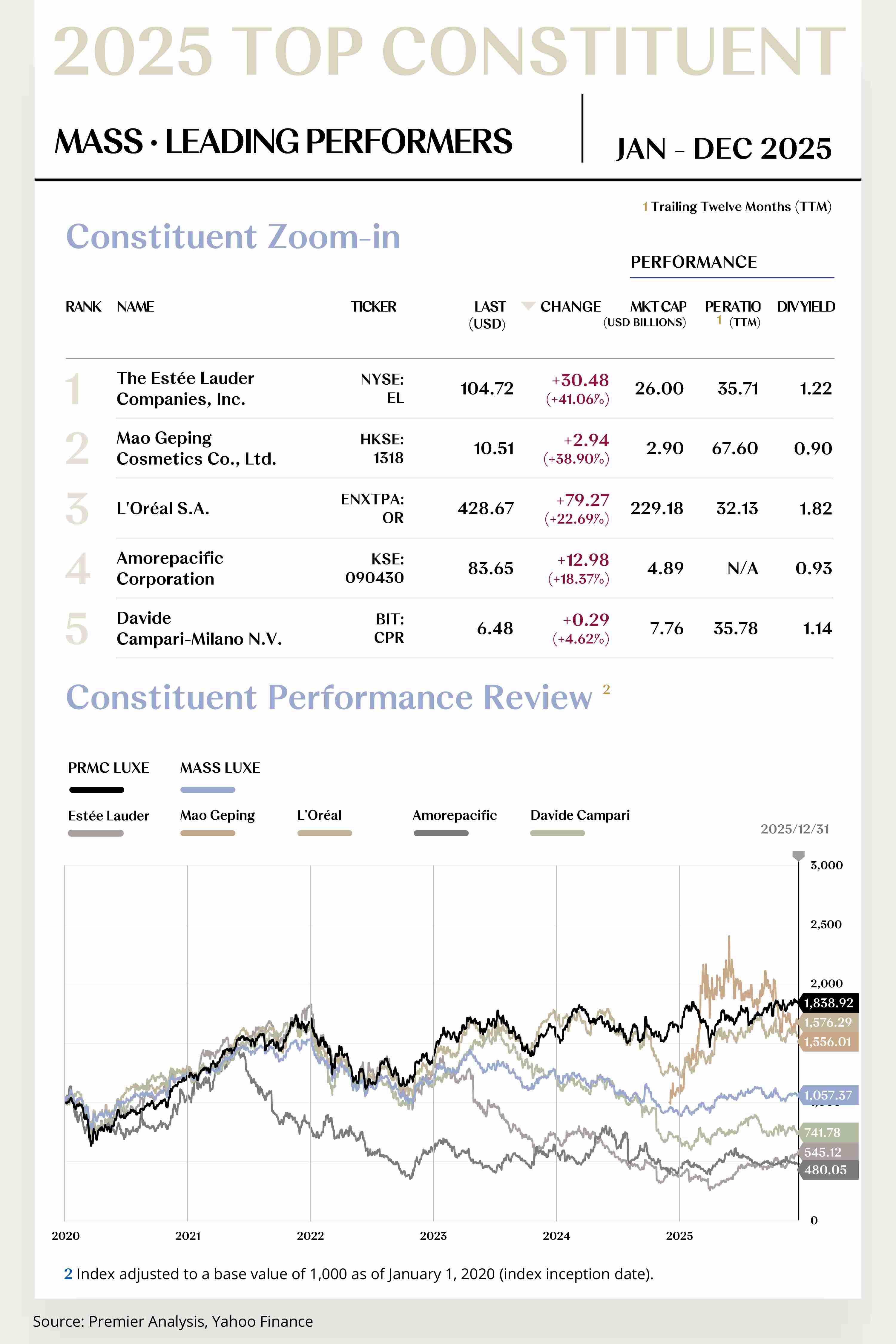

MASS LUXE CONSTITUENT ZOOM-IN

Global Footprint Expanding Market Reach,

Localized Operations Aligning with Authentic Demand

The Mass Luxe Index comprises 19 stocks, with 5 rising and 14 falling.

Leading Performers

1.The Estée Lauder Companies Inc. (NYSE: EL)

The Estée Lauder Companies is a world-renowned beauty company with a portfolio that includes Estée Lauder, La Mer, Clinique, and many other leading brands. For full year 2025, the company’s share price rose by $30.48 to close at $104.72, up 41.06%.

On February 4, the company officially launched its “Beauty Reimagined” strategy and expanded its “profit recovery and growth plan,” freeing up resources for consumer-facing investment and innovation through channel restructuring, outsourcing, and supply-chain efficiency gains.

In April, the company reported Q3 results and noted progress in the “travel-retail reset.” At that time, pressured traffic and conversion in Hainan weighed on the sector; industry and channel data also showed weakening duty-free spending, underscoring the necessity of destocking and structural adjustments.

In December, the Jo Malone London AI Fragrance Advisor co-built with Google Cloud went live, enabling “olfactory try-on” online. Bobbi Brown launched on Amazon Premium Beauty in the United States to open a new customer-acquisition entry point.

Looking ahead to 2026, under the “Beauty Reimagined” strategy, Estée Lauder is expected to regain organic growth momentum and repair margins. The company will also expand its profit recovery and growth plan, creating expense headroom via supply-chain and outsourcing optimization.

2. Mao Geping Cosmetics Co., Ltd. (HKSE: 1318)

Mao Geping is a leading Chinese premium color-cosmetics company, whose brands include “Mao Geping” and “Zaishang Chuangmei,” with products spanning base, eye, and lip categories. For full year 2025, the company’s share price rose by $2.94 to close at $10.51, up 38.90%.

The company delivered a clear growth cadence during the year. On January 12, it issued a positive interim outlook: for the six months ended June 30, revenue was expected at RMB 2.57–2.60 billion, up 30.4%–31.9% year over year, with net profit of RMB 665–675 million, up 35%–37% year over year.

In December, its equity- and long-term-incentive plan was implemented, granting restricted stock units to 133 key employees at HK$45.12 per share to bind core talent and reinforce organizational capability.

Looking ahead to 2026, Mao Geping is poised for steady growth on a high profitability base. Synergy between offline high-end department-store counters and online live-commerce/content e-commerce will remain the growth core, with a high member repurchase rate supporting stable release of volume and profit.

[For more insights, please download the full report]

Resilience Champions

1. Mao Geping Cosmetics Co., Ltd. (HKSE: 1318)

Mao Geping is a leading Chinese premium color-cosmetics company, whose brands include “Mao Geping” and “Zaishang Chuangmei,” with products spanning base, eye, and lip categories. For full year 2025, the company’s share price rose by $2.94 to close at $10.51, up 38.90%.

On March 27, the company released audited 2024 annual results, disclosing full-year revenue of RMB 3.885 billion and net profit of RMB 881 million among other key indicators.

On product and brand, in March the company launched the “Jingcan Xingqiong” eye-shadow and, in the first half, introduced the “Gu Yun Ning Xiang” and “Wen Dao Dong Fang” fragrance series, further enriching the color-cosmetics and fragrance matrices and the narrative of Eastern aesthetics.

Looking ahead to 2026, Mao Geping is poised for steady growth on a high profitability base. Synergy between offline high-end department-store counters and online live-commerce/content e-commerce will remain the growth core, with a high member repurchase rate supporting stable release of volume and profit.

2. Puig Brands, S.A. (BME: PUIG)

Puig is a Barcelona-headquartered global beauty and fashion group that spans prestige fragrances, makeup, skincare, and fashion. For full year 2025, the company’s share price fell by $0.84 to close at $17.39, down 4.62%.

On April 28, the company reported Q1 performance: net revenue of approximately €1.206 billion, up 7.5% year over year, and disclosed that forward stocking in the U.S. helped buffer tariff impacts; full-year guidance remained unchanged, demonstrating operating resilience and execution.

On October 30, the company reported Q3 results: quarterly net revenue of about €1.30 billion, 6.1% organic growth. Heading into holiday season, management again confirmed full-year growth would be mid-range of the 6%–8% corridor, underscoring “quality-led stability” in growth visibility.

This top-down cadence management, proactive external hedging, and internal organizational upgrades together underpinned the company’s “high-resilience” chassis in 2025, maintaining relative outperformance versus premium beauty and a stable margin-improvement path from Q1 through year-end.

Building on 2025’s “steady growth + efficiency,” the company is expected to sustain mid- to high-single-digit organic growth and margin improvement, continuing multi-business and multi-region synergies and laying the operating baseline for 2026 margin flexibility.

[For more insights, please download the full report]

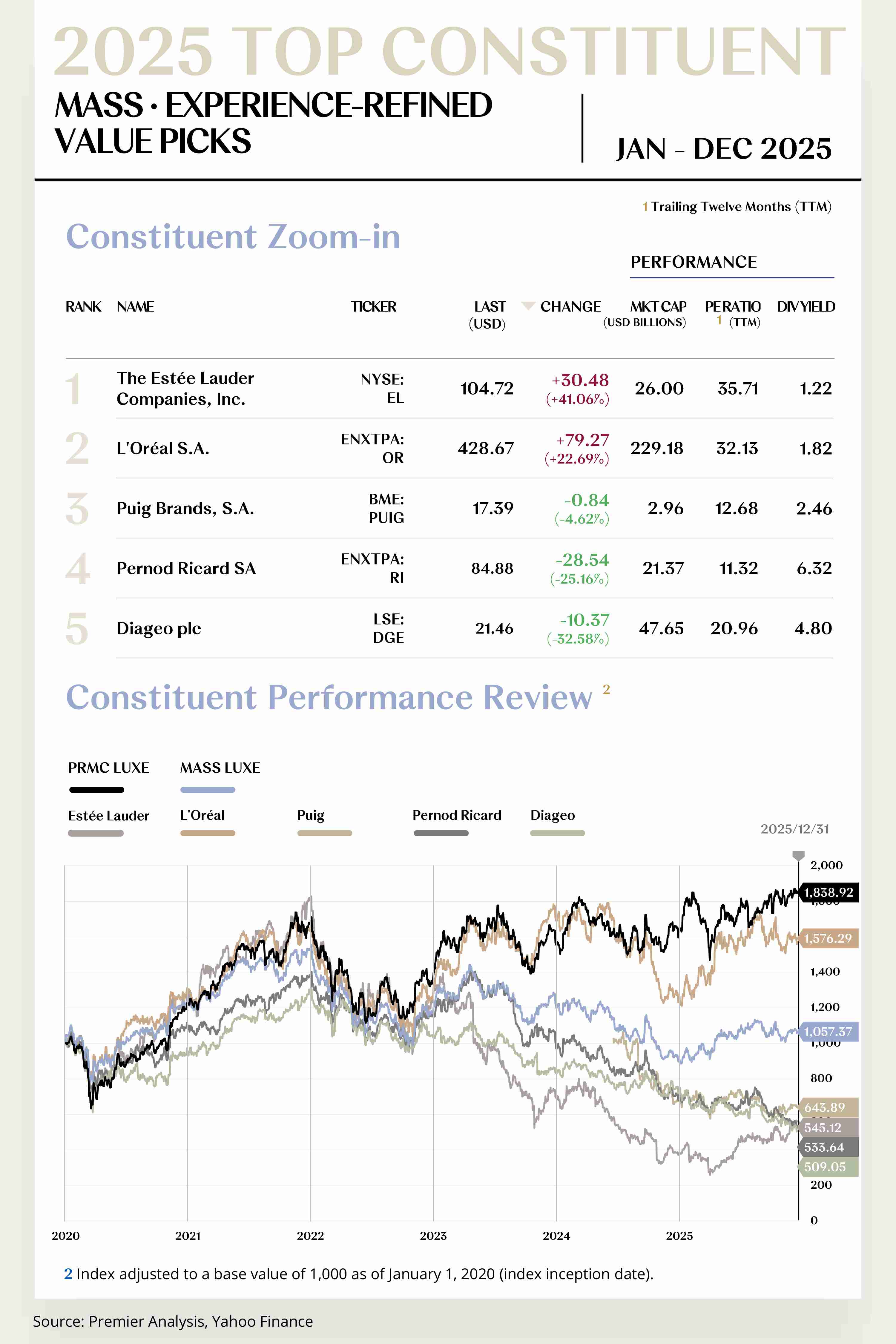

Experience-refined Value Picks

1. The Estée Lauder Companies Inc. (NYSE: EL)

The Estée Lauder Companies is a world-renowned beauty company with a portfolio that includes Estée Lauder, La Mer, Clinique, and many other leading brands. For full year 2025, the company’s share price rose by $30.48 to close at $104.72, up 41.06%.

In 2025, Estée Lauder connected the year with the “Beauty Reimagined” reset. In January, M·A·C preheated with the “I Only Wear M·A·C” star-studded campaign and its annual philanthropy report, and announced immersive flagship experiences and artistic collaborations in China to reinforce word-of-mouth around “participatory artistry.”

In March, TOM FORD BEAUTY held the SOLEIL summer collection launch in Tokyo with Asia-Pacific celebrities, followed by a cross-category POP-UP at Hankyu Umeda with TOM FORD Eyewear, unifying fragrance, makeup, and accessories into a “complete look” experience.

From April to May, M·A·C launched the new Studio Fix powder foundation, and TOM FORD’s “Luminous Summer” national debut opened in Dongguan; concurrently, the company reported Q3 and noted progress in the “travel-retail reset.” At that time, pressured traffic and conversion in Hainan and broader industry data showing weaker duty-free consumption confirmed the need for destocking and structural adjustments.

In July, M·A·C opened an immersive “piano × beauty” flagship in Nanjing to heighten playability for younger consumers across online and offline. In the same month, the company reported FY2025: revenue declined 8% year over year, but gross margin improved. Management reiterated targets for growth resumption and margin repair in FY2026.

Looking ahead to 2026, under the “Beauty Reimagined” strategy, Estée Lauder is expected to regain organic growth momentum and repair margins. The company will also expand its profit recovery and growth plan, creating expense headroom via supply-chain and outsourcing optimization.

2. L’Oréal S.A. (ENXTPA: OR)

L’Oréal is the global leader in beauty, spanning luxury beauty, mass cosmetics, professional haircare, and dermatological beauty. For full year 2025, the company’s share price rose by $79.27 to close at $428.67, up 22.69%.

In 2025, the Group ran the year under “Beauty Tech × premium experience × portfolio upgrade × sustainability.”

In January at CES 2025, it unveiled Cell BioPrint personalized skin diagnostics and the accessibility-focused L’Oréal SYNC system, signaling a forward-looking experience roadmap powered by “longevity science + AI.” It also kicked off the Hainan offshore duty-free annual campaign, bringing an immersive sensorial space to the Sanya CDF travel-retail flagship centered on “algal light-and-shadow” materials and tea-ceremony hospitality.

In February, it announced a minority investment in Jacquemus together with a long-term exclusive beauty license, strengthening Luxe’s Gen-Z social-media narrative and “couture fragrance & beauty” matrix.

In May at VivaTech, the Group presented “Longevity Integrative Science™,” YSL Hyper Look Studio, and AirLight Pro experience technologies.

From June onward, brand-experience highlights included the Armani Mare summer pop-up at Milan Malpensa, a “five-senses retail” scene at the Hainan Consumer Expo, and the SXSW Sydney “Innovation Station” immersive installation—deepening “airport—exhibition—city festival” travel-style touchpoints.

Looking ahead to 2026, L’Oréal is expected to maintain an “outgrow the market + margin improvement” rhythm, riding the wave of travel retail and experiential consumption to deliver full-year performance and balance-sheet repair.

[For more insights, please download the full report]

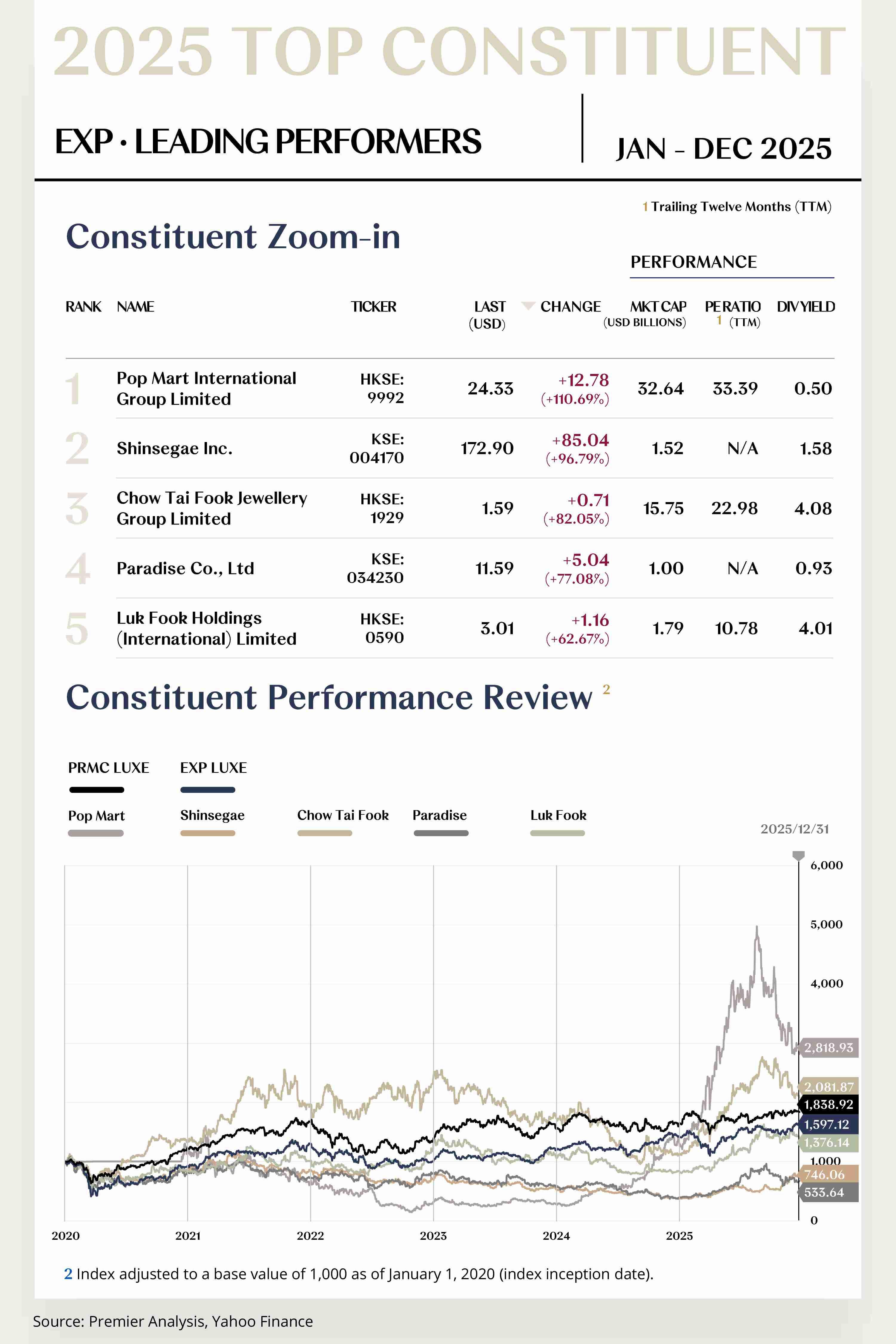

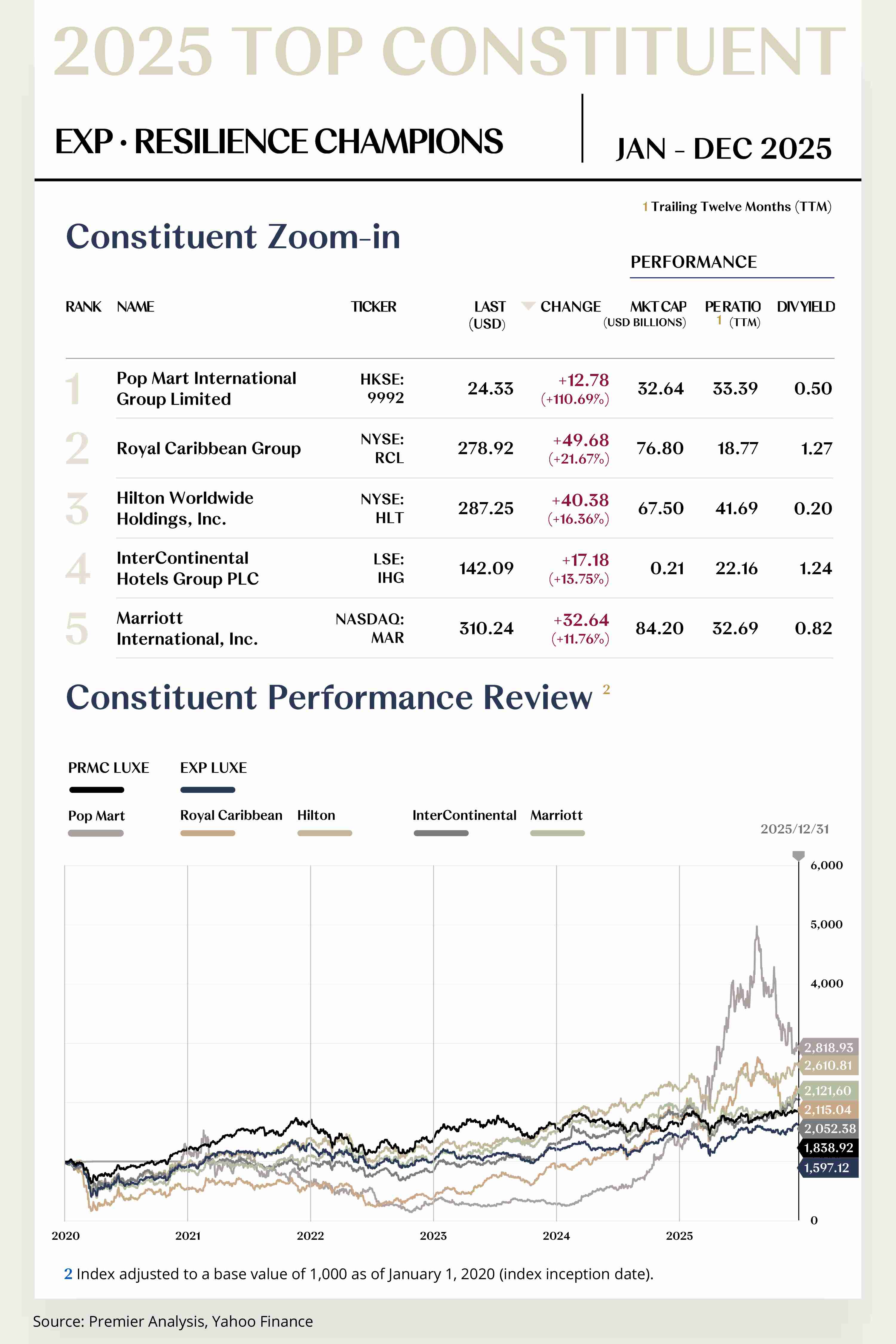

EXP LUXE CONSTITUENT ZOOM-IN

Digital Ecosystems Enhancing Customer Stickiness,

Omnichannel Coordination Increasing Purchase Frequency

The Experiential Luxe Index comprises 51 stocks, with 31 rising and 20 falling.

Leading Performers

1. Pop Mart International Group Limited (HKSE: 9992)

POP MART is a designer toy and character entertainment company centered on IP, owning and operating proprietary/exclusive IPs such as MOLLY, SKULLPANDA, DIMOO, and THE MONSTERS. For full-year 2025, the company’s share price rose by $12.78 to close at $24.33, an increase of 110.69%.

On February 23, the leadership told CNA in an interview that the proportion of overseas business would exceed 50%, and that the company would leverage collaboration with Ne Zha 2 along with pop-ups and co-branding to accelerate global breakout. On March 26, the company released its 2024 annual results, reporting revenue of RMB 13.038 billion and net profit of RMB 3.308 billion.

On December 10, the company announced changes to the Board and the Nomination Committee: Wu Yue was appointed as a Non-Executive Director and the committee composition was updated to bring in luxury and consumer insights.

Overall, in 2025 the company executed a cadence of “blockbuster single products + multi-IP portfolio + rapid overseas channel expansion + organizational governance upgrades,” achieving simultaneous volume and profit growth that also spilled over into capital operations and governance, cementing its sector-leading position.

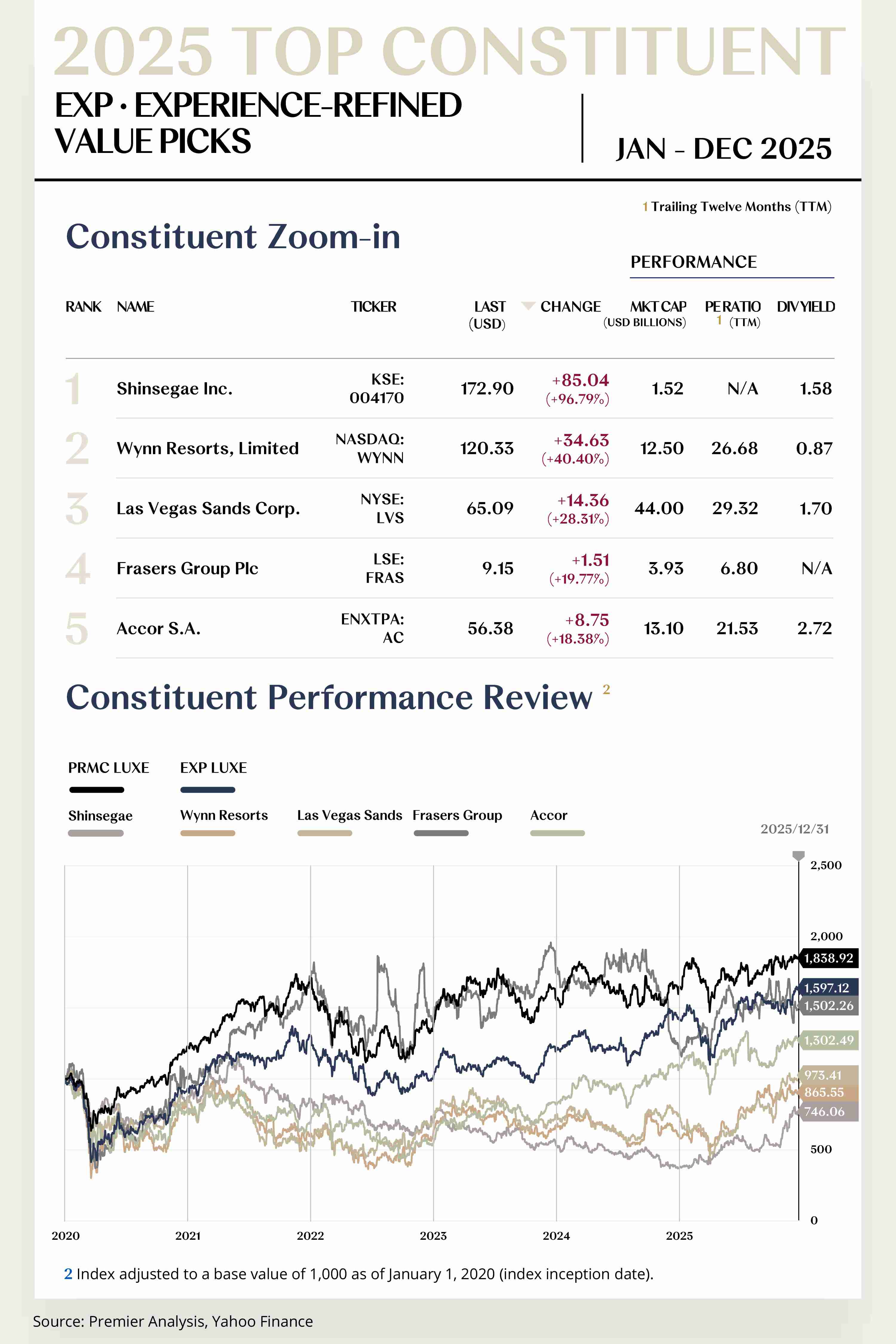

2. Shinsegae Inc. (KSE: 004170)

Shinsegae is a Seoul-based integrated retail group with department stores as its core business and, through subsidiaries, operates high-end outlets and duty-free formats. It is one of the “big three” department store groups in Korea. For full-year 2025, the company’s share price rose by $85.04 to close at $172.90, an increase of 96.79%.

On February 5, the company released a summary of Q4 and full-year 2024 results, setting the tone for the operating and capital game plan at the start of the year. On March 20, the company held its 68th AGM and approved a cash dividend of KRW 4,500 per share, thereby strengthening market confidence through tangible shareholder returns.

On July 8, together with Shinsegae Property, Hana Financial, and Bain Capital, the company reached a ~KRW 600 billion financing and investment agreement for the Starfield Cheongna complex, advancing a “retail × culture & performance” integrated destination.

Looking at 2026, the core will be driven by department store premiumization and scenario-based upgrades. Full-year operation of the The Heritage cultural landmark and the expansion of contemporary halls at Gangnam/Main Store, along with brand introductions, are expected to continue lifting basket size and sales per square meter.

[For more insights, please download the full report]

Resilience Champions

1. Pop Mart International Group Limited (HKSE: 9992)

POP MART is a designer toy and character entertainment company centered on IP, owning and operating proprietary/exclusive IPs such as MOLLY, SKULLPANDA, DIMOO, and THE MONSTERS. For full-year 2025, the company’s share price rose by $12.78 to close at $24.33, an increase of 110.69%.

On February 21, the artist brand HIRONO opened its first flagship store in Shanghai, further expanding the offline ecosystem.

On June 18, the operating scenes at the POP LAND city park set up in Beijing’s Chaoyang Park received concentrated coverage from multiple media outlets; the surge in buzz drove growth in offline footfall.

On June 27, the company was included for the first time in TIME’s 2025 “TIME100 Most Influential Companies,” marking authoritative recognition of its global brand influence.

Looking at 2026, growth is expected to be driven by accelerated overseas expansion and channel optimization, coupled with continuous launches of top proprietary IPs and tiered pricing. Refined member and private-domain operations are set to lift ARPU and repeat purchases, with revenue and profit likely to sustain double-digit growth.

2. Royal Caribbean Group (NYSE: RCL)

Royal Caribbean is one of the world’s leading cruise vacation companies, operating brands including Royal Caribbean International, Celebrity Cruises, and Silversea. For full-year 2025, the company’s share price rose by $49.68 to close at $278.92, an increase of 21.67%.

On January 16, Spectrum of the Seas returned to its homeport in Shanghai to commence a full-year sailing season. In the same month, the company brought forward the inaugural sailing of Star of the Seas and added two additional voyages on August 23 and 27.

On July 1, the company announced that the Royal Beach Club – Paradise Island opened for reservations and was slated to debut by year-end. On July 29, it released Q2 results, reporting EPS of $4.41, and raised full-year guidance again.

Looking at 2026, the third flagship class ship is expected to enter service during the year, alongside the opening of Royal Beach Club Santorini. Leveraging Perfect Day at CocoCay and other private-destination assets, the company aims to optimize capacity and pricing mix while lifting high-margin onboard and shore-side spending.

[For more insights, please download the full report]

Experience-refined Value Picks

1. Shinsegae Inc. (KSE: 004170)

Shinsegae is an integrated retail group headquartered in Seoul, South Korea, with department stores as its core business. Through its subsidiaries, it operates high-end outlets and duty-free formats, and is one of the “big three” department store groups in Korea. For full-year 2025, the company’s share price rose by $85.04 to close at $172.90, an increase of 96.79%.

In March, the company undertook the largest renovation in 12 years at its Myeong-dong main store, expanding high jewelry/designer brands and VIP clubs, and reconfiguring circulation and F&B to enhance immersion. On April 9, “THE HERITAGE” officially opened: a century-old building restored into a “culture–luxury” symbiotic space—CHANEL (boutique designed by Peter Marino) on levels 1–2, a museological exhibition on level 4, and a Korean craftsmanship gallery on level 5—making it a city-level destination.

In July, the company launched the high-end travel platform “VIA SHINSEGAE,” building end-to-end journey services (from chauffeured transfers and fast-track check-in to post-trip dining and exhibitions) via Masterpiece products such as “Arctic Icebreaker Expedition” and “Abu Dhabi Elite Racing Behind-the-Scenes Access,” and Origin products featuring “wellness + culture.” Spend is credited into the department store VIP program, with co-branded card linkage in tandem.

Looking at 2026, Shinsegae is set to benefit from the full-year pull-through of the Myeong-dong flagship renovation and “The Heritage,” the maturing operations of community-style Starfield Village, and monetization via member linkages between Myeong-dong Duty Free “K-trend” content and the “VIA SHINSEGAE” high-end travel platform—driving visit frequency and basket size while lifting the mix of luxury and experiential businesses.

2. Wynn Resorts, Limited (NASDAQ: WYNN)

Wynn Resorts is a luxury resort developer and operator headquartered in Las Vegas, with upscale integrated resorts in Las Vegas, Boston, and Macau, including Wynn Las Vegas, Encore Boston Harbor, Wynn Macau, and Wynn Palace. For full-year 2025, the company’s share price rose by $34.63 to close at $120.33, an increase of 40.40%.

In January, Wynn announced the acquisition of Crown London Aspinalls in Mayfair, entering Europe’s ultra–high-net-worth social circle.

In February, financing of $2.4 billion was completed for “Wynn Al Marjan Island” in Ras Al Khaimah, UAE; the company disclosed a “one floor per week” structural construction pace and progress in guestroom fit-out, securing funding and engineering milestones toward a 2027 opening.

In June, Wynn completed $2 billion in refinancing to optimize its capital structure, opened “Wynn Mayfair,” and rolled out new summer dining scenes including the “Revelry” food festival and “PISCES Bar & Seafare,” expanding touchpoints across eat–stay–play–shop–entertain.

In September, “Wynn Signature—Hypercar Exhibition” returned, extending the luxury narrative through extreme motoring culture. Foreign media also reported that the company reserved a second integrated resort parcel on Al Marjan Island and embedded a potential local listing pathway in the shareholders’ agreement, reinforcing the Middle East “experience universe” growth optionality.

In October, around the F1 Las Vegas Grand Prix Week, Wynn staged “Ultimate Race Week” and hosted a Domaine de la Romanée-Conti (DRC) dinner, further deepening the sports + fine wine + social immersion.

Looking at 2026, Wynn is expected to consolidate share in Macau via a premium clientele and ongoing non-gaming/product upgrades, while in Las Vegas it aims to sustain its high-end positioning alongside robust MICE/group bookings.

[For more insights, please download the full report]

MACROECONOMY UPDATES

Structural Reshaping Forging Resilience,

Steady Progress Navigating Market Uncertainty

Global Economy Growth

Global: Structural adjustment and resilience testing coexist,

with growth sought amid uncertainty in 2026

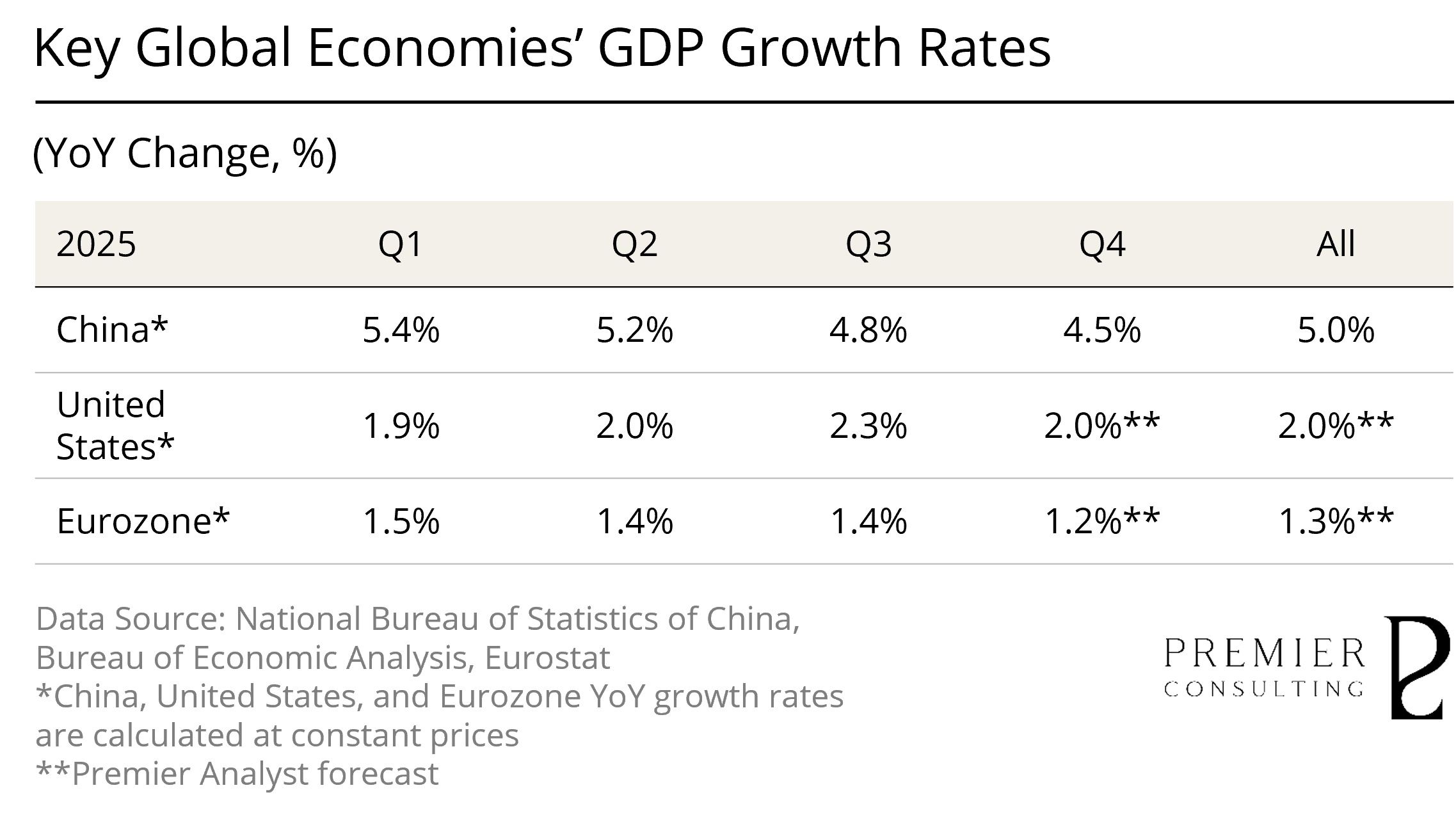

After volatility in 2023–2024, the global economy moved into a phase of moderate expansion in 2025. Institutions including the IMF expect global growth of around 3.1%–3.2%. Although below the historical average, this pace reflects a degree of resilience amid trade frictions, energy price swings, and geopolitical tensions.

Growth in advanced economies remained relatively subdued, while emerging and developing markets maintained faster expansion, supporting overall global growth. Global inflation continued to ease gradually but with notable regional divergence: core inflation in some advanced economies remained above target, while many emerging markets saw clearer declines. Despite tariff pressures and uncertainty, partial policy coordination and supply chain restructuring helped major economies maintain basic trade hookup stability.

On the policy front, major central banks made incremental, data-dependent adjustments after inflation showed initial signs of control. The Fed and the ECB, while maintaining overall stability, increasingly balanced growth and financial stability considerations, creating wider tolerance bands for market volatility. Global equities performed relatively steadily on liquidity and earnings support, while some commodities and safe-haven assets saw sharper swings, reflecting divergent expectations about future risks.

Looking into 2026, the global economy is expected to maintain moderate growth but at a potentially slower pace. Forecasts from the UN, Goldman Sachs, and others suggest global GDP growth of around 2.7%–2.8%, slightly below 2025 levels, highlighting continued divergence in demand and investment momentum. Advanced markets are likely to see moderate growth, while emerging economies remain key drivers, albeit constrained by trade frictions, debt risks, and demographic challenges.

In terms of inflation and monetary policy, global inflation is expected to ease further, with core inflation in most major economies moving closer to policy targets, giving central banks greater room for maneuver. Major central banks, including the Federal Reserve, may implement moderate rate cuts in 2026 to support growth, while Europe and other economies are likely to remain more cautious amid structural bottlenecks and medium- to long-term growth risks.

Regional divergence remains evident. U.S. growth is expected to stay moderate but resilient; the Eurozone faces structural constraints but is seeing improving inflation dynamics; emerging Asian economies are likely to maintain relatively strong growth driven by both domestic demand and exports; Latin America and Africa are expected to improve gradually alongside policy adjustments and firmer external demand. Global trade should continue to support growth in 2026, though unilateral protectionism and policy uncertainty remain downside risks.

[For more insights, please download the full report]

Consumer Confidence Index

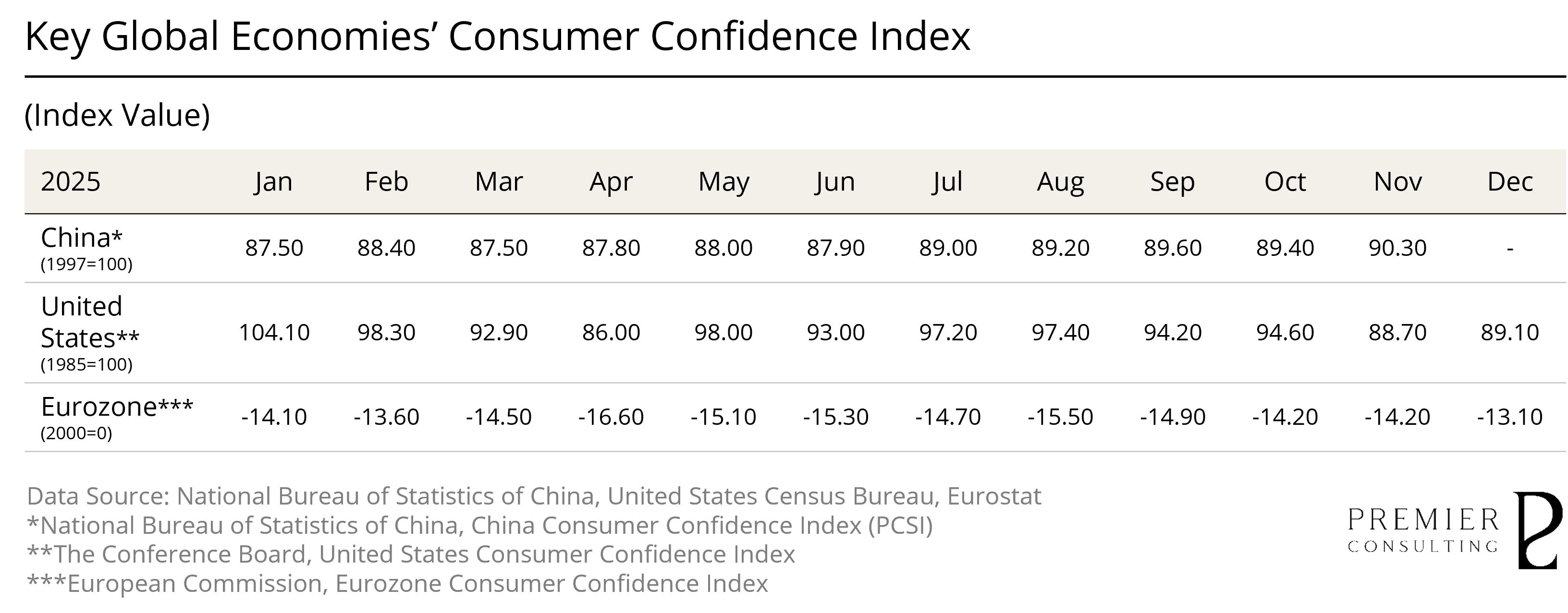

China: Employment stability and low inflation underpin a recovery phase driven by expectations

In 2025, China’s consumption showed “aggregate repair but weak expectations.” Retail sales grew 3.7% year-on-year, with online and service consumption remaining resilient, though monthly growth slowed to 0.9% by year-end, indicating recovery was largely structural rather than fundamental. Disposable income grew 5.0% in both nominal and real terms, supporting spending, but asset volatility and external uncertainty led households to raise risk premiums and delay discretionary purchases, slowing confidence recovery.

Employment remained broadly stable, with surveyed urban unemployment at 5.2%. However, structural mismatches in skills, sectors, and regions constrained job quality and income expectations for new labor entrants, weighing on consumption confidence through the income-expectations channel.

Price levels stayed low. CPI was broadly flat versus 2024, with year-end inflation at 0.8% and core CPI at 0.7%, indicating limited demand-side pressure. Continued PPI weakness reflected ongoing supply-demand rebalancing and weak price transmission, leaving a gap between corporate profit recovery and consumer willingness to spend.

Looking forward to 2026, consumer confidence is poised for a measured recovery from its troughs, though the path to repair remains fraught with uncertainty. The durability of this improvement will be contingent upon whether three pivotal transmission chains can yield verifiable real-world gains:

Firstly, through the stabilization of employment and enhancement of job quality to bolster household income expectations and the subsequent appetite for discretionary spending; furthermore, via the continued alleviation of balance sheet pressures linked to real estate and household leverage, which serves to revive risk appetite and marginally dampen precautionary saving motives; and finally, through the successful transition of consumption-support policies—centered on services and durables—into sustainable demand drivers that elevate the consumer experience and propensity to spend via supply-side optimization and scenario innovation.

Employment is likely to remain stable in aggregate but structurally divergent, with service absorption, job quality in new sectors, and skills matching remaining key variables shaping income expectations and spending behavior.

[For more insights, please download the full report]

Retail Sales Growth Review & Outlook

China: Resonating Momentum and Structural Upgrading,

Policy Tailwinds Underpinning Consumption Release

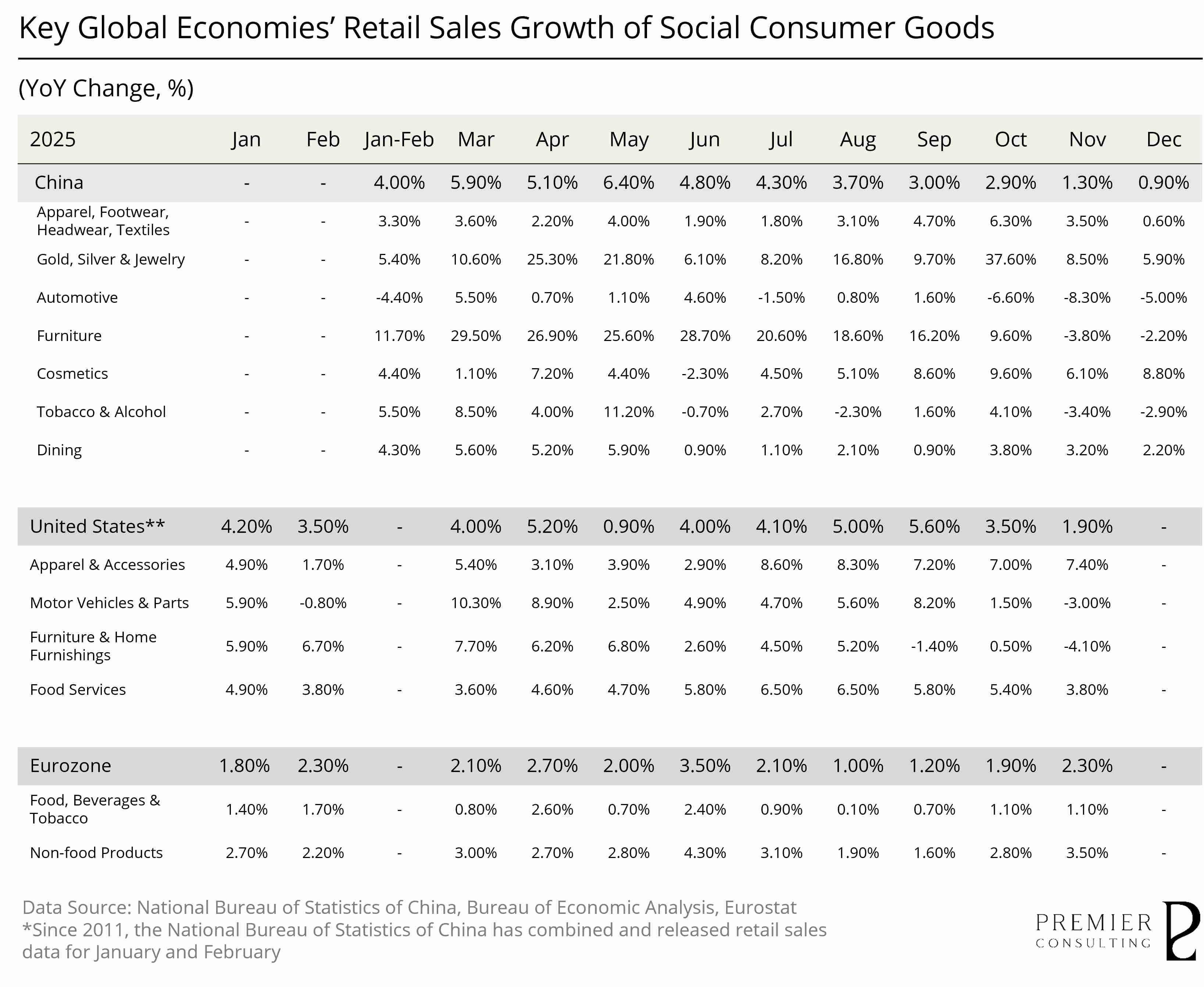

According to data released by the National Bureau of Statistics (NBS), China's total retail sales of consumer goods reached RMB 50.12 trillion in 2025, representing a year-on-year growth of approximately 3.7%, signaling the overall resilience of the consumption sector. Notably, retail sales excluding automobiles showed a stronger growth rate of roughly 4.4%, highlighting the robustness of traditional consumption driven by both inelastic demand and service-related spending.

Granular data further reflects significant structural improvements: service-oriented consumption, such as catering, sports, and entertainment, maintained a relatively fast growth pace. Meanwhile, emerging categories including jewelry, cosmetics, and sporting goods delivered standout performances, underscoring an ongoing cycle of consumption upgrading.

Concurrently, demand for service consumption accelerated, showing structural expansion in sectors like culture, tourism, sports, and wellness. Service retail sales grew 5.20% year-on-year in the first three quarters, outpacing the growth rate of commodity retail sales by 0.6 percentage points, indicating a steady shift in consumption patterns from goods-oriented to service and experience-oriented.

Furthermore, emerging consumption formats remained vibrant, with rapid penetration of new models like instant retailing, live-streaming e-commerce, and social commerce, fostering the digital upgrade of consumption scenarios. National online retail sales grew 9.80% year-on-year in the first three quarters, with the growth rate accelerating consistently since May, establishing it as a significant driver of overall consumption.

Despite the overall restorative growth in consumption, its pace remains below the overall economic growth rate, indicating that household consumption willingness and confidence require further bolstering. Looking ahead to the fourth quarter, stabilizing employment expectations, improving income distribution structures, and strengthening consumer credit support will be crucial to continuously enhance households' actual purchasing power and propensity to consume, thereby guiding the Chinese consumer market towards higher-quality and more sustainable growth.

Within the consumption structure, luxury goods and other discretionary spending have emerged as critical variables in the divergence of annual consumption. Overall, such consumption is more directly influenced by consumer confidence, income expectations, and wealth effects, exhibiting more pronounced structural characteristics. On one hand, high-net-worth individuals and certain "high-value, strong value-retention/heritage" categories demonstrate relative resilience, with consumption increasingly characterized as "certainty-based expenditure." On the other hand, discretionary consumption targeting the broader middle-to-high-income group is more susceptible to disturbances from macroeconomic uncertainties and rising price sensitivity, manifesting as prolonged purchasing decision cycles, decreased frequency, and significantly higher requirements for "cost-performance/perceived value."

At the same time, discretionary consumption faces periodic downward pressure. Against a backdrop of fluctuating macroeconomic expectations and cautious consumer risk appetite, consumers are more inclined to defer large-scale discretionary spending, increase sensitivity to price and benefits, and shift expenditures from "brand premiums" toward quantifiable value elements such as materials, craftsmanship, rarity, service experience, and usage scenarios. This implies that fluctuations in luxury consumption stem more from changes in "expectations and perceptions" rather than a simple disappearance of demand; market performance will rely more on whether brands can reinforce the "reason to buy" through product and service excellence and reduce decision-making friction in discretionary consumption through more refined customer segment operations.

Looking ahead to 2026, Chinese social consumption is expected to enter a new stage of "stabilizing quality and optimizing structure." From a policy allocation perspective, the central government has deployed a comprehensive stimulus package aimed at boosting domestic demand through expanding consumer credit, extending trade-in subsidies, and broadening service consumption scenarios. For luxury and discretionary consumption, such policies manifest more as indirect improvements: by stabilizing employment and income expectations, strengthening the supply of service consumption and experiences, and optimizing the consumption environment and supply structure, the uncertainty premium for residents will gradually decrease, thereby driving a marginal recovery in discretionary consumption.

Building on this, the growth rate of total retail sales of social consumer goods in 2026 is expected to be slightly higher than in 2025, with consumption's contribution to economic growth likely to increase further. The consumption structure will continue to tilt toward service-based consumption, high-quality experiential consumption, and smart living sectors; online retail and new lifestyle consumption will maintain growth rates above the overall level. The long-term growth driver of the consumer market will lie in resident income growth, improved wealth effects, and the expansion of new consumption models.

[For more insights, please download the full report]

PRIMARY INDEX REVIEW & PROSPECT

Channel Adjustments Signaling Demand Divergence,

Macro Expectations Reshaping Index Valuations

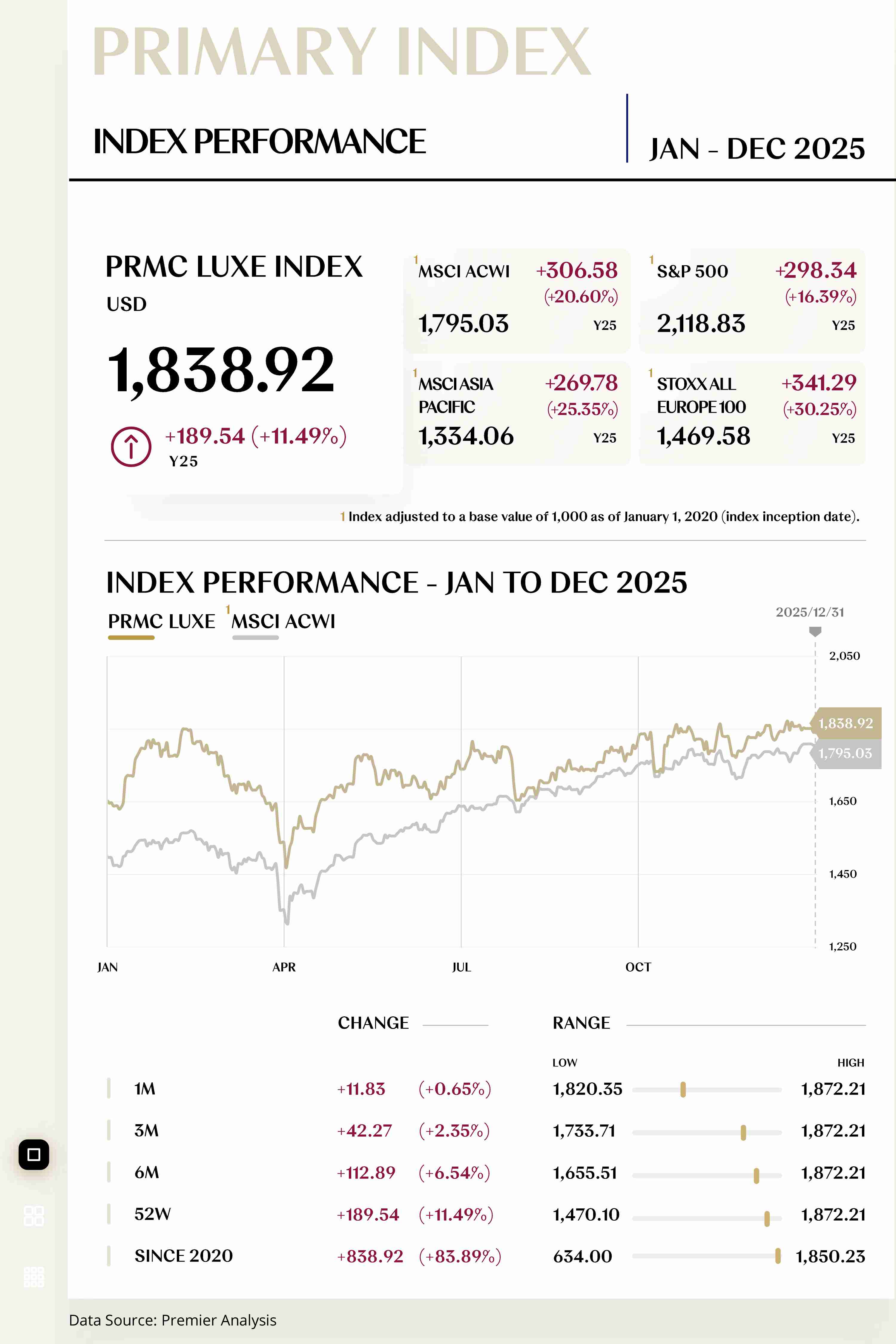

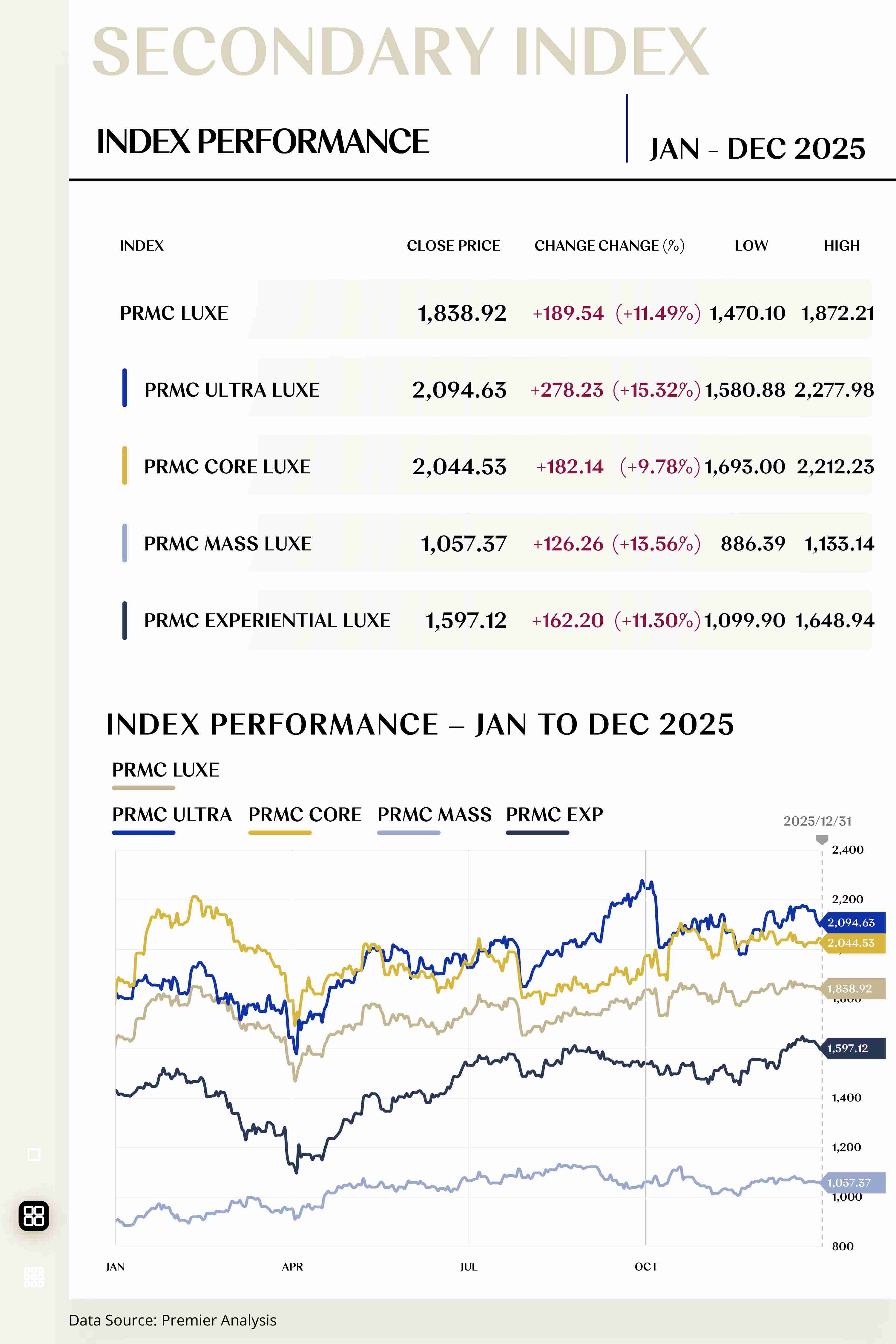

As of December 31, 2025, the PRMC Luxe Index closed at 1,838.92 points, rising by 189.54 points during the year, an increase of 11.49%.

Reviewing the full year, the index overall exhibited an evolutionary path of "periodic retracement—recovery and rebound—high-level volatility": it maintained range-bound fluctuations between valuation resilience and demand divergence early in the year, with April being the primary retracement period. Subsequently, it gradually recovered supported by leading companies' earnings stability, strengthened channel and inventory discipline, and marginal improvement in global risk appetite, entering a state of "trending upward but deepening divergence" in the second half of the year.

During the first quarter, the index experienced both range-bound volatility and structural rotation. On one hand, global interest rate expectations and the liquidity environment provided support for the valuation of high-quality assets, enhancing overall downside protection for the sector. On the other hand, regional differences in end-demand and channel sell-through, restocking/destocking rhythms, and corporate control over discount intensity continued to affect earnings visibility and market confidence. In this stage, the index primarily achieved price discovery through internal structural rotation, with market preference concentrating on leading companies with stable performance, stronger margin elasticity, and higher channel control, characterizing the sector as "resilient but with limited upside."

In April, the index experienced a significant retracement due to rising risk premiums triggered by the shift in US tariff policies. Additionally, earnings disclosures and management guidance provided a concentrated verification of market expectations: some companies' demand recovery progress in major markets fell short of expectations, which, coupled with the impact of expense investment, channel strategies, and product structure changes on profit margins, led investors to raise risk premium requirements in the short term. The adjustment in this stage was closer to a reassessment of valuation and earnings assumptions rather than a systemic reset of the industry's long-term growth logic.

From May to July, the index entered a recovery phase, driven by three main factors: first, a marginal improvement in risk appetite at the macro level provided renewed support for the valuation of high-quality consumer assets; second, improvements in inventory management, discount discipline, and expense efficiency by leading companies at the industry level gradually translated into profit margin stability and improved cash flow quality, enhancing earnings verifiability; third, travel-related consumption and experiential demand provided a buffer for cross-regional sales, reducing dependence on any single market. The pricing logic during the recovery phase gradually focused on "earnings quality and sustainable delivery," with relative returns within the sector further concentrating on companies with stronger operational resilience.

From August to December, the index maintained an overall upward trend, but with more prominent volatility characteristics. This was due to increased periodic disturbances to risk premiums from macro and policy variables, including changes in interest rate path expectations, exchange rate fluctuations, and geopolitical and trade policy uncertainties. Simultaneously, internal industry differences further magnified: companies with strong brand equity, superior product structures, higher channel control, and the ability to generate continuous cash flow remained relatively strong; while companies with high dependence on specific regions or single categories, or those facing greater discount pressure or expense rigidity, experienced more significant pressure.

Looking ahead to 2026, the PRMC Luxe Index is expected to exhibit a new round of divergent trends: at the valuation level, if the global interest rate environment continues to improve, the sector's valuation midpoint is expected to receive support; at the earnings level, the primary driver of the index's upside is expected to rely more on the verifiable delivery of operational results rather than mere expansion of expectations.

Sources of industry growth may be more structural: the ability of high-value categories such as jewelry and watches to capture wealth effects, the continuity of travel-related consumption, and the ongoing optimization of channel efficiency and cost management by top brands are expected to constitute the core pillars of the sector's resilience. Meanwhile, macro and policy uncertainties may still cause disturbances to periodic risk premiums, leading the index to exhibit range-bound volatility.

In terms of allocation strategy, it is recommended to focus on "quality premium and earnings delivery" as the core theme, concentrating research efforts on companies with stable pricing power and core customer assets, strong channel and inventory discipline, high profit margin and cash flow stability, and stronger anti-volatility capabilities in global layouts. Structurally, priority can be given to two directions of relative certainty: first, related assets with a higher proportion of high-value categories and high-end customer segments and stronger operational elasticity; second, related chain assets benefiting from travel consumption, experiential consumption, and scenario expansion.

Regarding risk management, it is recommended to use interest rates, exchange rates, trade policies, and demand recovery progress in key markets as key monitoring variables. Establishing scenario-based rebalancing mechanisms and controlling retracements through dynamic adjustments of positions and styles during periods of amplified volatility will enhance the stability and sustainable return quality of the portfolio in an uncertain environment.

SECONDARY INDEX REVIEW & PROSPECT

Ultra Luxe Leading and Core Luxe Stabilizing,

Mass Luxe Recovering and Experiential Luxe Accelerating

As of December 31, 2025, the PRMC Core Luxe Index closed at 2,044.53 points, rising by 182.14 points during the year, an increase of 9.78%.

Behind this performance was not a "universal rise," but a structural recovery driven by steadier high-net-worth demand, stronger category divergence, and capital preference for certainty:

On one hand, after experiencing a growth slowdown, global luxury demand entered a repricing stage of "de-bubbling—returning to product strength and cash flow," with consumption concentrating more on high-asset individuals and categories with high unit prices and strong value-retention attributes.

On the other hand, marginal improvements in interest rate paths and wealth effects, coupled with the redistribution of tourism and cross-regional consumption, led the market to re-elevate valuation weights for "certainty of delivery + high-quality earnings."

Specifically, the jewelry and watch sector played the role of an "anchor" in the index's performance throughout the year. First, jewelry possesses stronger intrinsic value and non-fashion cycle attributes; when consumption becomes more cautious, it is more easily interpreted as "wearable assets" and "essential gifting/commemoration," thus maintaining relative resilience. Second, leading jewelry brands, relying on classic collections, rare materials, and craftsmanship narratives, are able to maintain more stable price systems and gross margin structures amidst demand fluctuations. Finally, the watch sector, after experiencing previous supply-demand imbalances and a cooling secondary market, gradually returned to a "brand tier divergence" norm: high-end and complicated models remain attractive to high-net-worth segments, while mid-range and entry-level segments are more affected by discretionary consumption downgrades.

In contrast, the contribution of the fashion and leather goods sector to the Elite Luxury Index was more "periodic," with its rise coming more from the structural victory of leading brands. On one hand, price increases accumulated over the past few years more frequently hit the boundaries of demand elasticity in 2025; market tolerance for "trading price increases for growth" declined, turning instead to examine whether brands truly possess the support of product innovation, channel efficiency, and global customer structures.

On the other hand, travel retail and cross-border consumption recovery brought localized improvements, but recovery rhythms varied across regions. This, combined with adjustments in channel inventory and the wholesale side, caused the sector as a whole to exhibit earnings divergence where "the strong get stronger and the tail end faces pressure".

Looking ahead to 2026, the PRMC Core Luxe Index may enter a state of "moderate recovery and deepening divergence". At the macro level, if the path of falling inflation and declining interest rates in major economies continues, risk appetite and high-net-worth asset ends will provide support for luxury valuations, though geopolitical, trade friction, and exchange rate fluctuations may still periodically raise risk premiums. At the industry level, many institutions hold a "cautiously optimistic" judgment on subsequent demand recovery—growth will return but will rely more on product strength, customer structure, and channel health rather than simple expansion.

Specifically, the jewelry and watch sector may continue to lead growth in 2026. Under a tone of cautious consumption, jewelry possesses gifting, emotional, and value-storage attributes, and is more likely to differentiate price ranges and gross margins through high-end craftsmanship, rare gemstones, and high-end customization. Watches are likely to show "strong high-end, weak low-end": the rare supply and brand equity of top brands can still hedge against cycles, but the industry as a whole still faces pressures of channel destocking and price system maintenance after demand returns to normal, making the sector more about "selective opportunities."

The fashion and leather goods sector in 2026 is more likely to exhibit a "neutral-to-stable" recovery: if macro improvements drive a rebound in discretionary consumption, leading brands may benefit from travel consumption and new product cycles; however, after the room for price increases narrows, growth will rely more on the supply rhythm of core categories, store efficiency, and member operations, making it difficult to achieve comprehensive valuation uplifts through "universal price increases."

In terms of specific investment allocation, 2026 is better suited for a strategy of "quality first, structural victory":

First, prioritize companies with strong brand equity + high gross margins + supply rarity in the jewelry and high-end watch segments to hedge against macro volatility and obtain more stable earnings certainty.

Second, in fashion and leather goods, lean toward "heritage brands with deep customer connections and leading pricing power," focusing on their same-store efficiency, inventory health, and profit resilience under demand mismatches across different regions.

Third, control dependence on "price-driven" growth assumptions, using indicators like cash flow quality, expense discipline, and shareholder returns such as buybacks and dividends to calibrate valuation safety margins.

As of December 31, 2025, the PRMC Ultra Luxe Index closed at 2,094.63 points, rising by 278.23 points during the year, an increase of 15.32%.

Behind this performance was a round of structural recovery buoyed by "resilience of high-end demand" and "supply rarity," and amplified by marginal improvements in interest rates and risk appetite.

On one hand, although global luxury consumption remains within a broader scenario of "slowdown and divergence," the purchasing power and balance sheet resilience of high-end and ultra-high-end customer segments are stronger, making capital markets more willing to price for "order visibility, delivery verifiability, and cash flow certainty."

On the other hand, the private jet, private yacht, and luxury car sectors generally possess stronger characteristics of order lock-in and delivery cycles, forming a buffer of "using backlogs to hedge against demand fluctuations" during macro volatility, effectively supporting sector valuation levels.

Specifically, the core support for the private jet sector lies in the overlap of "high-end business travel demand + supply discipline + existing fleet renewal." With order and delivery rhythms visible over a long cycle, market valuation for leading companies is often anchored in delivery ramp-ups and the cash flow stickiness of after-sales services.

The private yacht sector more typically reflects the unique trait of "rare supply + high-end order lock-in": leading enterprises often "smooth out" demand fluctuations into order and delivery cycles through high-end customization, delivery scheduling, and price system management, resulting in stronger predictability for earnings and cash flow.

Based on earnings/order clues disclosed by some European yacht manufacturing leaders, market pricing for them also leans more toward "order quality, capacity ramp-up, and delivery fulfillment" rather than short-term sales fluctuations.

Excess returns in the luxury car sector are more concentrated in "brand pricing power and product premiumization." For example, by using personalized, high-margin models and relatively restrained exposure management in major markets, earnings certainty and anti-volatility attributes are strengthened. The market is more willing to pay a premium for the combination of "rare high-end supply + margin visibility."

In contrast, the furniture and home furnishings sector is closer to a pro-cyclical attribute sensitive to "discretionary consumption + real estate and interest rates." Its contribution to the index often manifests as periodic recovery, such as valuation elasticity brought by easing interest rate expectations, but it is typically weaker than "order-locked" yachts and aircraft in terms of boom sustainability, thus its pull on the index is more of an "intermittent contribution" rather than a "continuous uplift."

Looking ahead to 2026, the Ultra Luxury Index is more likely to enter a stage of "fundamental repricing" rather than mere "valuation expansion". At the macro level, if the path of falling inflation and declining interest rates becomes clearer, risk appetite will provide support for high-end discretionary consumption, but geopolitical, trade friction, and regulatory uncertainties may still raise risk premiums at certain points, causing the index rhythm to exhibit characteristics of "rising amidst volatility, progressing amidst divergence."

At the industry level, mainstream research generally believes that luxury demand will remain within a framework of moderate growth and structural divergence, with high-end customer resilience being relatively stronger, but regional recovery is not synchronized, especially related to the rhythm of China's consumption recovery and fluctuations in the wealth effects of Europe and the US. This means index opportunities are more likely to come from "segment leaders capable of continuously delivering orders and cash flow" rather than a universal rise.

Specifically, private jets and private yachts are likely to remain relatively advantaged "certainty assets": the core focus is on delivery fulfillment and after-sales service cash flow. If the global macro does not face severe headwinds, these two are more likely to stabilize earnings through order and capacity rhythms.

Within luxury cars, divergence will emphasize "brand pricing power + product structure upgrade + regional exposure management". Brands with strong reputations and high-margin product portfolios may continue to lead, while companies more exposed to price competition or regional demand fluctuations are likely to record lackluster performance.

Home furnishings and furniture are more likely to exhibit elastic characteristics of "recovering if interest rates are friendly, and facing pressure if interest rates fluctuate". Sustained valuation recovery will only be easier to achieve if global interest rate cuts are realized and real estate and high-net-worth consumption improve marginally.

As of December 31, 2025, the PRMC Mass Luxe Index closed at 1,057.37 points, rising by 126.26 points during the year, an increase of 13.56%.

The underlying logic of this round of index upside was the prior recovery of sub-sectors with more "affordable luxury" attributes, steadier cash flows, and stronger channel elasticity, which drove the recovery of the index's valuation midpoint.

Specifically, the fragrance and cosmetics sector was the core driver of the index's rise. Behind this, on one hand, consumers in an uncertain environment prefer the instant gratification of "small-scale but high emotional value" items; categories such as fragrances and makeup are more likely to form income resilience within a structure of "high-frequency repurchase + strong brand premium."

On the other hand, the periodic recovery of travel retail and cross-border passenger flows provided additional volume growth for international beauty groups. Large groups have also continued to reinforce the main themes of "category portfolio optimization, operational efficiency, and margin recovery" in their earnings communications, reflecting the stronger operational visibility and anti-volatility capabilities of the beauty track within the mass luxury sector.

Relatively speaking, the wine and spirits sector played more of a counteractive role in the overall index's rise. This sector is susceptible to two types of factors: first, the rhythm of channel inventory and wholesale destocking; second, disturbances from regional demand and the policy/trade environment.

From public information and news tracking of leading companies, the spirits industry faces pressures at the demand and channel levels in some regions, while also implementing multiple measures through price systems, portfolio upgrades, and cost management to achieve steady positive cash flow.

Looking ahead to 2026, the PRMC Mass Luxe Index may follow a path of "moderate upside, with rhythm more dependent on fundamental delivery." If global interest rate and inflation expectations become more friendly and travel retail continues to recover, the fragrance and cosmetics sector is expected to maintain its relative lead—scenario expansion for fragrances, structural recovery for makeup, and "value-proving consumption" represented by functional skincare/dermatological beauty could all become key levers for supporting valuation and earnings.

The wine and spirits sector is more likely to follow a long-term logic of "digesting inventory and repairing demand." If trade frictions and regulatory uncertainties rise, the valuation elasticity of this sector may continue to be suppressed; conversely, if channel replenishment and improved demand in emerging markets are realized, a window for periodic recovery may exist.

Allocation for related sectors needs to combine "certainty + structural" factors: prioritize companies in the fragrance and cosmetics sector with strong brand equity, product iteration capabilities, and channel control to obtain more predictable cash flow and margin recovery.

The wine and spirits sector emphasizes "valuation safety margin + inventory cycle turning point verification," with a focus on tracking destocking progress, regional demand recovery, and trade policy variables, while controlling retracements through diversification and dynamic rebalancing.

As of December 31, 2025, the PRMC Experiential Luxe Index closed at 1,597.12 points, rising by 162.20 points during the year, an increase of 11.30%.

The upside of the Experiential Luxury Index in this round essentially stems from the structural resilience maintained by "experiential consumption" amidst high interest rates and geopolitical uncertainties. On one hand, global travel and offline social interaction have entered a more sustainable normal range in the post-pandemic recovery, with demand transitioning from "compensatory explosion" to a steady state of "high-frequency, layered, and experience-heavy." On the other hand, the supply side finds it difficult to expand at an equal pace in the short term, allowing leading enterprises to translate demand into higher unit revenue and steadier cash flow through membership systems, dynamic pricing, and product upgrades.

Specifically, the cruising sector made a prominent contribution to the annual index. With higher visibility on the demand side and controllable delivery rhythms of new ships on the supply side, the industry benefited from the two growth themes of ticket prices and onboard consumption. Several leading cruise companies emphasized the continuation of "strong booking and pricing" into subsequent years in their earnings communications, which helps maintain long-term market sentiment.

The gambling sector manifested as "recovery realized but marginal slowdown." As a major destination for high-end entertainment and tourism in the Asia-Pacific, Macau achieved year-on-year growth in gross gaming revenue in 2025, but the market has begun to hold more moderate growth expectations for 2026, meaning the contribution logic for this sector will shift toward being driven by "operational efficiency and customer structure."

In contrast, the fine dining sector operated relatively stably: it benefited from the essential social needs and recovery of business activities of high-net-worth segments, but also faced cost stickiness from raw materials, labor, and rent. Industry returns came more from brand premiums, table turnover efficiency, and store structure optimization rather than simple volume expansion.

As for the fine art sector, its contribution to the 2025 Experiential Luxury Index was more of a "drag": the global art market continued to cool under fluctuating interest rates and wealth effects, with bidding for top high-priced items becoming more cautious and liquidity discounts rising, making the sector more prone to repricing when risk appetite retreats.

Looking ahead to 2026, the trend of the PRMC Experiential Luxe Index is likely to switch from "recovery-based upside" to "high-quality evolution." The hospitality sector is still expected to provide solid support, but excess returns are more likely to come from leading stocks capable of productizing experiences and converting passenger flows into members.

The cruising sector still possesses a relative advantage under high booking visibility, but requires a more rigorous assessment of the marginal impact of fuel, exchange rates, geopolitical disturbances, and new capacity on ticket prices; return divergence may increase.

The gambling sector is more likely to enter a stage of "low growth and heavy competition," where stock price elasticity will be determined by the structure of high-end and mass-market customer segments, the proportion of non-gaming revenue, and the balance between capital expenditure and dividends/buybacks.